Answered step by step

Verified Expert Solution

Question

1 Approved Answer

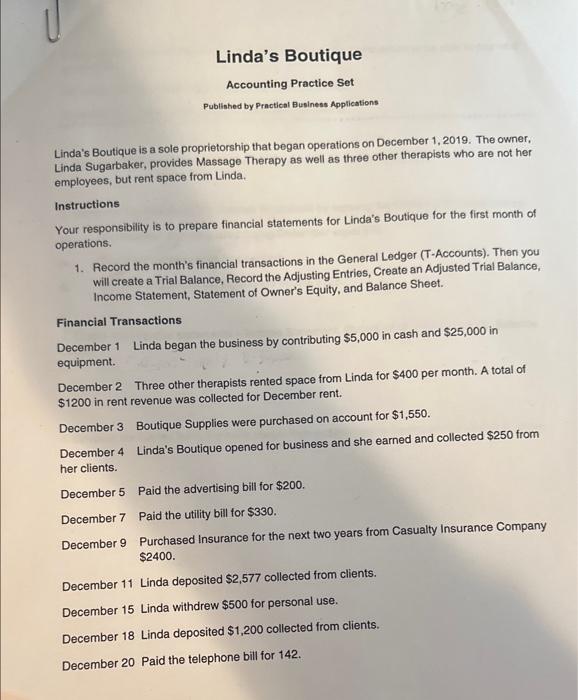

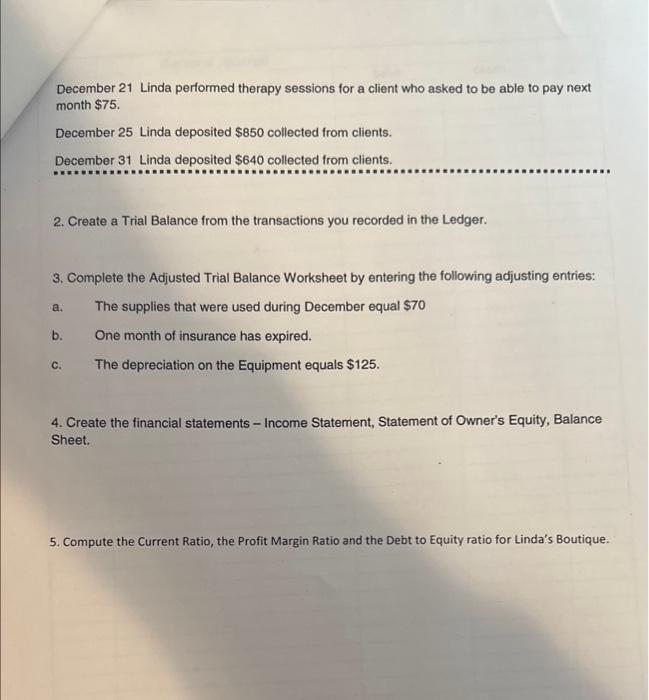

Accounting Practice Set Published by Practical Business Applications Linda's Boutique is a sole proprietorship that began operations on December 1, 2019. The owner, Linda Sugarbaker,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mastering Auditing Essentials A Comprehensive Guide To Learn Auditing Essentials

Authors: Cybellium Ltd, Kris Hermans

1st Edition

B0CHL7H261, 979-8861235617