Answered step by step

Verified Expert Solution

Question

1 Approved Answer

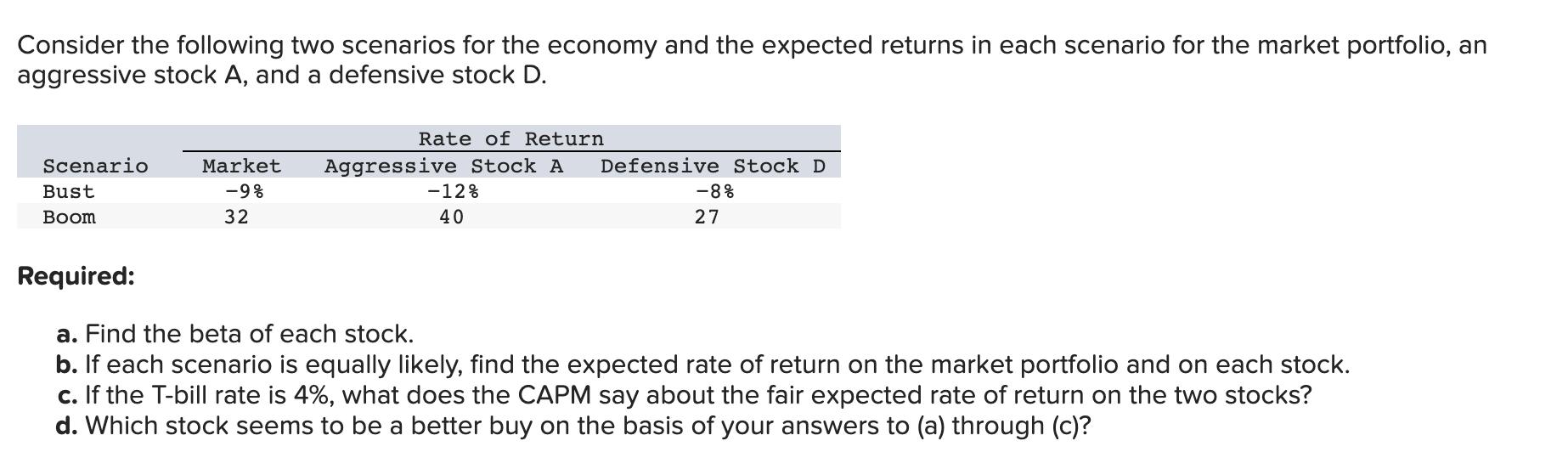

Consider the following two scenarios for the economy and the expected returns in each scenario for the market portfolio, an aggressive stock A, and

Consider the following two scenarios for the economy and the expected returns in each scenario for the market portfolio, an aggressive stock A, and a defensive stock D. Scenario Bust Boom Required: Rate of Return Market Aggressive Stock A -9% 32 -12% 40 Defensive Stock D -8% 27 a. Find the beta of each stock. b. If each scenario is equally likely, find the expected rate of return on the market portfolio and on each stock. c. If the T-bill rate is 4%, what does the CAPM say about the fair expected rate of return on the two stocks? d. Which stock seems to be a better buy on the basis of your answers to (a) through (c)?

Step by Step Solution

★★★★★

3.40 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

The in a clear step by step manner Step 1 answer provided below has been developed Return of Stock A ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Management Measuring Monitoring And Motivating Performance

Authors: Leslie G. Eldenburg, Susan K. Wolcott

2nd Edition

978-0-470-7694, 0470769424, 978-0470769423