Adjusting entries

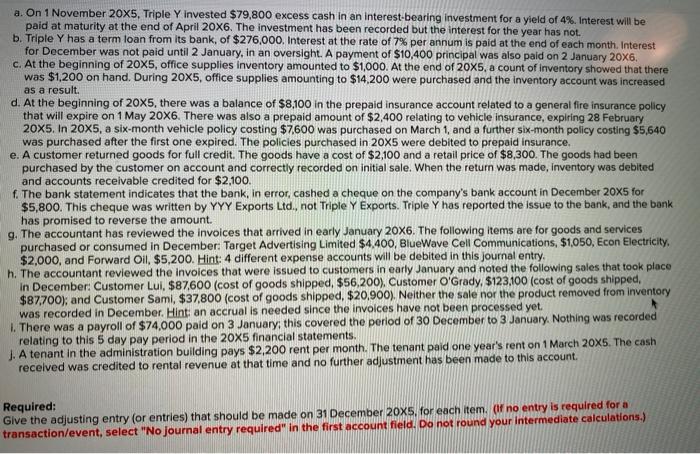

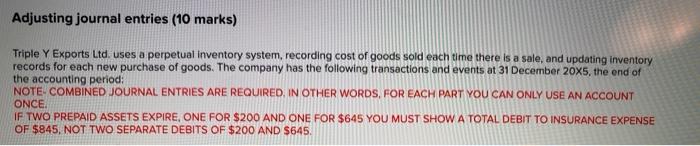

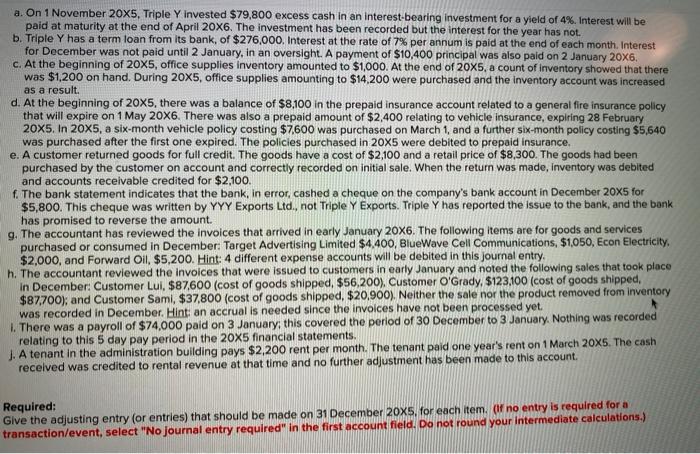

Adjusting journal entries (10 marks) Triple Y Exports Ltd. uses a perpetual inventory system, recording cost of goods sold each time there is a sale, and updating inventory records for each new purchase of goods. The company has the following transactions and events at 31 December 20x5, the end of the accounting period: NOTE-COMBINED JOURNAL ENTRIES ARE REQUIRED. IN OTHER WORDS, FOR EACH PART YOU CAN ONLY USE AN ACCOUNT ONCE IF TWO PREPAID ASSETS EXPIRE, ONE FOR $200 AND ONE FOR $645 YOU MUST SHOW A TOTAL DEBIT TO INSURANCE EXPENSE OF $845, NOT TWO SEPARATE DEBITS OF $200 AND $645. a. On 1 November 20X5, Triple Y invested $79,800 excess cash in an interest-bearing investment for a yield of 4%. Interest will be paid at maturity at the end of April 20X6. The investment has been recorded but the interest for the year has not. b. Triple Y has a term loan from its bank, of $276,000. Interest at the rate of 7% per annum is paid at the end of each month. Interest for December was not paid until 2 January, in an oversight. A payment of $10,400 principal was also paid on 2 January 20x6. c. At the beginning of 20X5, office supplies inventory amounted to $1,000. At the end of 20x5, a count of inventory showed that there was $1,200 on hand. During 20x5, office supplies amounting to $14,200 were purchased and the inventory account was increased as a result. d. At the beginning of 20X5, there was a balance of $8,100 in the prepaid insurance account related to a general fire insurance policy that will expire on 1 May 20X6. There was also a prepaid amount of $2,400 relating to vehicle insurance, expiring 28 February 20x5. In 20x5, a six-month vehicle policy costing $7.600 was purchased on March 1, and a further six-month policy costing $5,640 was purchased after the first one expired. The policies purchased in 20x5 were debited to prepaid insurance, e. A customer returned goods for full credit. The goods have a cost of $2,100 and a retail price of $8,300. The goods had been purchased by the customer on account and correctly recorded on initial sale. When the return was made, Inventory was debited and accounts receivable credited for $2,100. f. The bank statement indicates that the bank, in error, cashed a cheque on the company's bank account in December 20x5 for $5,800. This cheque was written by YYY Exports Ltd., not Triple Y Exports. Triple Y has reported the issue to the bank, and the bank has promised to reverse the amount. g. The accountant has reviewed the invoices that arrived early January 20X6. The foll ving items are for goods and services purchased or consumed in December: Target Advertising Limited $4,400, BlueWave Cell Communications, $1,050, Econ Electricity $2,000, and Forward Oil, $5,200. Hint: 4 different expense accounts will be debited in this journal entry. h. The accountant reviewed the invoices that were issued to customers in early January and noted the following sales that took place in December: Customer Lui, $87,600 (cost of goods shipped, $56,200). Customer O'Grady, $123,100 (cost of goods shipped, $87,700); and Customer Sami, $37,800 (cost of goods shipped, $20,900). Neither the sale nor the product removed from inventory was recorded in December. Hint: an accrual is needed since the invoices have not been processed yet. 1. There was a payroll of $74,000 paid on 3 January, this covered the period of 30 December to 3 January. Nothing was recorded relating to this 5 day pay period in the 20x5 financial statements. J. A tenant in the administration building pays $2,200 rent per month. The tenant paid one year's rent on 1 March 20x6. The cash received was credited to rental revenue at that time and no further adjustment has been made to this account. Required: Give the adjusting entry (or entries) that should be made on 31 December 20x5, for each item. Of no entry is required for a transaction/event, select "No journal entry required" in the first account field. Do not round your intermediate calculations.)