Question

a. Using the weighted average method, complete the following information regarding the Weaving and Pattern production process: I i. Physical flow schedule (measured in yards)

a. Using the weighted average method, complete the following information regarding the Weaving and Pattern production process:

I

i. Physical flow schedule (measured in yards)

ii. Materials

Conversion Costs

ili. Unit cost

iv. Cost of goods transferred out

b. To convert the output of the Weaving and Pattern Department to the output of the Coloring and Bolting Department, yards transferred is by

c. Using the weighted average method, complete the following for the Coloring and Bolting Department:

i. Physical flow schedule (measured in bolts)

Transferred-in

Materials

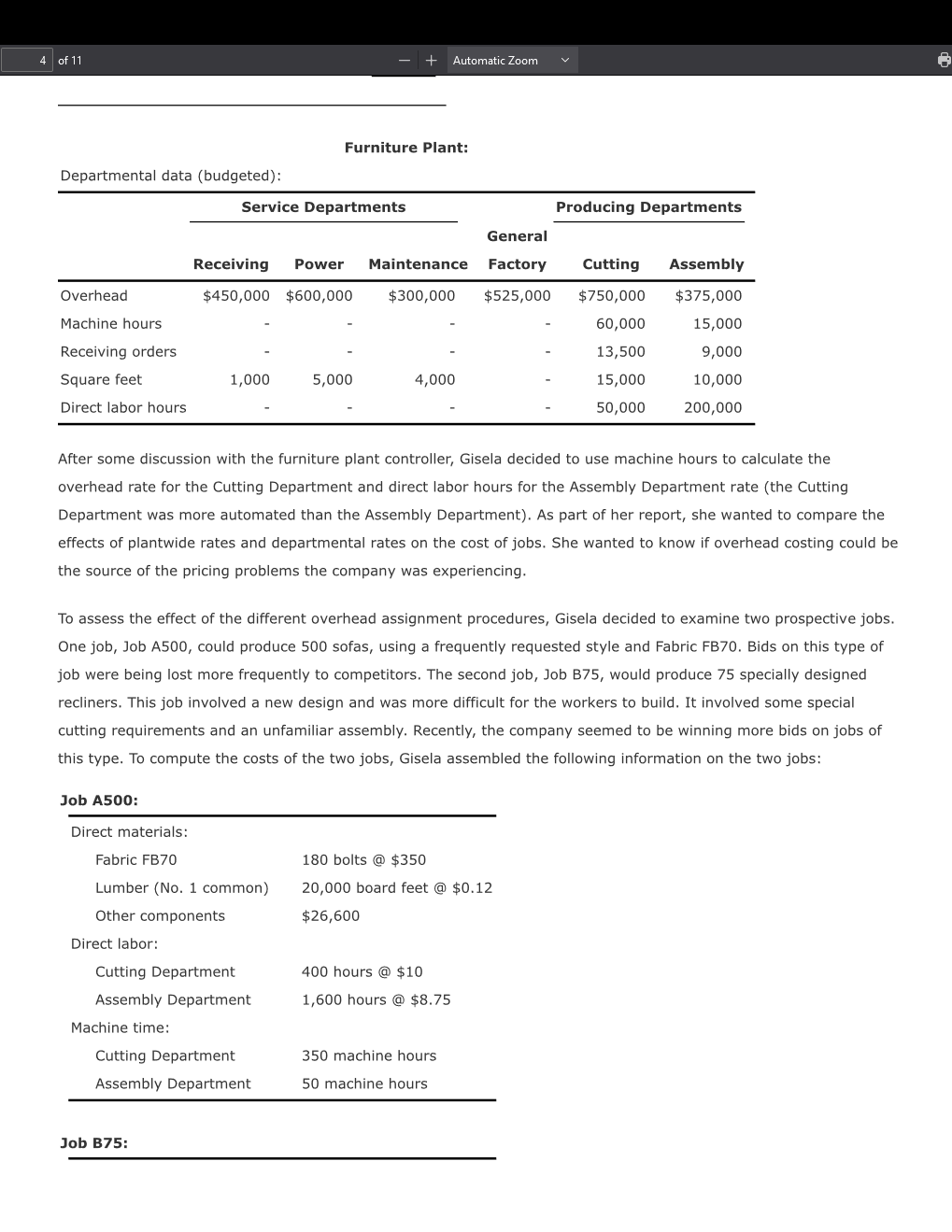

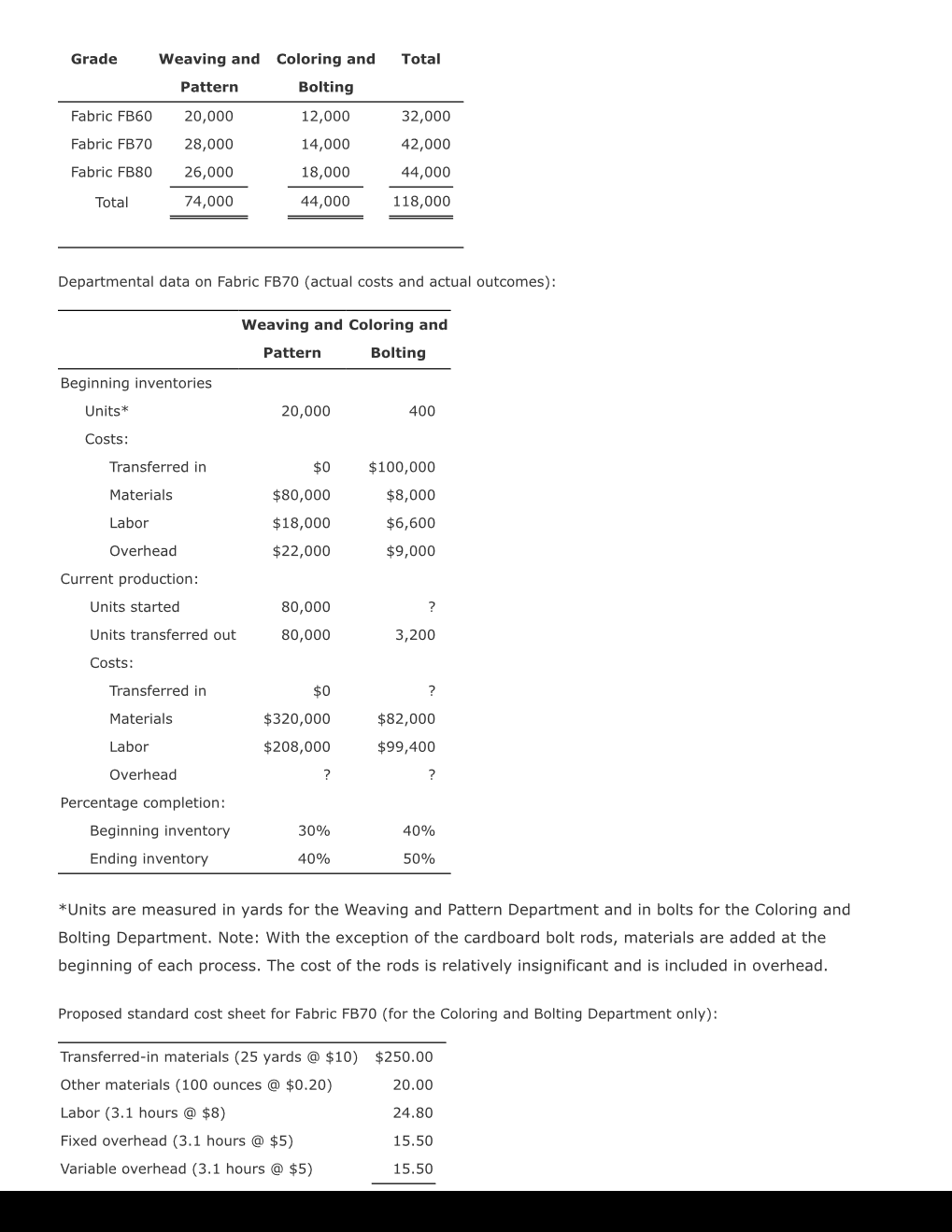

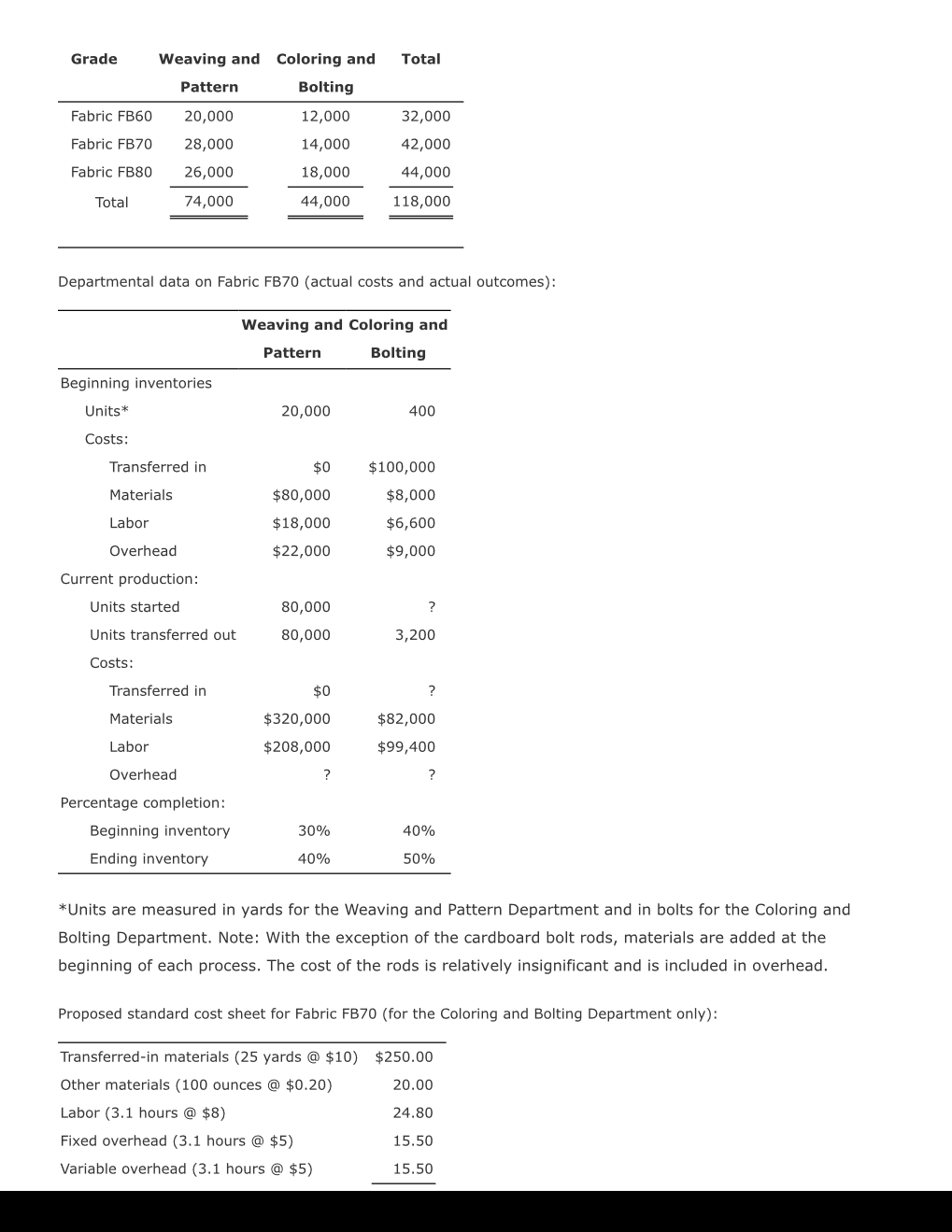

Furniture Plant: Departmental data (budgeted): After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the the source of the pricing problems the company was experiencing. To assess the effect of the different overhead assignment procedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric FB70. Bids on this type of job were being lost more frequently to competitors. The second job, Job B75, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs: Gisela prepared herself by reading recent literature on cost management and product costing and attending several conferences that explored the same issues. She then reviewed the costing procedures of the company's mill and two plants and did a preliminary assessment of their soundness. The production costs of the mill were common to all lumber grades and were assigned using the physical units method. Since the output and production costs were fairly uniform throughout the year, the mill used an actual costing system. Although Gisela had no difficulty with actual costing, she decided to explore the effects of using the sales-value-at-split-off method. Thus, cost and production data for the mill were gathered so that an analysis could be conducted. The two plants used normal costing systems. The fabric plant used process costing, and the furniture plant used job-order costing. Both plants used plantwide overhead rates based on direct labor hours. Based on her initial reviews, she concluded that the costing procedures for the fabric plant were satisfactory. Essentially, there was no evidence of product diversity. A statistical analysis revealed that about 90 percent of the variability in the plant's overhead cost could be explained by direct labor hours. Thus, the use of a plantwide overhead rate based on direct labor hours seemed justified. What did concern her, though, was the material waste that she observed in the plant. Maybe a standard cost system would be useful for increasing the overall cost efficiency of the plant. Consequently, as part of her report to Lance, she decided to include a description of the fabric plant's costing procedures-at least for one of the fabric types. She also decided to develop a standard cost sheet for the chosen fabric. The furniture plant, however, was a more difficult matter. Product diversity was present and could be causing some distortions in product costs. Furthermore, statistical analysis revealed that only about 40 percent of the variability in overhead cost was explained by the direct labor hours. She decided that additional analysis was needed so that a sound product costing method could be recommended. One possibility would be to increase the number of overhead rates. Thus, she decided to include departmental data so that the effect of moving to departmental rates could be assessed. Finally, she also wanted to explore the possibility of converting the sawmill and fabric plant into profit centers and changing the existing transfer pricing policy. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: \begin{tabular}{l} Fabric Plant: \\ Budgeted overhead: $1,200,000(50% fixed) \\ Practical volume (direct labor hours): 120,000 hours \\ Actual overhead: $1,150,000(50% fixed) \\ Actual hours worked: \\ \hline \end{tabular} Departmental data on Fabric FB70 (actual costs and actual outcomes): *Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only): Departmental data on Fabric FB70 (actual costs and actual outcomes): *Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only): Furniture Plant: Departmental data (budgeted): After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the the source of the pricing problems the company was experiencing. To assess the effect of the different overhead assignment procedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric FB70. Bids on this type of job were being lost more frequently to competitors. The second job, Job B75, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs: Gisela prepared herself by reading recent literature on cost management and product costing and attending several conferences that explored the same issues. She then reviewed the costing procedures of the company's mill and two plants and did a preliminary assessment of their soundness. The production costs of the mill were common to all lumber grades and were assigned using the physical units method. Since the output and production costs were fairly uniform throughout the year, the mill used an actual costing system. Although Gisela had no difficulty with actual costing, she decided to explore the effects of using the sales-value-at-split-off method. Thus, cost and production data for the mill were gathered so that an analysis could be conducted. The two plants used normal costing systems. The fabric plant used process costing, and the furniture plant used job-order costing. Both plants used plantwide overhead rates based on direct labor hours. Based on her initial reviews, she concluded that the costing procedures for the fabric plant were satisfactory. Essentially, there was no evidence of product diversity. A statistical analysis revealed that about 90 percent of the variability in the plant's overhead cost could be explained by direct labor hours. Thus, the use of a plantwide overhead rate based on direct labor hours seemed justified. What did concern her, though, was the material waste that she observed in the plant. Maybe a standard cost system would be useful for increasing the overall cost efficiency of the plant. Consequently, as part of her report to Lance, she decided to include a description of the fabric plant's costing procedures-at least for one of the fabric types. She also decided to develop a standard cost sheet for the chosen fabric. The furniture plant, however, was a more difficult matter. Product diversity was present and could be causing some distortions in product costs. Furthermore, statistical analysis revealed that only about 40 percent of the variability in overhead cost was explained by the direct labor hours. She decided that additional analysis was needed so that a sound product costing method could be recommended. One possibility would be to increase the number of overhead rates. Thus, she decided to include departmental data so that the effect of moving to departmental rates could be assessed. Finally, she also wanted to explore the possibility of converting the sawmill and fabric plant into profit centers and changing the existing transfer pricing policy. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: \begin{tabular}{l} Fabric Plant: \\ Budgeted overhead: $1,200,000(50% fixed) \\ Practical volume (direct labor hours): 120,000 hours \\ Actual overhead: $1,150,000(50% fixed) \\ Actual hours worked: \\ \hline \end{tabular} Departmental data on Fabric FB70 (actual costs and actual outcomes): *Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only): Departmental data on Fabric FB70 (actual costs and actual outcomes): *Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Non Accounting Students

Authors: John R. Dyson

7th Edition

0273709224, 9780273709220