Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Fabien Ltd is a manufacturing organisation supplying specialised engineered products to a wide range of public and private sector throughout the UK. You are

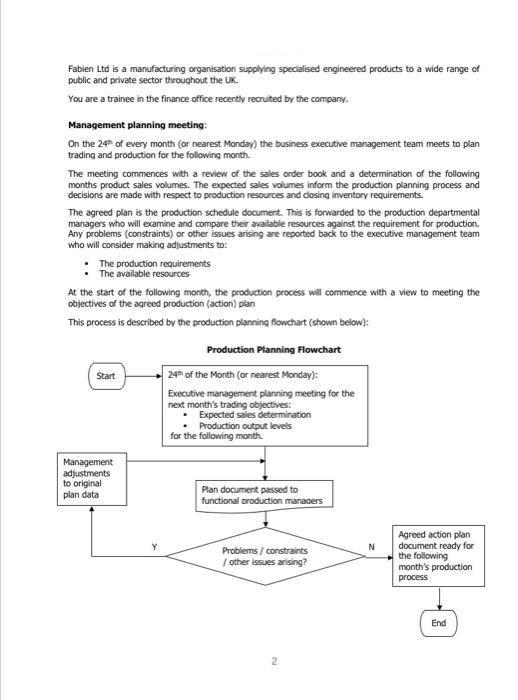

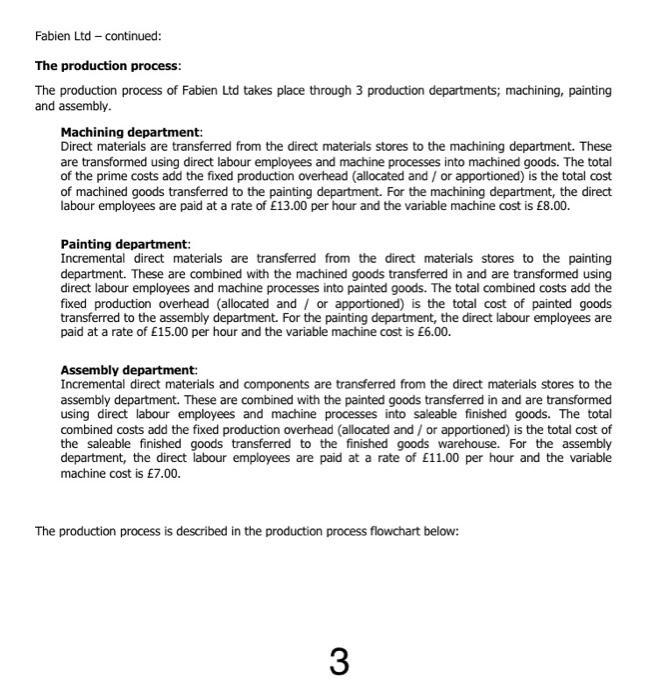

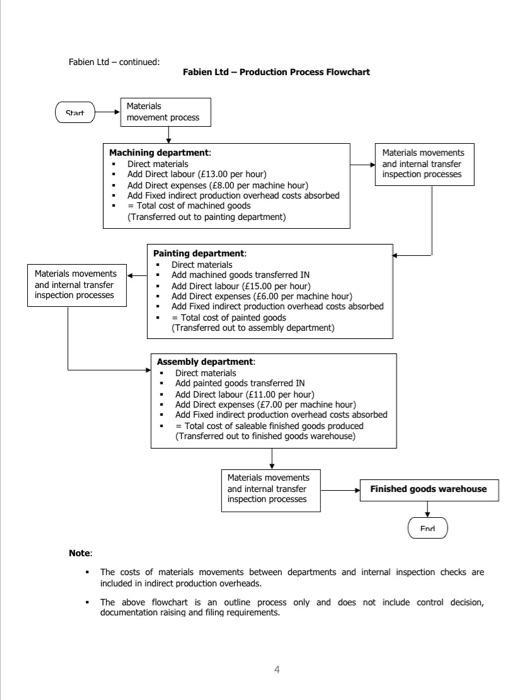

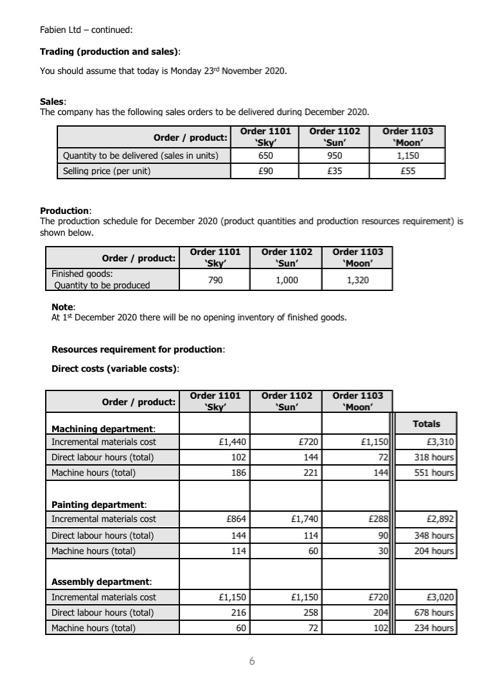

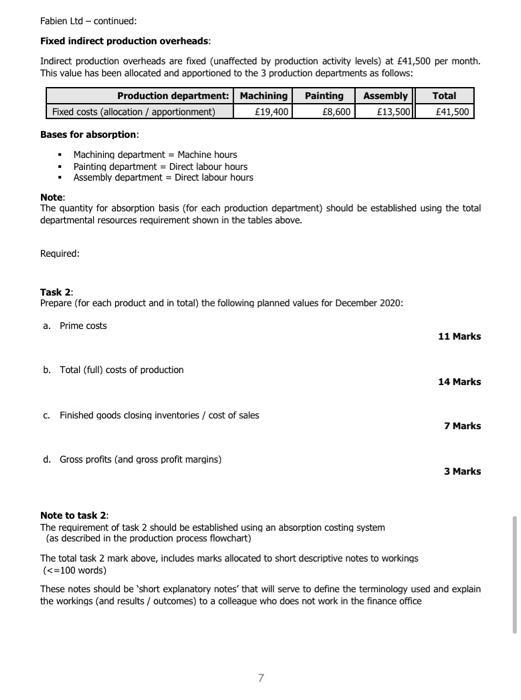

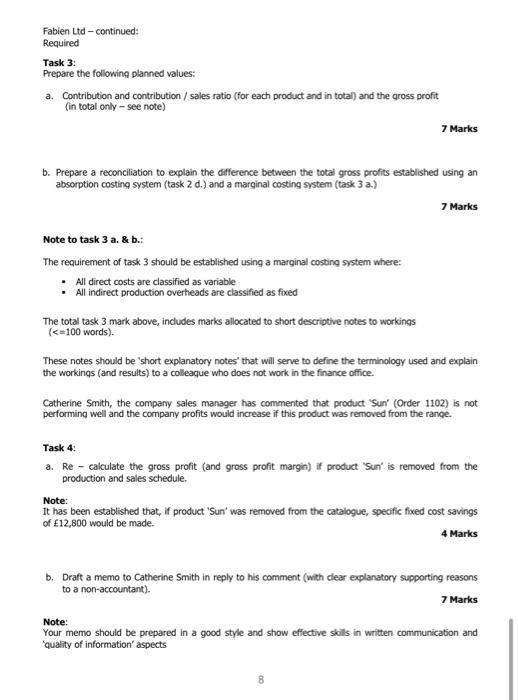

Fabien Ltd is a manufacturing organisation supplying specialised engineered products to a wide range of public and private sector throughout the UK. You are a trainee in the finance office recently recruited by the company. Management planning meeting: On the 24 of every month (or nearest Monday) the business executive management team meets to plan trading and production for the following month. The meeting commences with a review of the sales order book and a determination of the following months product sales volumes. The expected sales volumes inform the production planning process and decisions are made with respect to production resources and dosing inventory requirements. The agreed plan is the production schedule document. This is forwarded to the production departmental managers who will examine and compare their available resources against the requirement for production. Any problems (constraints) or other issues arising are reported back to the executive management team who will consider making adjustments to: The production requirements The available resources At the start of the following month, the production process wil commence with a view to meeting the objectives of the agreed production (action) plan This process is described by the production planning flowchart (shown below): Production Planning Flowchart Start 24t of the Month (or nearest Monday): Executive management planning meeting for the next month's trading objectives: Expected sales determination Production output levels for the following month. Management adjustments to original plan data Plan document passed to functional oroduction managers Agreed action plan document ready for the following month's production process Problems / constraints / other issues arising? End 2 Fabien Ltd continued: The production process: The production process of Fabien Ltd takes place through 3 production departments; machining, painting and assembly. Machining department: Direct materials are transferred from the direct materials stores to the machining department. These are transformed using direct labour employees and machine processes into machined goods. The total of the prime costs add the fixed production overhead (allocated and / or apportioned) is the total cost of machined goods transferred to the painting department. For the machining department, the direct labour employees are paid at a rate of 13.00 per hour and the variable machine cost is 8.00. Painting department: Incremental direct materials are transferred from the direct materials stores to the painting department. These are combined with the machined goods transferred in and are transformed using direct labour employees and machine processes into painted goods. The total combined costs add the fixed production overhead (allocated and / or apportioned) is the total cost of painted goods transferred to the assembly department. For the painting department, the direct labour employees are paid at a rate of 15.00 per hour and the variable machine cost is 6.00. Assembly department: Incremental direct materials and components are transferred from the direct materials stores to the assembly department. These are combined with the painted goods transferred in and are transformed using direct labour employees and machine processes into saleable finished goods. The total combined costs add the fixed production overhead (allocated and / or apportioned) is the total cost of the saleable finished goods transferred to the finished goods warehouse. For the assembly department, the direct labour employees are paid at a rate of 11.00 per hour and the variable machine cost is 7.00. The production process is described in the production process flowchart below: Fabien Ltd - continued: Fabien Ltd - Production Process Flowchart Materials Start movement process Machining department: Direct materials Materials movements and internal transfer inspection processes Add Direct labour (E13.00 per hour) Add Direct expenses (E8.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost of machined goods (Transferred out to painting department) Painting department: Direct materials Add machined goods transferred IN Add Direct labour (E15.00 per hour) Add Direct expenses (6.00 per machine hour) Add Fixed indirect production overhead costs absorbed - Total cost of painted goods (Transferred out to assembly department) Materials movements and internal transfer inspection processes Assembly department: Direct materials Add painted goods transferred IN Add Direct labour (E11.00 per hour) Add Direct expenses (7.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost of saleable finished goods produced (Transferred out to finished goods warehouse) Materials movements and internal transfer Finished goods warehouse inspection processes Frvt Note: The costs of materials movements between departments and internal inspection checks are included in indirect production overheads. The above flowchart is an outline process only and does not include contral decision, documentation raising and filing requirements. 4. Fabien Ltd - continued: Sales Office process: Fabien Ltd is a manufacturer of bespoke products for the building industry and domestic customers. Sales customers place orders either by phone directly to the sales office or through the business website. Sales staff operators well initially cheque whether the customer is an existing account holder. For existing account holders, staff will examine the account to see if there are any existing problems (e.g. long outstanding accounts and / or disputed invoices). Where this is the case, the customer and order information is passed to the chief credit controller for decision-making. Existing customers, where the account is otherwise in good order, most then be checked against current credit limits. Where an order may take the account beyond the current credit limit, the customer and order information is, again, passed to the chief credit controler for decision-making. Where the sales order is acceptable, the order documentation is passed to the production manager for scheduling. Non-existing (new) customers must pay cash in advance of production, and, if this is acceptable to the customer becomes a 'potential' and is offered an application to the sales Ledger. The customer may accept or decline the invitation. An application form is attached to an email and sent to accepting potentials. The contact details of declining potentials will be held anyway for future promotional activities. Required: Task 1: Prepare a flowchart in a A4 size paper (one side only) to describe the sales office process of Fabien Ltd described above. Note: Your flowchart should be prepared in a good style using the Microsoft office Word: "Insert / Shapes / Flowchart' facility (Maximum 20 marks induding 6 marks credit for software use, good style and clear presentation). Fabien Ltd - continued: Trading (production and sales): You should assume that today is Monday 23d November 2020. Sales: The company has the following sales orders to be delivered during December 2020. Order / product: Order 1101 "Sky Order 1102 "Sun' Order 1103 "Moon Quantity to be delivered (sales in units) Selling price (per unit) 650 950 1,150 90 35 55 Production: The production schedule for December 2020 (product quantities and production resources requirement) is shown below. Order 1101 Sky Order 1103 "on" Order 1102 Order / product: Sun Finished goods: Quantity to be produced 790 1,000 1,320 Note: At 1* December 2020 there will be no opening inventory of finished goods. Resources requirement for production: Direct costs (variable costs): Order 1102 Sun Order 1101 Order 1103 Order / product: Sky Moon' Totals Machining department: 1,150 3,310 318 hours Incremental materials cost E1,440 E720 Direct labour hours (total) 102 144 72 Machine hours (total) 186 221 144 551 hours Painting department: Incremental materials cost 864 E1,740 288 2,892 Direct labour hours (total) 90 30 144 114 348 hours Machine hours (total) 114 60 204 hours Assembly department: Incremental materials cost 1,150 E1,150 3,020 720 204 Direct labour hours (total) 216 258 678 hours Machine hours (total) 60 72 102 234 hours 6. Fabien Ltd - continued: Fixed indirect production overheads: Indirect production overheads are fixed (unaffected by production activity levels) at 41,500 per month. This value has been allocated and apportioned to the 3 production departments as follows: Production department: Machining Painting 19,400 Assembly E8,600 Total Fixed costs (allocation / apportionment) E13,500 E41,500 Bases for absorption: Machining department = Machine hours Painting department - Direct labour hours Assembly department = Direct labour hours Note: The quantity for absorption basis (for each production department) should be established using the total departmental resources requirement shown in the tables above. Required: Task 2: Prepare (for each product and in total) the following planned values for December 2020: a. Prime costs 11 Marks b. Total (full) costs of production 14 Marks c. Finished goods dlosing inventories / cost of sales 7 Marks d. Gross profits (and gross profit margins) 3 Marks Note to task 2: The requirement of task 2 should be established using an absorption costing system (as described in the production process flowchart) The total task 2 mark above, includes marks allocated to short descriptive notes to workings ( Fabien Ltd - continued: Required Task 3: Prepare the following planned values: a. Contribution and contribution / sales ratio (for each product and in total) and the gross profit (in total only - see note) 7 Marks b. Prepare a reconciliaion to explain the difference between the total gross profits established using an absorption costing system (task 2 d.) and a marginal costing system (task 3 a.) 7 Marks Note to task 3 a. & b.: The requirement of task 3 should be established using a marginal costing system where: All direct costs are classified as variable All indirect production overheads are classified as fixed The total task 3 mark above, includes marks allocated to short descriptive notes to workings (

Step by Step Solution

★★★★★

3.49 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

ANSWER AND STEP BY STEP EXPLANATION At the start of the month the executive management plan...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Operations And Supply Chain Management

Authors: F. Robert Jacobs, Richard Chase

14th Edition

978-0077824921, 78024021, 9780077823344, 007782492X, 77823346, 978-0078024023