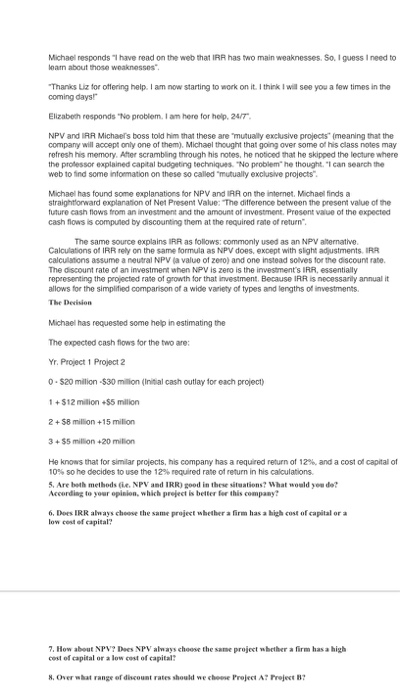

Abstract This case deals with the capital budgeting techniques of Net Present Value (ie. NPV) and Internal Rate of Return (.e. IRR). In this case, students will compare two mutually exclusive projects using NPV and IRR, and choose the best project. They will learn about NPV and IRR methods and their advantages and disadvantages. Students will also learn the weakness of the IRR method when comparing two or more projects. Finally, they will evaluate the two projects assuming that the projects are independent projects rather than mutually exclusive ones. This is a hands-on experience for students who want to delve into project valuation Introduction After graduating from an MBA Program on the East Coast, Michael Strahan had started working for a mining company. His company is evaluating two projects: One of them requires a smaller investment, and then will create a big, positive cash flow in the first year, and then smaller cash flows after that. The second project is a relatively bigger project. It will require a larger cash flow at the beginning, and then will bring in a relatively small cash flow in the first year. But, this second project will create much larger cash flows in the years after that. Michael has been given the task of evaluating these two projects and choosing the best one for his company. Initially he thought that this would be an easy task for him. He would just try to accurately predict the cash flows from the two projects and then evaluate them using some of the capital budgeting techniques that he had learned when he was at school. He visits Elizabeth, one of his colleagues, in order to clarity some issues that come to his mind. "Liz" he said, "I am tasked with evaluating two projects and then choosing the best one for our company. I am really excited because it seems like this decision will have a big impact on our company's bottom line. Could you help me a little bit?" Elizabeth has been working for the company for more than five years. She sure wants to help his colleague. She says "Sure, I can help you. Exactly what do you want to learn?" Michael sighs "Elizabeth, when evaluating these two projects, I think I need to use some of the capital budgeting techniques that we had learned at school. For example, we had Net Present Value, Internal Rate of Return, Payback Period, and others. I am not sure which of these methods to use". Elizabeth responds "I read somewhere that NPV and IRR are the most commonly used methods to evaluate a project. The Payback Period has lots of disadvantages, so you shouldn't use that one for sure". Michael responds "I don't know what the advantages and the disadvantages of each of these methods. I guess, first, I need to get more information about them. But, if I remember correctly, the Payback Period ignores the time value of money, so it is not good". Elizabeth says "And it also ignores the cash flows that come after the payback period. In otherwords if there is a very big positive cash flow that is expected to come sometime in the future, the Payback method ignores that. So, it is kind of weak. There are also other weaknesses with that method." She adds "IRR also has some weaknesses. I don't remember them, but you need to research. You don't want to do something wrong here." Michael responds have read on the web that IRR has two main weaknesses. So. I guess I need to learn about those weaknesses Thanks Liz for offering help. I am now starting to work on it. I think I will see you a few times in the coming days! Elizabeth responds "No problem. I am here for help. 24/7 NPV and IRR Michael's boss told him that these are "mutually exclusive projects" (meaning that the company will accept only one of them). Michael thought that going over some of his class notes may refresh his memory. After scrambling through his notes, he noticed that he skipped the lecture where the professor explained capital budgeting techniques. "No problem" he thought. I can search the web to find some information on these so called "mutually exclusive projects". Michael has found some explanations for NPV and IRR on the internet. Michael finds a straightforward explanation of Net Present Value: The difference between the present value of the future cash flows from an investment and the amount of investment, Prosent value of the expected cash flows is computed by discounting them at the required rate of return". The same source explains IRR as follows: commonly used as an NPV alternative Calculations of IRR rely on the same formula as NPV does, except with slight adjustments. IRR calculations assume a neutral NPV a value of zero) and one instead solves for the discount rate The discount rate of an investment when NPV is zero is the investment's IRR, essentially representing the projected rate of growth for that investment. Because IRR is necessarily annual it allows for the simplified comparison of a wide variety of types and lengths of investments The Decision Michael has requested some help in estimating the The expected cash flows for the two are: Yr. Project 1 Project 2 0 - $20 million -$30 million (Initial cash outlay for each project) 1 + $12 milion $5 milion 2 + $8 milion +15 million 3+ $5 million +20 milion He knows that for similar projects, his company has a required return of 12%, and a cost of capital of 10% so he decides to use the 12% required rate of return in his calculations 5. Are both methods die NPV and IRR) good in these situations? What would you do? According to your opinion, which project is better for this company 6. Does IRR always choose the same project whether a firm has a high cost of capital or a low cost of capital? 7. How about NPV? Does NPV always choose the same project whether a firm has a high cost of capital or a low cost of capital X. Over what range of discount rates should we choose Project A? Project B? Abstract This case deals with the capital budgeting techniques of Net Present Value (ie. NPV) and Internal Rate of Return (.e. IRR). In this case, students will compare two mutually exclusive projects using NPV and IRR, and choose the best project. They will learn about NPV and IRR methods and their advantages and disadvantages. Students will also learn the weakness of the IRR method when comparing two or more projects. Finally, they will evaluate the two projects assuming that the projects are independent projects rather than mutually exclusive ones. This is a hands-on experience for students who want to delve into project valuation Introduction After graduating from an MBA Program on the East Coast, Michael Strahan had started working for a mining company. His company is evaluating two projects: One of them requires a smaller investment, and then will create a big, positive cash flow in the first year, and then smaller cash flows after that. The second project is a relatively bigger project. It will require a larger cash flow at the beginning, and then will bring in a relatively small cash flow in the first year. But, this second project will create much larger cash flows in the years after that. Michael has been given the task of evaluating these two projects and choosing the best one for his company. Initially he thought that this would be an easy task for him. He would just try to accurately predict the cash flows from the two projects and then evaluate them using some of the capital budgeting techniques that he had learned when he was at school. He visits Elizabeth, one of his colleagues, in order to clarity some issues that come to his mind. "Liz" he said, "I am tasked with evaluating two projects and then choosing the best one for our company. I am really excited because it seems like this decision will have a big impact on our company's bottom line. Could you help me a little bit?" Elizabeth has been working for the company for more than five years. She sure wants to help his colleague. She says "Sure, I can help you. Exactly what do you want to learn?" Michael sighs "Elizabeth, when evaluating these two projects, I think I need to use some of the capital budgeting techniques that we had learned at school. For example, we had Net Present Value, Internal Rate of Return, Payback Period, and others. I am not sure which of these methods to use". Elizabeth responds "I read somewhere that NPV and IRR are the most commonly used methods to evaluate a project. The Payback Period has lots of disadvantages, so you shouldn't use that one for sure". Michael responds "I don't know what the advantages and the disadvantages of each of these methods. I guess, first, I need to get more information about them. But, if I remember correctly, the Payback Period ignores the time value of money, so it is not good". Elizabeth says "And it also ignores the cash flows that come after the payback period. In otherwords if there is a very big positive cash flow that is expected to come sometime in the future, the Payback method ignores that. So, it is kind of weak. There are also other weaknesses with that method." She adds "IRR also has some weaknesses. I don't remember them, but you need to research. You don't want to do something wrong here." Michael responds have read on the web that IRR has two main weaknesses. So. I guess I need to learn about those weaknesses Thanks Liz for offering help. I am now starting to work on it. I think I will see you a few times in the coming days! Elizabeth responds "No problem. I am here for help. 24/7 NPV and IRR Michael's boss told him that these are "mutually exclusive projects" (meaning that the company will accept only one of them). Michael thought that going over some of his class notes may refresh his memory. After scrambling through his notes, he noticed that he skipped the lecture where the professor explained capital budgeting techniques. "No problem" he thought. I can search the web to find some information on these so called "mutually exclusive projects". Michael has found some explanations for NPV and IRR on the internet. Michael finds a straightforward explanation of Net Present Value: The difference between the present value of the future cash flows from an investment and the amount of investment, Prosent value of the expected cash flows is computed by discounting them at the required rate of return". The same source explains IRR as follows: commonly used as an NPV alternative Calculations of IRR rely on the same formula as NPV does, except with slight adjustments. IRR calculations assume a neutral NPV a value of zero) and one instead solves for the discount rate The discount rate of an investment when NPV is zero is the investment's IRR, essentially representing the projected rate of growth for that investment. Because IRR is necessarily annual it allows for the simplified comparison of a wide variety of types and lengths of investments The Decision Michael has requested some help in estimating the The expected cash flows for the two are: Yr. Project 1 Project 2 0 - $20 million -$30 million (Initial cash outlay for each project) 1 + $12 milion $5 milion 2 + $8 milion +15 million 3+ $5 million +20 milion He knows that for similar projects, his company has a required return of 12%, and a cost of capital of 10% so he decides to use the 12% required rate of return in his calculations 5. Are both methods die NPV and IRR) good in these situations? What would you do? According to your opinion, which project is better for this company 6. Does IRR always choose the same project whether a firm has a high cost of capital or a low cost of capital? 7. How about NPV? Does NPV always choose the same project whether a firm has a high cost of capital or a low cost of capital X. Over what range of discount rates should we choose Project A? Project B