Question

ABSTRACT:The Walnut Creek Amphitheatre(Walnut Creek) case is intended for the undergraduate management accounting or cost accounting course and the M.B.A. management accounting course. It provides

ABSTRACT:The Walnut Creek Amphitheatre(Walnut Creek) case is intended for the undergraduate management accounting or cost accounting course and the M.B.A. management accounting course. It provides an excellent context in which to examine strategic issues in using cost volume profit (CVP) in a service business. Based on an actual entertainment pavilion, the case develops many factors unique to a service business and illustrates how pavilion management can use CVP analysis to determine which artists to attract and what kinds of contracts to have with these performers. The Pavilion has two types of customers (paying ticket holders and free ticket holders) and earns profits from three types of revenues (ticket revenues, concession revenues, and parking fees). The case requires you to identify the best strategy for different types of artists, conduct cost-volume-profit analyses, consider the strategic issues related to operating leverage and how this affects the choice of performer and contract, and assess pricing strategies.ne day in early November, Pam Berg, Manager of the Walnut Creek Amphitheatre(previously named the Time Warner Music Pavilion), was reviewing the operating results for the year just completed in preparation for the executive board meeting the following Friday. While the year ended in the black, she was disappointed that Walnut Creek failed to earn the budgeted profit goal. This was the second year since Ms. Berg assumed the managers position at Walnut Creek. After the somewhat disappointing first year, she was determined to exceed the budgeted profit in the coming year. While not all events developed exactly as expected at the time of preparing the budget for the year, there were no major surprises during the year. Yet, the operating results are below the budgeted goal. In addition, Pam was frustrated by the lack of clear guidelinesfor contract negotiations with artists, for setting ticket prices, and in dealing with unexpected low ticket sales for certain concerts.THE WALNUT CREEK AMPHITHEATREFOR LIVE ENTERTAINMENTThe Walnut Creek Amphitheatre in Raleigh, North Carolina (walnutcreekamphitheatre.com)is an outdoor amphitheater that provides live concerts to the public from April through October each year, hosting as many as half a million patrons a year. The seven-month season usually hosts an average of 40 concerts, and 12 year-round staff plan and manage each season. SFX Entertainment Inc. (or LiveStyle) operates the pavilion. SFX is one of the largest diversified promoters, producers, and venue operators for live entertainment events in the United States. It has 71 venues either directly owned or operated under lease or exclusive booking arrangements in 29 of the top 50 U.S.markets, including 14 amphitheaters or pavilions in 9 of the top 10 markets.Edward Blocher is a Professor at The University of North Carolina at Chapel Hill, and Kung H.Chen is a Professor at the University of NebraskaLincoln.O

Requirements:

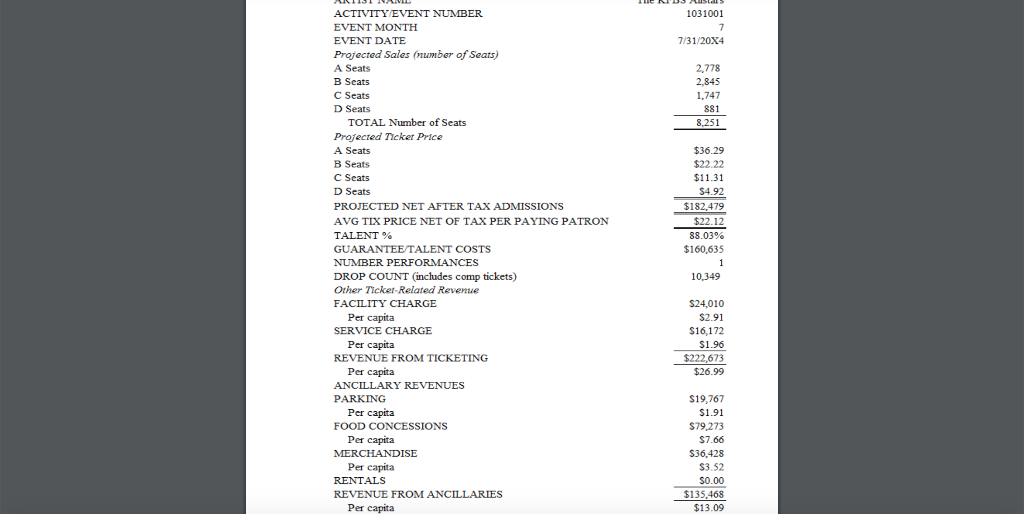

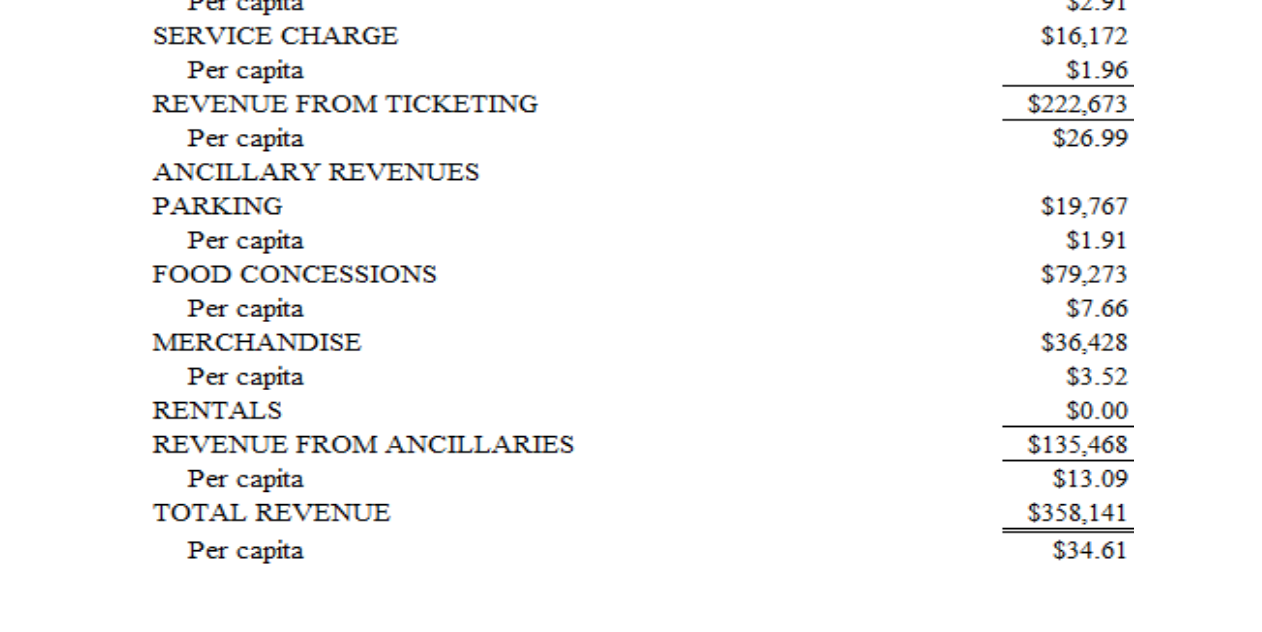

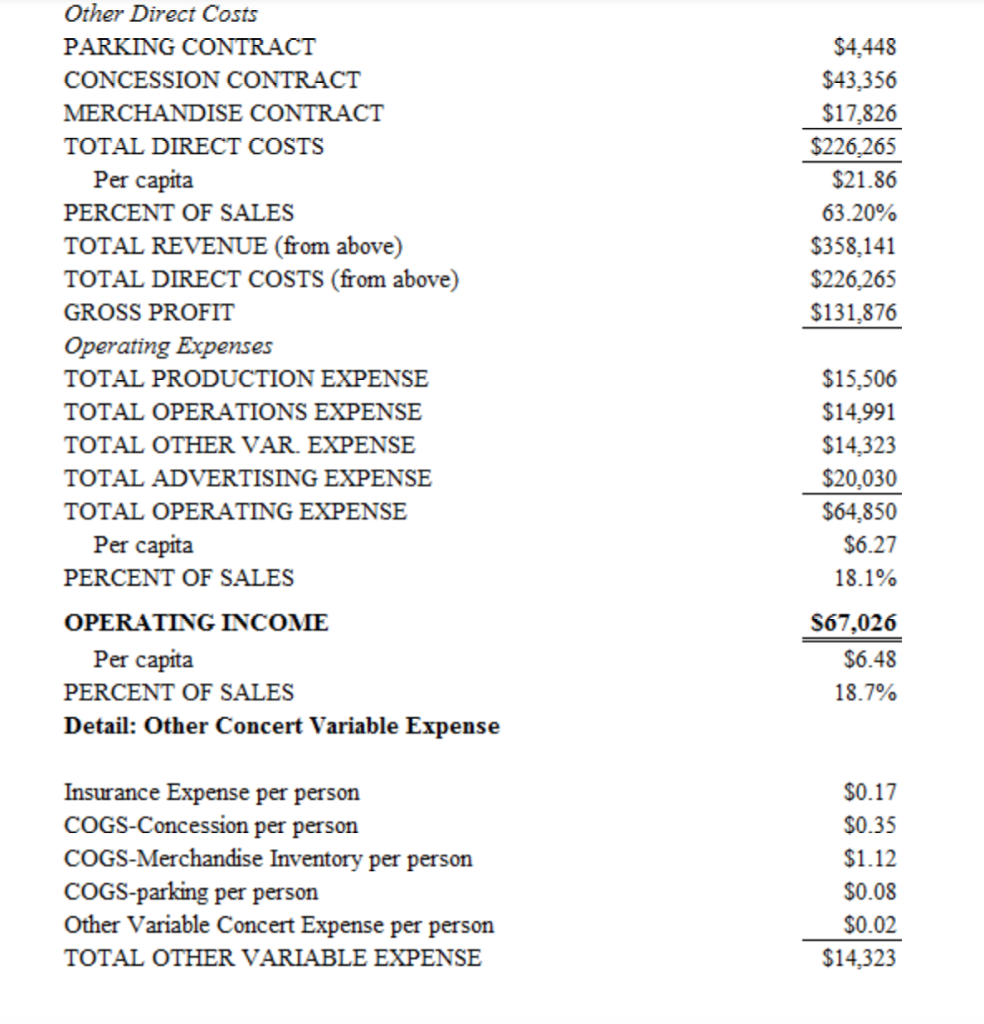

2.Complete the following two cost-volume-profit analyses for the show illustrated in Exhibit 2, the KFBS Allstars:

a.How many tickets must Walnut Creek sell to break even? (Hint: dont ignore the possibility that the attendance of Comp ticket holders affects the concerts profitability). i.Do you think that it is likely that Walnut Creek will break even? Briefly explain.

ii.Givenyour estimated breakeven point in units, compute the Margin of Safety (MOS) in units. Briefly comment on the MOS result.b.How many tickets must Walnut Creek sell to earn $30,000 operating income after taxes, assuming a 40 percent tax rate? Is it reasonable to assume this level of operating income will be achieved? Briefly explain.

3.What should be the average ticket price (for all ticket types combinedA through D) for the KFBS concert if the fixed-pay fee is $200,000(rather than $160,635) and Walnut Creek expects to sell 7,000 tickets and wants to earn $30,000 operating income after 40 percent in taxes? After you estimate the average ticket price for all ticket types combined (which is $22.12 for the situation depicted in Exhibit 2), estimate the price for each type of seat (i.e., in Exhibit 2: A--$36.29, B--$22.22, C--$11.31, D--$4.92). [Hint: assume sales mix for A, B, C, and D seats remains the same as the mix in the Flash Report (Exhibit 2).]

4.Negotiating the talent fee for the KFBS Allstars is an important strategic decision for Walnut Creek management. Perform the following two independent scenario analyses regarding differenttalentfee arrangements. Then comment briefly on what the results of your two scenario analyses suggest regarding whether Walnut Creek is better off negotiating a fixed-pay contract with performers or a per capita contract with performers:a.What is the maximum fixed fee that Walnut Creek can pay KFBS Allstars if Walnut Creek wants to earn $45,000 operating income after 40 percent tax and still expects the show to have an average ticket price of $22.12? Assume, including the same 25 percent comp tickets (i.e., 4:1 mix as before), the show is expected to be a sell-out.b.Independent of (a), what is the maximum per capita fee (see p. 557 of the case for the reference of the 2.5 percent comp tickets at per capita shows) that Walnut Creek can pay the KFBS Allstars, whose concert is expected to be a sellout, if the Pavilion wants to earn $180,000 operating income after 40 percent tax from an average ticket price of $22.12 per ticket?

5. Walnut Creek management examined the results of the scenarios examined in requirement 4 and subsequently held additional discussions with Walnut Creeks marketing team. The biggest uncertainty for Walnut Creek concerns the number of paying ticket patrons for lesser known performers. As a result, Walnut Creek management believes that the two most likely contract structure scenarios it will face when negotiating contracts with lesser known performers (i.e., bands) will be as follows. The first structure is per-capita in nature (Alternative 1) and would pay the performer a fee of $20 per paid ticket holder. The second structure is fixed in nature (Alternative 2) and would pay the performer a flat fee of $250,000. a.Assuming the same other relevant information from the case, calculate the indifference point for these two fee contract structures. Be sure to SHOW YOUR CALCULATIONS.Briefly explain what this indifference point means.b.What profit is earned by Walnut Creek at this indifference point? Be sure to SHOW YOUR CALCULATIONS.c.Walnut Creeks marketing team estimates that it will be able to sell 10,000 tickets for the hot new bandThe Dont Suck. Explain which contract structure Walnut Creek should pursue with The Dont Suck band negotiations and WHY this particular structure is best for Walnut Creek.

6.What role does CVP analysis and operating leverage play in contract negotiations with different types of performers (fixed-fee or per capita)?7.The results of CVP analyses are extremely useful for decision making. However, they also are highly dependent upon the assumptions used to generate the inputs into the CVP analyses. Preferably using an Excel spreadsheet (although you may simply use paper instead if you so desire), rerun the following two CVP analyses but take into account the sensitivity changes (i.e., changes in key assumptions) described below:

a.The break even analysis for requirement 2a: Assume now that the number of comp tickets in a fixed-fee concert is only 10 percent (rather than 25 percent as on p. 557of the case). What is the break even point in units given this change?

b.The maximum fixed-fee that Walnut Creek can pay in requirement 4a: Assume now that after the KFBS Allstar show is arranged (i.e., cant be moved or canceled), another unexpected big event becomes scheduled for the same evening as the KFBS Allstar show (e.g., Presidential debate, the Oscars, Cubs in another World Series Game 7, etc.). As a result, assume that the KFBS Allstar show draws only 3,000 paying ticket holders. What is the maximum fixed-fee that Walnut Creek can pay given this change?c.Explain any insights that the analyses in parts (a) and (b) revealed regarding the use of CVP for Walnut Creeks strategic decision making

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistical Sampling And Risk Analysis In Auditing

Authors: Peter Jones

1st Edition

1138263214, 978-1138263215