Answered step by step

Verified Expert Solution

Question

1 Approved Answer

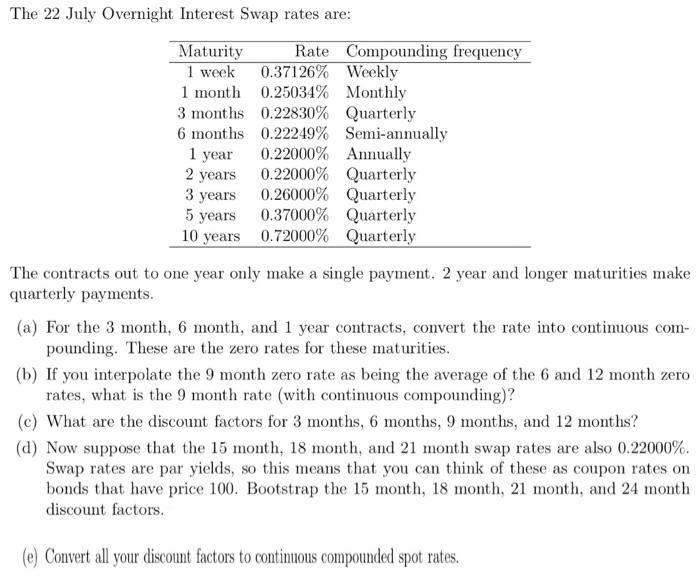

The 22 July Overnight Interest Swap rates are: Maturity 1 week 1 month 0.25034% Monthly 3 months 0.22830% Quarterly 6 months 0.22249% Semi-annually 1

The 22 July Overnight Interest Swap rates are: Maturity 1 week 1 month 0.25034% Monthly 3 months 0.22830% Quarterly 6 months 0.22249% Semi-annually 1 year 2 years 3 years 5 years 0.37000% Quarterly 10 years 0.72000% Quarterly Rate Compounding frequency 0.37126% Weekly 0.22000% Annually 0.22000% Quarterly 0.26000% Quarterly The contracts out to one year only make a single payment. 2 year and longer maturities make quarterly payments. (a) For the 3 month, 6 month, and 1 year contracts, convert the rate into continuous com- pounding. These are the zero rates for these maturities. (b) If you interpolate the 9 month zero rate as being the average of the 6 and 12 month zero rates, what is the 9 month rate (with contimuous compounding)? (c) What are the discount factors for 3 months, 6 months, 9 months, and 12 months? (d) Now suppose that the 15 month, 18 month, and 21 month swap rates are also 0.22000%. Swap rates are par yields, so this means that you can think of these as coupon rates on bonds that have price 100. Bootstrap the 15 month, 18 month, 21 month, and 24 month discount factors. (e) Convert all your discount factors to continuous compounded spot rates.

Step by Step Solution

★★★★★

3.53 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

a 3 month OIS rate 022830 Compounded quarterly 6 month OIS rate 022249 Compounded semiannually 1 year OIS rate 022000 Compounded annually Continuous rate Compounding frequency ln1 discrete rate compou...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Pathway To Introductory Statistics

Authors: Jay Lehmann

1st Edition

0134107179, 978-0134107172