Green Thumb Ltd. (GT Ltd.) is a Canadian-controlled private corporation operating a franchise gardening and plant nursery retail store in Kamloops, BC. Bob Green,

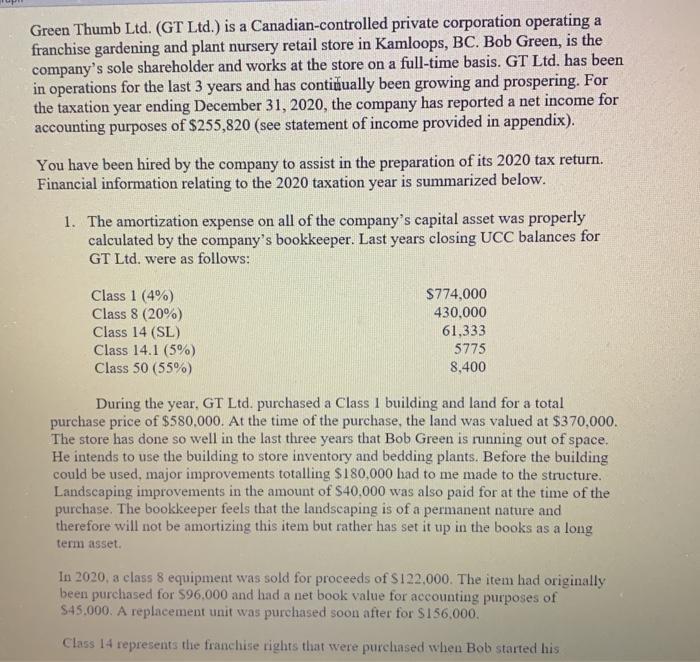

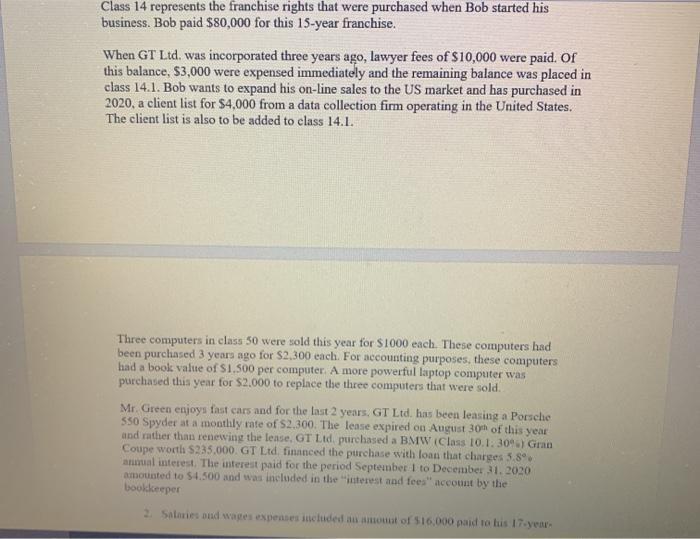

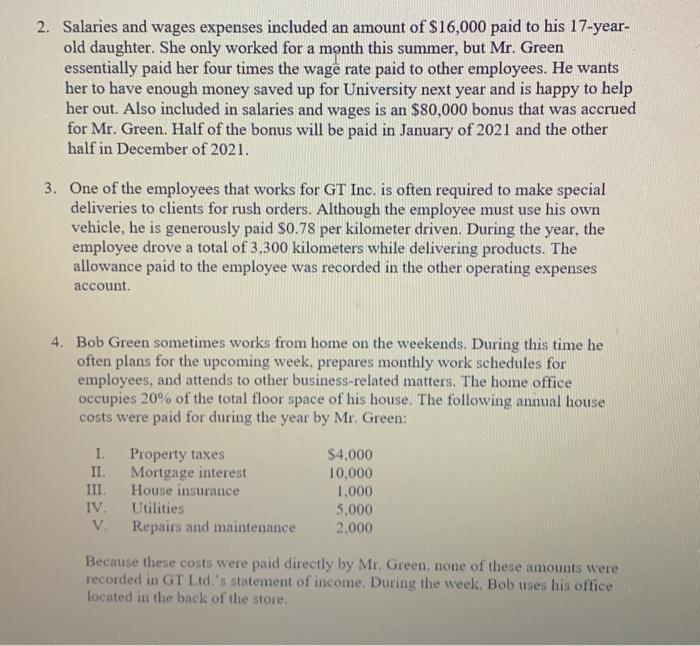

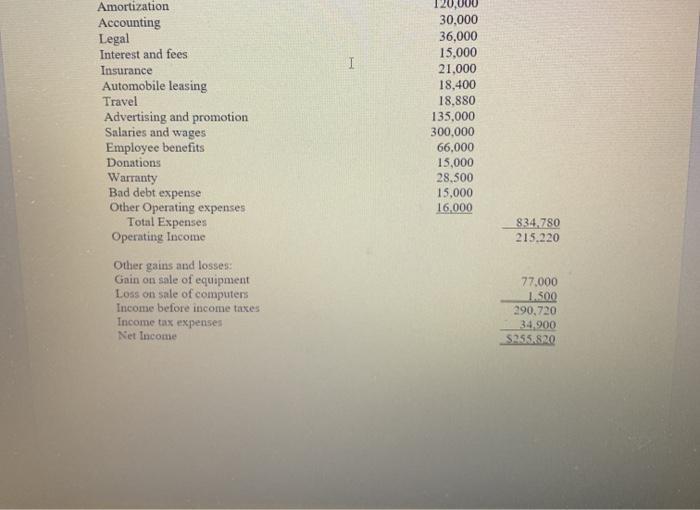

Green Thumb Ltd. (GT Ltd.) is a Canadian-controlled private corporation operating a franchise gardening and plant nursery retail store in Kamloops, BC. Bob Green, is the company's sole shareholder and works at the store on a full-time basis. GT Ltd. has been in operations for the last 3 years and has continually been growing and prospering. For the taxation year ending December 31, 2020, the company has reported a net income for accounting purposes of $255,820 (see statement of income provided in appendix). You have been hired by the company to assist in the preparation of its 2020 tax return. Financial information relating to the 2020 taxation year is summarized below. 1. The amortization expense on all of the company's capital asset was properly calculated by the company's bookkeeper. Last years closing UCC balances for GT Ltd. were as follows: Class 1 (4%) Class 8 (20%) Class 14 (SL) Class 14.1 (5%) Class 50 (55%) $774,000 430,000 61,333 5775 8,400 During the year, GT Ltd. purchased a Class 1 building and land for a total purchase price of $580,000. At the time of the purchase, the land was valued at $370,000. The store has done so well in the last three years that Bob Green is running out of space. He intends to use the building to store inventory and bedding plants. Before the building could be used, major improvements totalling $180,000 had to me made to the structure. Landscaping improvements in the amount of $40,000 was also paid for at the time of the purchase. The bookkeeper feels that the landscaping is of a permanent nature and therefore will not be amortizing this item but rather has set it up in the books as a long term asset. In 2020, a class 8 equipment was sold for proceeds of $122,000. The item had originally been purchased for $96,000 and had a net book value for accounting purposes of $45,000. A replacement unit was purchased soon after for $156,000. Class 14 represents the franchise rights that were purchased when Bob started his Class 14 represents the franchise rights that were purchased when Bob started his business. Bob paid $80,000 for this 15-year franchise. When GT Ltd. was incorporated three years ago, lawyer fees of $10,000 were paid. Of this balance, $3,000 were expensed immediately and the remaining balance was placed in class 14.1. Bob wants to expand his on-line sales to the US market and has purchased in 2020, a client list for $4,000 from a data collection firm operating in the United States. The client list is also to be added to class 14.1. Three computers in class 50 were sold this year for $1000 each. These computers had been purchased 3 years ago for $2,300 each. For accounting purposes, these computers had a book value of $1.500 per computer. A more powerful laptop computer was purchased this year for $2,000 to replace the three computers that were sold. Mr. Green enjoys fast cars and for the last 2 years, GT Ltd. has been leasing a Porsche 550 Spyder at a monthly rate of $2.300. The lease expired on August 30th of this year and rather than renewing the lease. GT Ltd. purchased a BMW (Class 10.1. 30%) Gran Coupe worth $235.000. GT Ltd. financed the purchase with loan that charges 5.8 annual interest. The interest paid for the period September 1 to December 31. 2020 amounted to $4.500 and was included in the "interest and fees" account by the bookkeeper 2. Salaries and wages expeases included an amount of $16,000 paid to his 17-year- 2. Salaries and wages expenses included an amount of $16,000 paid to his 17-year- old daughter. She only worked for a month this summer, but Mr. Green essentially paid her four times the wage rate paid to other employees. He wants her to have enough money saved up for University next year and is happy to help her out. Also included in salaries and wages is an $80,000 bonus that was accrued for Mr. Green. Half of the bonus will be paid in January of 2021 and the other half in December of 2021. 3. One of the employees that works for GT Inc. is often required to make special deliveries to clients for rush orders. Although the employee must use his own vehicle, he is generously paid $0.78 per kilometer driven. During the year, the employee drove a total of 3,300 kilometers while delivering products. The allowance paid to the employee was recorded in the other operating expenses account. 4. Bob Green sometimes works from home on the weekends. During this time he often plans for the upcoming week, prepares monthly work schedules for employees, and attends to other business-related matters. The home office occupies 20% of the total floor space of his house. The following annual house costs were paid for during the year by Mr. Green: I. Property taxes Mortgage interest House insurance Utilities V. Repairs and maintenance II. III. IV. $4,000 10,000 1,000 5,000 2.000 Because these costs were paid directly by Mr. Green, none of these amounts were recorded in GT Ltd.'s statement of income. During the week. Bob uses his office located in the back of the store. Paragraph Arrange 5. Since the Kamloops Lawn Bowling Club has been such a good customer ever since Mr. Green started his gardening store, he has become a full-time member of the club. Although the club fees are significant, $2,300 per year, he feels that it is well worth it. He can often attract new customers and boost his sales by bowling with gardening enthusiasts and mingling with the ground keepers who are always on the look out for new lawn and flower varieties for their club grounds. These fees were expensed as other operating expenses. 6. Legal fees include $2,300 paid to a lawyer defending GT against a lawsuit initiated by a client who claims they were seriously injured while pruning a tree with a pair of defective pruning sheers purchased at the store. Because the lawyer feels that the client has a good chance of winning the claim, GT has expensed an amount of $20,000 as a contingent reserve for a possible future payout settlement. 7. The insurance expense account includes premiums of $2.400 paid for a life insurance policy on the life of Mr. Green. The policy is for coverage of $500,000 which was required by the bank as security for a business loan. The insurance account also includes premiums of $4,000 for another life insurance policy in which his wife is named as the beneficiary. 8. Included in the interest and fees account is interest expense of $1.100 paid on a bank loan that was obtained in order to make an interest-free loan to one of the company's employees who was experiencing some financial difficulties. GT Ltd. also had to pay $1,700 in financing fees for preparing and registering the mortgage taken out to finance the purchase of the new building. 9, Accounting fees included $1,800 paid to a local accounting firm for audit and tax services as well as a $320 penalty for failure to prepare the 2019 tax return on time, 10. Advertising and promotion includes an amount of $4,300 paid for the design and i printing of the 2021 seed catalogue which will be sent out to clients in the early spring of 2021. The account also includes $7,000 paid for advertising that aired on American television gardening shows promoting GT Ltd.'s products to the Northwestem US states. 11. The donations account is for amounts that GT Ltd. has given to three registered charitable organizations: Green Peace, Save the Planet, and the Plant a Tree Foundation. Mr. Green feels that these organization share the same ideology and values as he does. He also thinks that the media exposure that he receives from making these generous gifts is good for getting the company's name into the public eye. 12. Mr. Green has gone to three gardening conventions during the year: Costs Meals and entertainment Travel Hotel Convention fee Total #1 $500 1.800 1,400 800 $4.500 #2 $650 2.200 1,800 500 $5.150 #3 $580 5,800 1.600 1.250 59,230 Since convention 3 was held in Cawa and Mr. Green's wife is originally from there. she decided to accompany her husband so that she could visit her family. Half of the travel costs reconfed for convrution 3 was for Mrs. Green's aisfare Because she was 9 40 # F4 144 $ F5 % 5 12. Mr. Green has gone to three gardening conventions during the year: Costs Meals and entertainment Travel Hotel Convention fee Total F6 P e Since convention #3 was held in Ottawa and Mr. Green's wife is originally from there, she decided to accompany her husband so that she could visit her family. Half of the travel costs recorded for convention #3 was for Mrs. Green's airfare. Because she was living with her family while Mr. Green was attending the convention, all other costs relate to Mr. Green. All convention costs were recorded by the bookkeeper in the travel account 6 F7 13. An analysis of the allowance for doubtful accounts by the bookkeeper indicated that a bad debt expense of $15.000 should be recorded for accounting purposes in 2020. Last year, GT Ltd claimed a bad debt reserve of $20,000. This year, the company has determined that a write off of $22,000 is required for bad debts and a reserve of $13,000 should be clauned FB #1 I 14. The cloning inventory was valued by the bookkeeper at the lower of cost and market. The coot was determined using the weighted average method while the market was determined wing the set realizable value method. Became the bookkeeper felt that some of the inventory still on hand was getting old and that it might have to be sold at a loss, he immediately reduced the value of the ending inventory by an $18.000 reserve for oboelete inventory & $500 1,800 1.400 800 $4,500 7 15 is GT Lad's policy to claim a wory serve equal to 1 of sales ($28.500 During the year. $24.800 was speat on repairing os replacing items rensed under waty Reunited F9 DELL * 8 #2 $650 2,200 1,800 500 $5,150 F10 ( 9 #3 5580 5,800 1,600 1.250 $9,230 F11 ) 0 F12 PrtScr T Insert Delete Backspace Required: Calculate GT Ltd.'s net business income for tax purposes for the year ended December 31, 2020. Include any taxable capital gain or allowable capital losses in your reconciliation. When calculating the maximum CCA that the company can claim, also show the ending UCC balances for the year. Sale revenues Cost of goods sold: Inventory, beginning of year Goods purchased during the year Goods available for sale Green Thumb Ltd. Statement of Income Year ended December 31, 2020 Deduct inventory, end of year Cost of goods sold Gross Profit Expenses: Amortization Accounting Legal Interest and fees Insurance Automobile leasing Travel Advertising and promotion Salaries and wages Employee benefits Donations Warranty Bad debt expense Other Operating expenses Total Expenses Operating Income Other pains and losses Gesan on sale of epipment $750,000 1.650.000 2,400,000 600,000 120,000 30,000 36,000 15,000 21.000 18.400 18,880 135,000 300,000 66,000 15.000 28.500 15.000 16.000 $2,850,000 1.800.000 1,050,000 834-780 17,000 1.500 Amortization Accounting Legal Interest and fees Insurance Automobile leasing Travel Advertising and promotion Salaries and wages Employee benefits Donations Warranty Bad debt expense Other Operating expenses Total Expenses Operating Income Other gains and losses: Gain on sale of equipment Loss on sale of computers Income before income taxes Income tax expenses Net Income I 120,000 30,000 36,000 15,000 21,000 18,400 18,880 135,000 300,000 66,000 15,000 28,500 15,000 16,000 834,780 215.220 77,000 1.500 290,720 34,900 $255.820

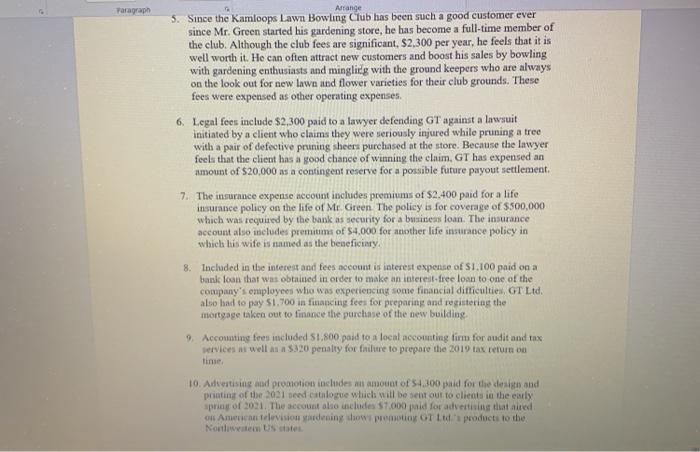

Step by Step Solution

3.33 Rating (159 Votes )

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Horngren, Harrison, Oliver

3rd Edition

978-0132497992, 132913771, 132497972, 132497999, 9780132913775, 978-0132497978