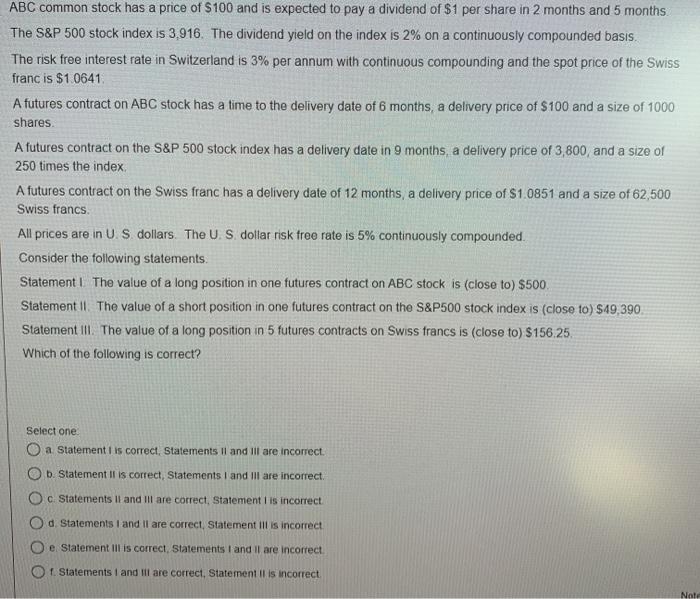

ABC common stock has a price of $100 and is expected to pay a dividend of $1 per share in 2 months and 5 months The S&P 500 stock index is 3,916. The dividend yield on the index is 2% on a continuously compounded basis. The risk free interest rate in Switzerland is 3% per annum with continuous compounding and the spot price of the Swiss franc is $1.0641 A futures contract on ABC stock has a time to the delivery date of 6 months, a delivery price of $100 and a size of 1000 shares A futures contract on the S&P 500 stock index has a delivery date in 9 months, a delivery price of 3,800, and a size of 250 times the index A futures contract on the Swiss franc has a delivery date of 12 months, a delivery price of $1.0851 and a size of 62,500 Swiss francs All prices are in US dollars. The US dollar risk free rate is 5% continuously compounded. Consider the following statements Statement. The value of a long position in one futures contract on ABC stock is (close to) $500 Statement. The value of a short position in one futures contract on the S&P500 stock index is (close to) $49,390 Statement Ill. The value of a long position in 5 futures contracts on Swiss francs is (close to) $156.25 Which of the following is correct? Select one O a Statement is correct, Statements II and Ill are incorrect. b. Statement il is correct, Statements I and Ill are incorrect O c Statements II and Ill are correct, Statement is incorrect d. Statements I and il are correct, Statement Ill is incorrect e Statement illis correct, Statements I and II are incorrect 1. Statements I and Ill are correct, Statement il is incorrect Note ABC common stock has a price of $100 and is expected to pay a dividend of $1 per share in 2 months and 5 months The S&P 500 stock index is 3,916. The dividend yield on the index is 2% on a continuously compounded basis. The risk free interest rate in Switzerland is 3% per annum with continuous compounding and the spot price of the Swiss franc is $1.0641 A futures contract on ABC stock has a time to the delivery date of 6 months, a delivery price of $100 and a size of 1000 shares A futures contract on the S&P 500 stock index has a delivery date in 9 months, a delivery price of 3,800, and a size of 250 times the index A futures contract on the Swiss franc has a delivery date of 12 months, a delivery price of $1.0851 and a size of 62,500 Swiss francs All prices are in US dollars. The US dollar risk free rate is 5% continuously compounded. Consider the following statements Statement. The value of a long position in one futures contract on ABC stock is (close to) $500 Statement. The value of a short position in one futures contract on the S&P500 stock index is (close to) $49,390 Statement Ill. The value of a long position in 5 futures contracts on Swiss francs is (close to) $156.25 Which of the following is correct? Select one O a Statement is correct, Statements II and Ill are incorrect. b. Statement il is correct, Statements I and Ill are incorrect O c Statements II and Ill are correct, Statement is incorrect d. Statements I and il are correct, Statement Ill is incorrect e Statement illis correct, Statements I and II are incorrect 1. Statements I and Ill are correct, Statement il is incorrect