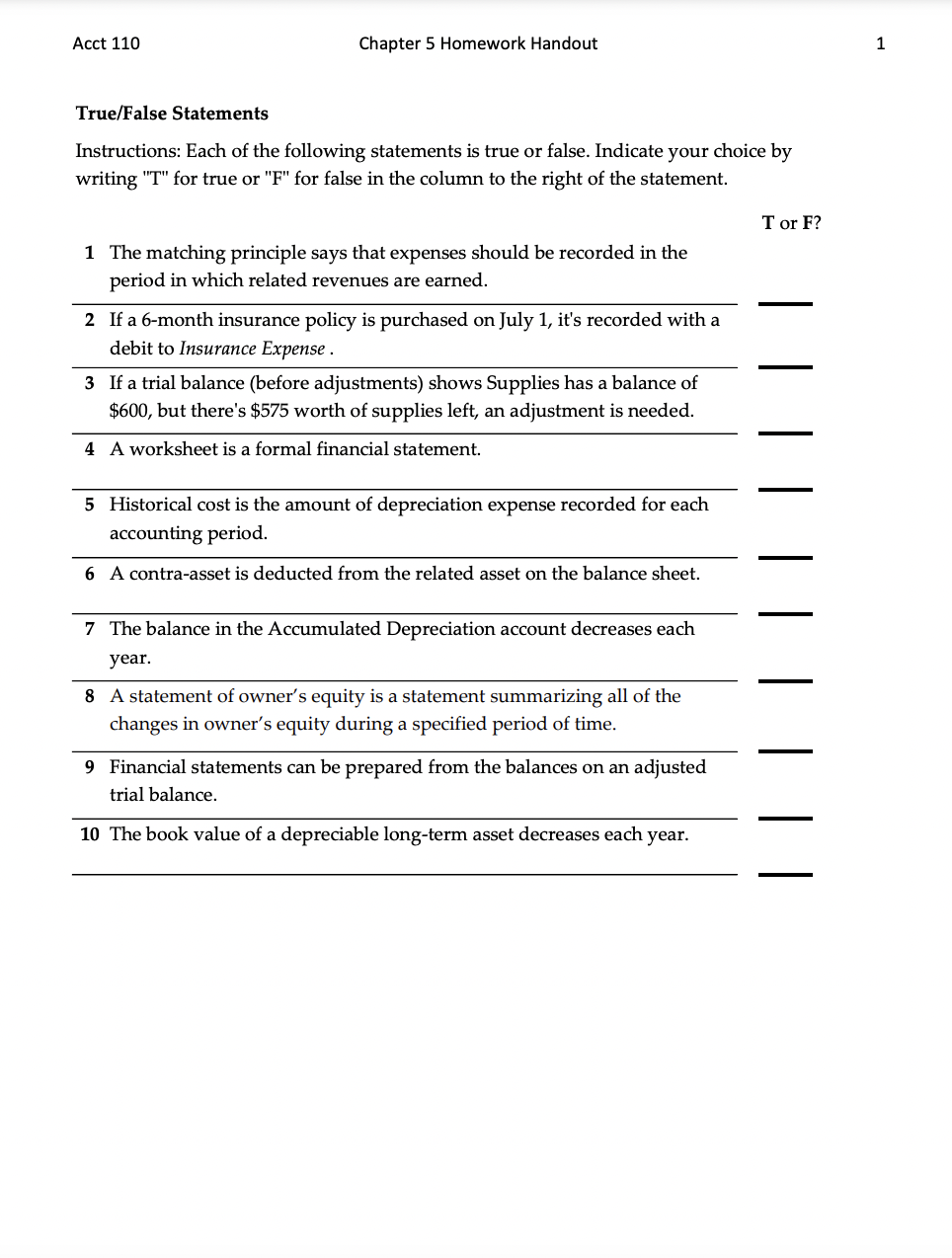

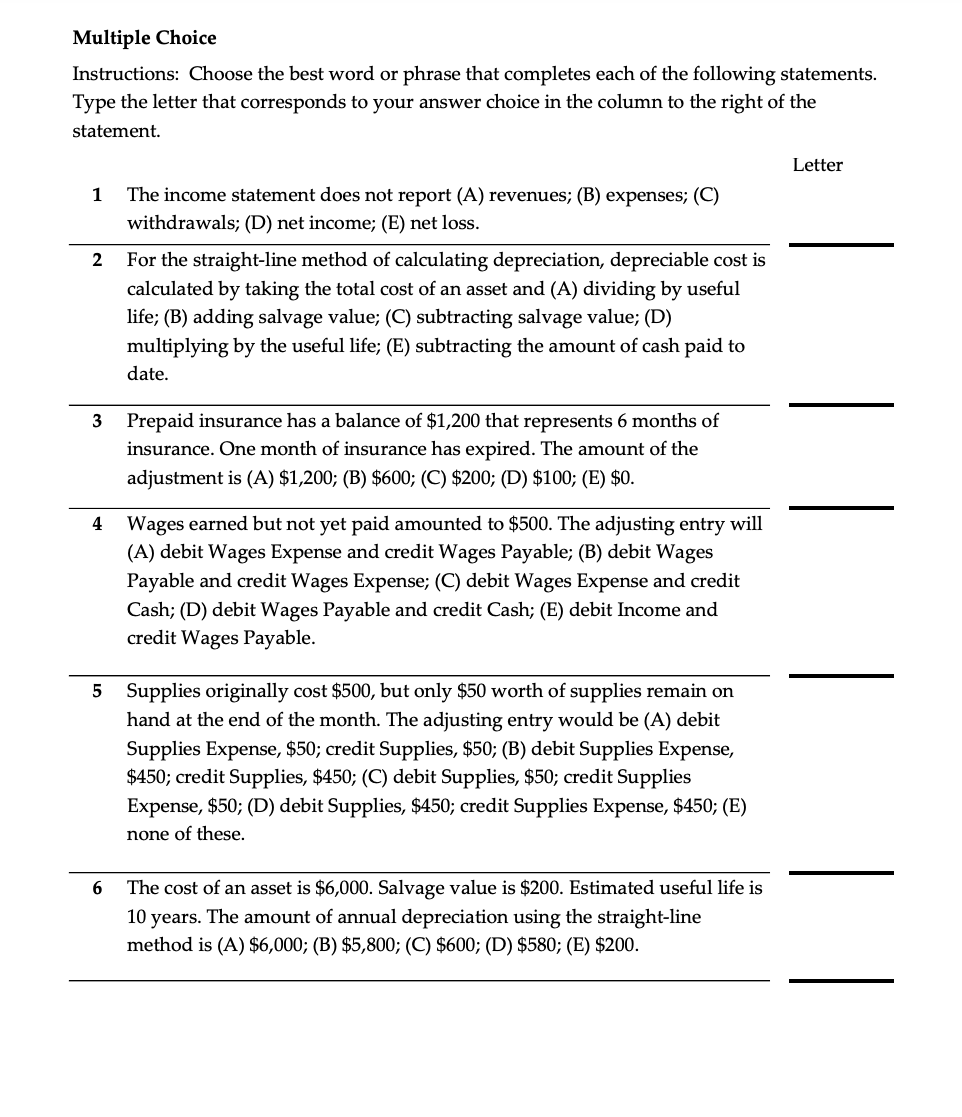

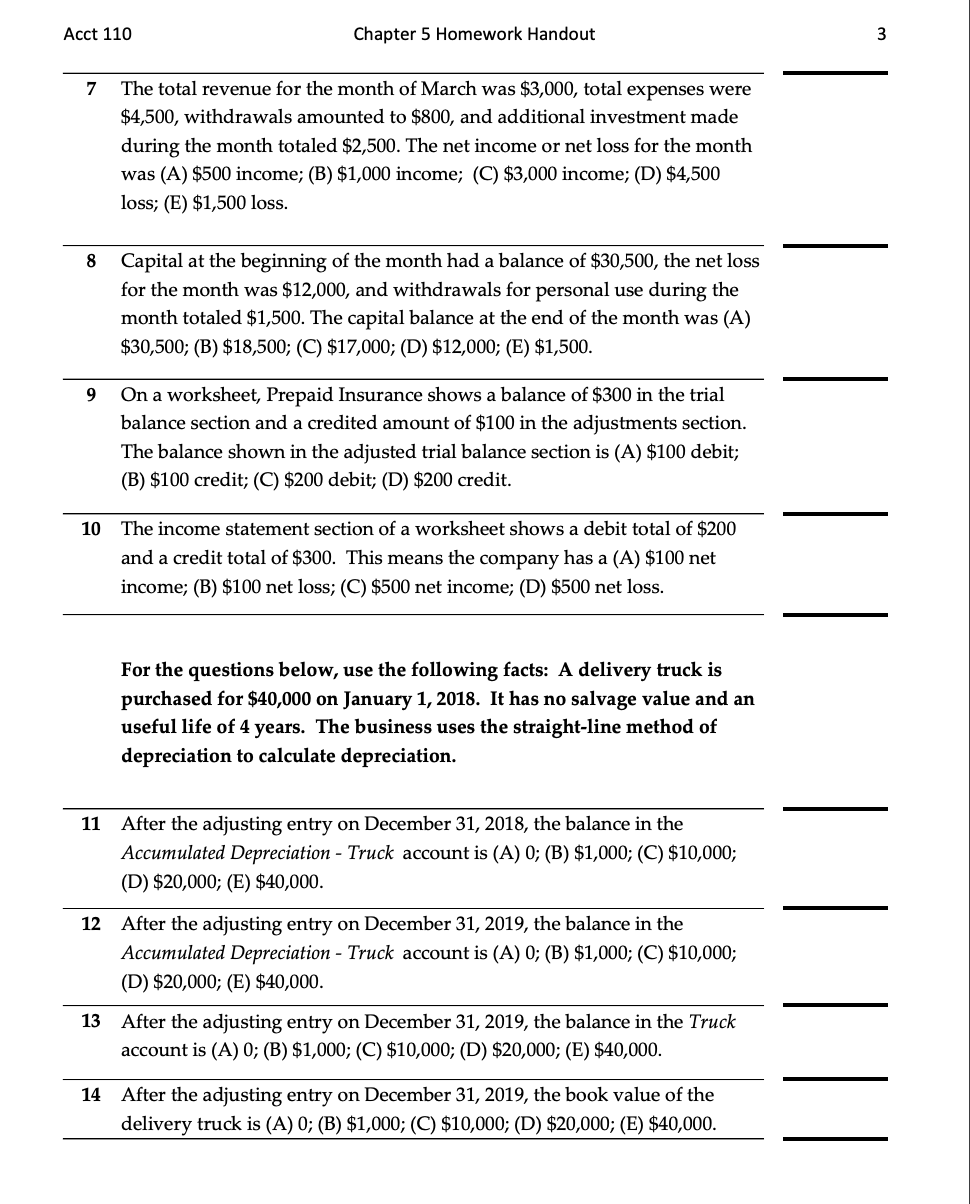

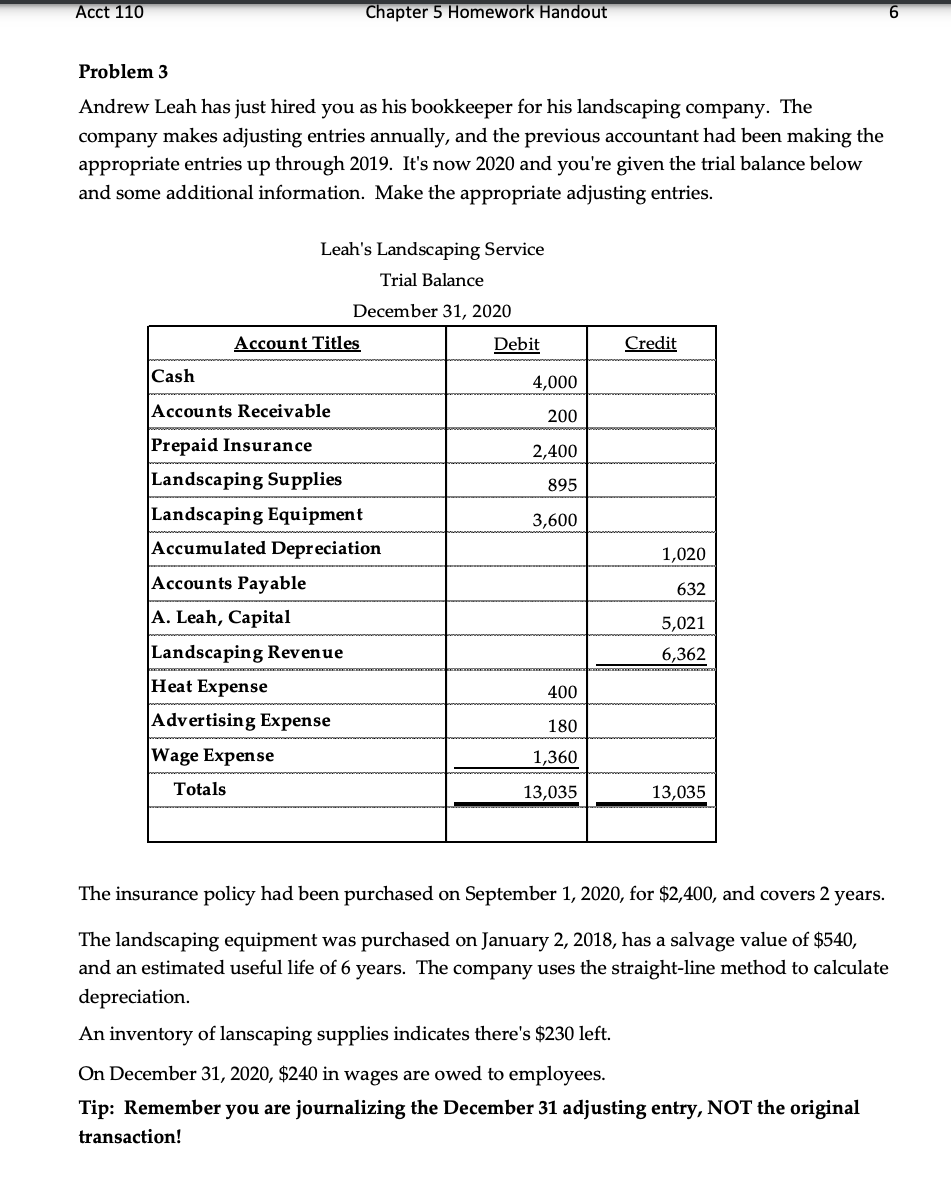

Acct 110 Chapter 5 Homework Handout 1 True/False Statements Instructions: Each of the following statements is true or false. Indicate your choice by writing "T" for true or "F" for false in the column to the right of the statement. Tor F? 1 The matching principle says that expenses should be recorded in the period in which related revenues are earned. 2 If a 6-month insurance policy is purchased on July 1, it's recorded with a debit to Insurance Expense . 3 If a trial balance (before adjustments) shows Supplies has a balance of $600, but there's $575 worth of supplies left, an adjustment is needed. 4 A worksheet is a formal financial statement. 5 Historical cost is the amount of depreciation expense recorded for each accounting period. 6 A contra-asset is deducted from the related asset on the balance sheet. 7 The balance in the Accumulated Depreciation account decreases each year. 8 A statement of owner's equity is a statement summarizing all of the changes in owner's equity during a specified period of time. 9 Financial statements can be prepared from the balances on an adjusted trial balance. 10 The book value of a depreciable long-term asset decreases each year. Multiple Choice Instructions: Choose the best word or phrase that completes each of the following statements. Type the letter that corresponds to your answer choice in the column to the right of the statement. Letter 1 2 The income statement does not report (A) revenues; (B) expenses; (C) withdrawals; (D) net income; (E) net loss. For the straight-line method of calculating depreciation, depreciable cost is calculated by taking the total cost of an asset and (A) dividing by useful life; (B) adding salvage value; (C) subtracting salvage value; (D) multiplying by the useful life; (E) subtracting the amount of cash paid to date. 3 Prepaid insurance has a balance of $1,200 that represents 6 months of insurance. One month of insurance has expired. The amount of the adjustment is (A) $1,200; (B) $600; (C) $200; (D) $100; (E) $0. 4 Wages earned but not yet paid amounted to $500. The adjusting entry will (A) debit Wages Expense and credit Wages Payable; (B) debit Wages Payable and credit Wages Expense; (C) debit Wages Expense and credit Cash; (D) debit Wages Payable and credit Cash; (E) debit Income and credit Wages Payable. 5 Supplies originally cost $500, but only $50 worth of supplies remain on hand at the end of the month. The adjusting entry would be (A) debit Supplies Expense, $50; credit Supplies, $50; (B) debit Supplies Expense, $450; credit Supplies, $450; (C) debit Supplies, $50; credit Supplies Expense, $50; (D) debit Supplies, $450; credit Supplies Expense, $450; (E) none of these. 6 The cost of an asset is $6,000. Salvage value is $200. Estimated useful life is 10 years. The amount of annual depreciation using the straight-line method is (A) $6,000; (B) $5,800; (C) $600; (D) $580; (E) $200. Acct 110 Chapter 5 Homework Handout 3 7 The total revenue for the month of March was $3,000, total expenses were $4,500, withdrawals amounted to $800, and additional investment made during the month totaled $2,500. The net income or net loss for the month was (A) $500 income; (B) $1,000 income; (C) $3,000 income; (D) $4,500 loss; (E) $1,500 loss. 8 Capital at the beginning of the month had a balance of $30,500, the net loss for the month was $12,000, and withdrawals for personal use during the month totaled $1,500. The capital balance at the end of the month was (A) $30,500; (B) $18,500; (C) $17,000; (D) $12,000; (E) $1,500. 9 On a worksheet, Prepaid Insurance shows a balance of $300 in the trial balance section and a credited amount of $100 in the adjustments section. The balance shown in the adjusted trial balance section is (A) $100 debit; (B) $100 credit; (C) $200 debit; (D) $200 credit. 10 The income statement section of a worksheet shows a debit total of $200 and a credit total of $300. This means the company has a (A) $100 net income; (B) $100 net loss; (C) $500 net income; (D) $500 net loss. For the questions below, use the following facts: A delivery truck is purchased for $40,000 on January 1, 2018. It has no salvage value and an useful life of 4 years. The business uses the straight-line method of depreciation to calculate depreciation. 11 After the adjusting entry on December 31, 2018, the balance in the Accumulated Depreciation - Truck account is (A) 0; (B) $1,000; (C) $10,000; (D) $20,000; (E) $40,000. 12 After the adjusting entry on December 31, 2019, the balance in the Accumulated Depreciation - Truck account is (A) 0; (B) $1,000; (C) $10,000; (D) $20,000; (E) $40,000. 13 After the adjusting entry on December 31, 2019, the balance in the Truck account is (A) 0; (B) $1,000; (C) $10,000; (D) $20,000; (E) $40,000. 14 After the adjusting entry on December 31, 2019, the book value of the delivery truck is (A) 0; (B) $1,000; (C) $10,000; (D) $20,000; (E) $40,000. Acct 110 Chapter 5 Homework Handout 4 Problem 1 On January 1, Simms Delivery purchased a truck for $60,000. The truck has an estimated useful life of 5 years and a $10,000 expected salvage value. Simms uses the straight-line method to calculate depreciation. Part A: Journalize the adjusting entry for depreciation for year ended December 31. Use this space to show your calculations. Date Accounts Debit Credit Part B : Compute the book value at the end of the second year of the truck's useful life. Use this space to show your calculations. Acct 110 Chapter 5 Homework Handout 5 Problem 2 Read the description of following adjustments that are required at the end of the accounting period, January 31, for Anise's Repair Services. Journalize the necessary adjusting entries in a general journal. Omit the descriptions. Use standard account titles, like those used in your textbook. 1 2 Prepaid rent for the year on January 1. Rent expired during the month of January, $1,600. Purchased supplies for $4,000 on January 1. Inventory of supplies was $1,200 on January 31. 3 Depreciation is computed using the straight-line method. Equipment purchased on January 1 for $3,000 has an estimated useful life of 5 years with no salvage value. 4 Signed a 3-month contract for $450 prepaid advertising on January 1. Tip: Remember you are journalizing the January 31 adjusting entry, NOT the original transaction! Date Accounts Debit Credit Acct 110 Chapter 5 Homework Handout 6 Problem 3 Andrew Leah has just hired you as his bookkeeper for his landscaping company. The company makes adjusting entries annually, and the previous accountant had been making the appropriate entries up through 2019. It's now 2020 and you're given the trial balance below and some additional information. Make the appropriate adjusting entries. Leah's Landscaping Service Trial Balance December 31, 2020 Account Titles Debit Credit Cash 4,000 Accounts Receivable 200 2,400 895 3,600 1,020 632 Prepaid Insurance Landscaping Supplies Landscaping Equipment Accumulated Depreciation Accounts Payable A. Leah, Capital Landscaping Revenue Heat Expense Advertising Expense Wage Expense Totals 5,021 6,362 400 180 1,360 13,035 13,035 The insurance policy had been purchased on September 1, 2020, for $2,400, and covers 2 years. The landscaping equipment was purchased on January 2, 2018, has a salvage value of $540, and an estimated useful life of 6 years. The company uses the straight-line method to calculate depreciation. An inventory of lanscaping supplies indicates there's $230 left. On December 31, 2020, $240 in wages are owed to employees. Tip: Remember you are journalizing the December 31 adjusting entry, NOT the original transaction! Acct 110 Chapter 5 Homework Handout 7 Problem 3 Journal Template Date Accounts Debit Credit Acct 110 Chapter 5 Homework Handout 8 Problem 4 1 Blanchard's accounting period is one month and records adjusting entries at the end of each month. Read the description of following adjustments that are required at the end of the accounting period, March 31, for Blanchard Consulting Services. Journalize the necessary adjusting entries for the month of March in a general journal. Omit the descriptions. Use standard account titles, like those used in your textbook. A 12-month lease (that means rent) on office space was signed and paid on January 1 for a total of $12,000. 2 Purchased supplies for $4,000 on January 22. Supplies used in March were $300. Depreciation is computed using the straight-line method. Equipment purchased on January 1 for $5,000 has an estimated useful life of 4 years with a residual value of $500. 4 Paid for 6 months of insurance for the company car on January 1. The amount paid was $1,200. 3 5 Employees earned $4,200 in wages at the end of March, but payday isn't until April 2. Tip: Remember you are journalizing the March 31 adjusting entry, NOT the original transaction! Date Accounts Debit Credit