Answered step by step

Verified Expert Solution

Question

1 Approved Answer

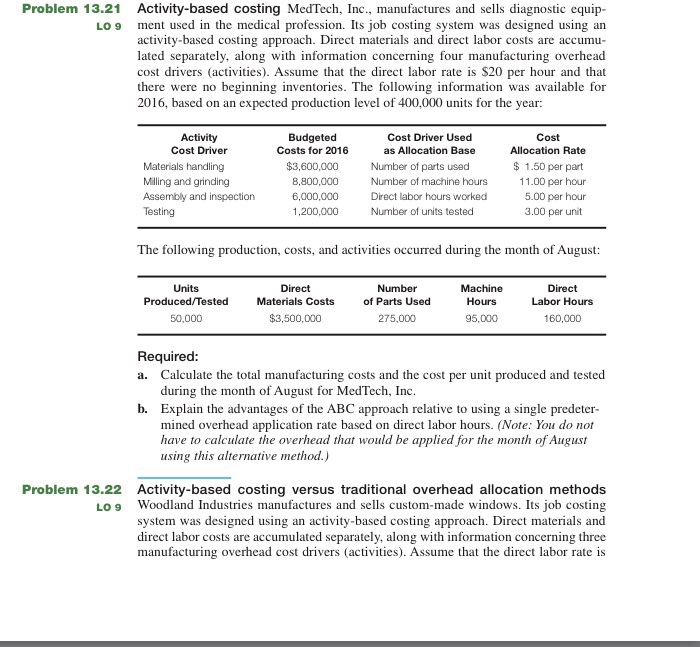

Activity-based costing Med Tech, Inc manufactures and sells diagnostic equip Problem 13.21 Lo 9 ment used in the medical profession. Its job costing system was

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Maintenance Audits Handbook A Performance Measurement Framework

Authors: Diego Galar Pascual, Uday Kumar

1st Edition

1466583916, 978-1466583917