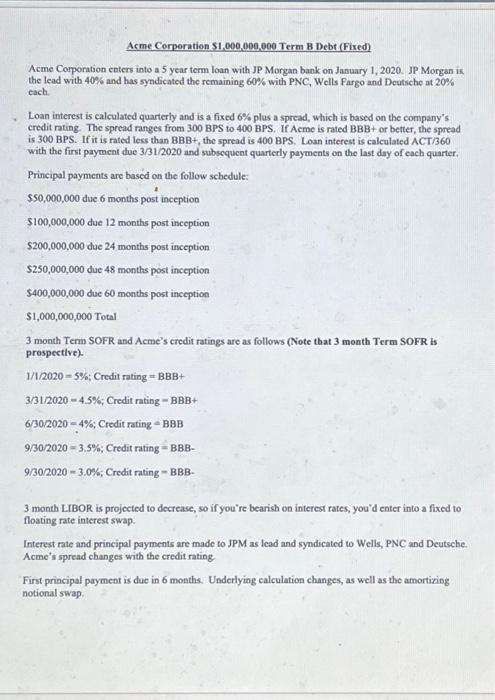

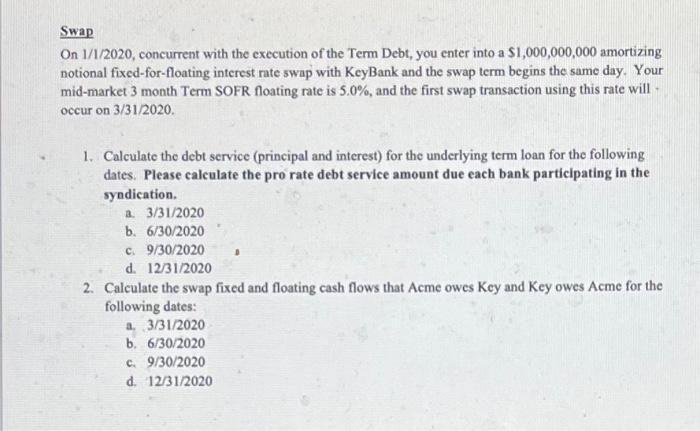

Acme Corporation $1,000,000,000 Term B Debt (Fixed) Acme Corporation enters into a 5 year term loan with JP Morgan bank on January 1, 2020. JP Morgan is the lead with 40% and has syndicated the remaining 60% with PNC, Wells Fargo and Deutsche at 20% each. Loan interest is calculated quarterly and is a fixed 6% plus a spread, which is based on the company's credit rating. The spread ranges from 300BPS to 400BPS. If Acme is rated BBB+ or better, the spread is 300BPS. If it is rated less than BBB+, the spread is 400BPS. Loan interest is calculated ACT/360 with the first payment due 3/31/2020 and subsequent quarterly payments on the last day of each quarter. Principal payments are based on the follow schedule: $50,000,000 due 6 months post inception $100,000,000 due 12 months post inception $200,000,000 due 24 months post inception $250,000,000 due 48 months post inception $400,000,000 due 60 months post inception $1,000,000,000 Total 3 month Term SOFR and Acme's credit ratings are as follows (Note that 3 month Term SOFR is prospectlve). 1/1/2020=5%;Creditrating=BBB+3/31/2020=4.5%;Creditrating=BBB+6/30/2020=4%;Creditrating=BBB9/30/2020=3.5%;Creditrating=BBB-9/30/2020=3.0%;Creditrating=BBB. 3 month LIBOR is projected to decrease, so if you're bearish on interest rates, you'd enter into a fixed to floating rate interest swap. Interest rate and principal payments are made to JPM as lead and syndicated to Wells, PNC and Deutsche. Acme's spread changes with the credit rating First principal payment is due in 6 months. Underlying calculation changes, as well as the amortixing notional swap. On 1/1/2020, concurrent with the execution of the Term Debt, you enter into a $1,000,000,000 amortizing notional fixed-for-floating interest rate swap with KeyBank and the swap term begins the same day. Your mid-market 3 month Term SOFR floating rate is 5.0%, and the first swap transaction using this rate will occur on 3/31/2020. 1. Calculate the debt service (principal and interest) for the underlying term loan for the following dates. Please calculate the pro rate debt service amount due each bank participating in the syndication. a. 3/31/2020 b. 6/30/2020 c. 9/30/2020 d. 12/31/2020 2. Calculate the swap fixed and floating cash flows that Acme owes Key and Key owes Acme for the following dates: a. 3/31/2020 b. 6/30/2020 c. 9/30/2020 d. 12/31/2020 Acme Corporation $1,000,000,000 Term B Debt (Fixed) Acme Corporation enters into a 5 year term loan with JP Morgan bank on January 1, 2020. JP Morgan is the lead with 40% and has syndicated the remaining 60% with PNC, Wells Fargo and Deutsche at 20% each. Loan interest is calculated quarterly and is a fixed 6% plus a spread, which is based on the company's credit rating. The spread ranges from 300BPS to 400BPS. If Acme is rated BBB+ or better, the spread is 300BPS. If it is rated less than BBB+, the spread is 400BPS. Loan interest is calculated ACT/360 with the first payment due 3/31/2020 and subsequent quarterly payments on the last day of each quarter. Principal payments are based on the follow schedule: $50,000,000 due 6 months post inception $100,000,000 due 12 months post inception $200,000,000 due 24 months post inception $250,000,000 due 48 months post inception $400,000,000 due 60 months post inception $1,000,000,000 Total 3 month Term SOFR and Acme's credit ratings are as follows (Note that 3 month Term SOFR is prospectlve). 1/1/2020=5%;Creditrating=BBB+3/31/2020=4.5%;Creditrating=BBB+6/30/2020=4%;Creditrating=BBB9/30/2020=3.5%;Creditrating=BBB-9/30/2020=3.0%;Creditrating=BBB. 3 month LIBOR is projected to decrease, so if you're bearish on interest rates, you'd enter into a fixed to floating rate interest swap. Interest rate and principal payments are made to JPM as lead and syndicated to Wells, PNC and Deutsche. Acme's spread changes with the credit rating First principal payment is due in 6 months. Underlying calculation changes, as well as the amortixing notional swap. On 1/1/2020, concurrent with the execution of the Term Debt, you enter into a $1,000,000,000 amortizing notional fixed-for-floating interest rate swap with KeyBank and the swap term begins the same day. Your mid-market 3 month Term SOFR floating rate is 5.0%, and the first swap transaction using this rate will occur on 3/31/2020. 1. Calculate the debt service (principal and interest) for the underlying term loan for the following dates. Please calculate the pro rate debt service amount due each bank participating in the syndication. a. 3/31/2020 b. 6/30/2020 c. 9/30/2020 d. 12/31/2020 2. Calculate the swap fixed and floating cash flows that Acme owes Key and Key owes Acme for the following dates: a. 3/31/2020 b. 6/30/2020 c. 9/30/2020 d. 12/31/2020