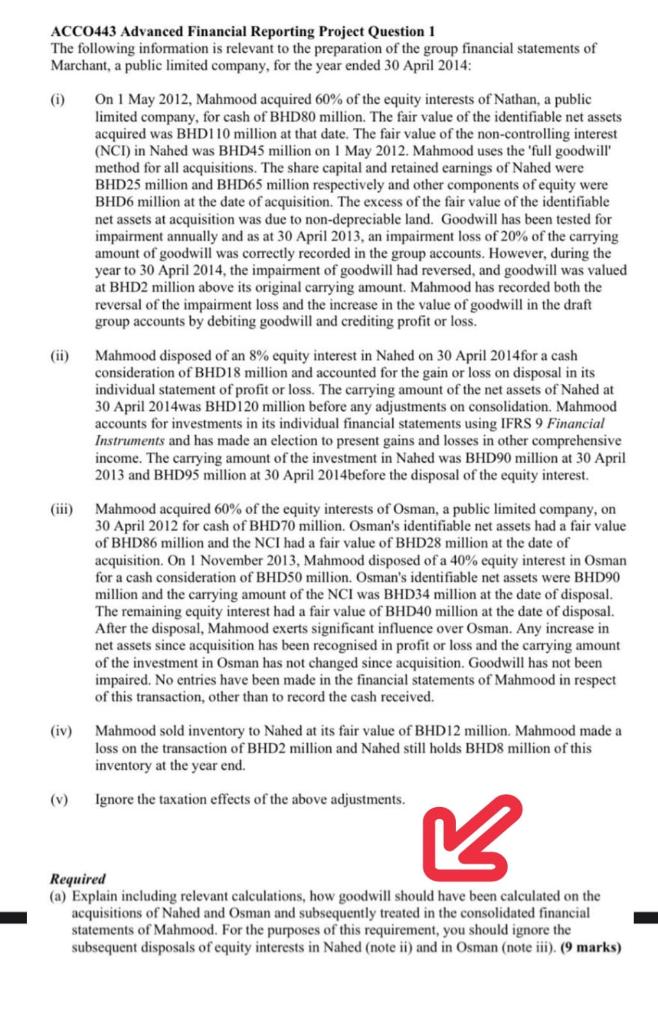

ACC0443 Advanced Financial Reporting Project Question 1 The following information is relevant to the preparation of the group financial statements of Marchant, a public limited company, for the year ended 30 April 2014: (i) On 1 May 2012, Mahmood acquired 60% of the equity interests of Nathan, a public limited company, for cash of BHD80 million. The fair value of the identifiable net assets acquired was BHDI 10 million at that date. The fair value of the non-controlling interest (NCI) in Nahed was BHD45 million on 1 May 2012. Mahmood uses the 'full goodwill method for all acquisitions. The share capital and retained earnings of Nahed were BHD25 million and BHD65 million respectively and other components of equity were BHD6 million at the date of acquisition. The excess of the fair value of the identifiable net assets at acquisition was due to non-depreciable land. Goodwill has been tested for impairment annually and as at 30 April 2013, an impairment loss of 20% of the carrying amount of goodwill was correctly recorded in the group accounts. However, during the year to 30 April 2014, the impairment of goodwill had reversed, and goodwill was valued at BHD2 million above its original carrying amount. Mahmood has recorded both the reversal of the impairment loss and the increase in the value of goodwill in the draft group accounts by debiting goodwill and crediting profit or loss. (ii) (iii) Mahmood disposed of an 8% equity interest in Nahed on 30 April 2014 for a cash consideration of BHD18 million and accounted for the gain or loss on disposal in its individual statement of profit or loss. The carrying amount of the net assets of Nahed at 30 April 2014was BHD120 million before any adjustments on consolidation. Mahmood accounts for investments in its individual financial statements using IFRS 9 Financial Instruments and has made an election to present gains and losses in other comprehensive income. The carrying amount of the investment in Nahed was BHD90 million at 30 April 2013 and BHD95 million at 30 April 2014before the disposal of the equity interest. Mahmood acquired 60% of the equity interests of Osman, a public limited company, on 30 April 2012 for cash of BHD70 million. Osman's identifiable net assets had a fair value of BHD86 million and the NCI had a fair value of BHD28 million at the date of acquisition. On 1 November 2013, Mahmood disposed of a 40% equity interest in Osman for a cash consideration of BHD50 million. Osman's identifiable net assets were BHD90 million and the carrying amount of the NCI was BHD34 million at the date of disposal. The remaining equity interest had a fair value of BHD40 million at the date of disposal. After the disposal, Mahmood exerts significant influence over Osman. Any increase in net assets since acquisition has been recognised in profit or loss and the carrying amount of the investment in Osman has not changed since acquisition. Goodwill has not been impaired. No entries have been made in the financial statements of Mahmood in respect of this transaction, other than to record the cash received. (iv) Mahmood sold inventory to Nahed at its fair value of BHD12 million. Mahmood made a loss on the transaction of BHD2 million and Nahed still holds BHD8 million of this inventory at the year end. (v) Ignore the taxation effects of the above adjustments. 2 Required (a) Explain including relevant calculations, how goodwill should have been calculated on the acquisitions of Nahed and Osman and subsequently treated in the consolidated financial statements of Mahmood. For the purposes of this requirement, you should ignore the subsequent disposals of equity interests in Nahed (note ii) and in Osman (note iii). (9 marks)