Answered step by step

Verified Expert Solution

Question

1 Approved Answer

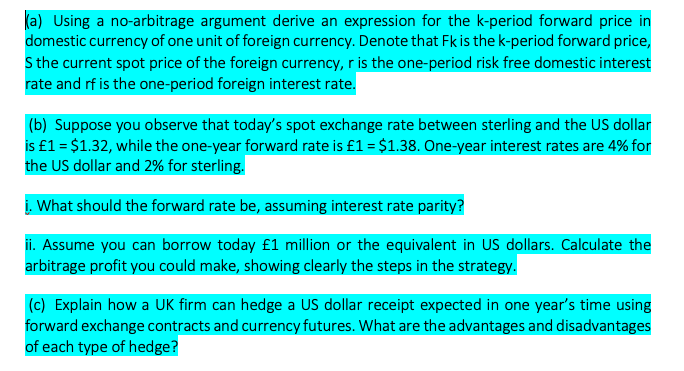

a) Using a no-arbitrage argument derive an expression for the k-period forward price in domestic currency of one unit of foreign currency. Denote that Fk

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

CA FOUNDATION FINANCIAL ACCOUNTING BY NSHAH MODULE I

Authors: Sanjay Nanak Chand Thadhani

1st Edition

172887419X, 978-1728874197