Advanced performance management

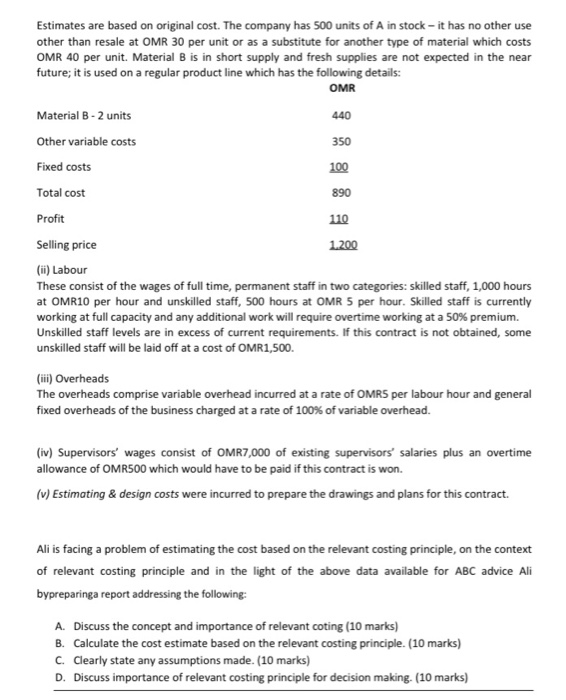

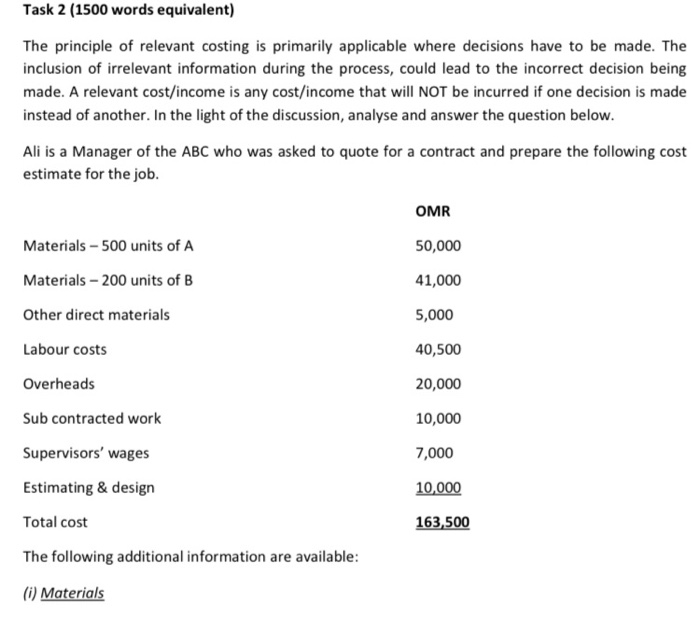

Task 2 (1500 words equivalent) The principle of relevant costing is primarily applicable where decisions have to be made. The inclusion of irrelevant information during the process, could lead to the incorrect decision being made. A relevant cost/income is any cost/income that will NOT be incurred if one decision is made instead of another. In the light of the discussion, analyse and answer the question below. Ali is a Manager of the ABC who was asked to quote for a contract and prepare the following cost estimate for the job. OMR 50,000 41,000 5,000 40,500 20,000 Materials - 500 units of A Materials - 200 units of B Other direct materials Labour costs Overheads Sub contracted work Supervisors' wages Estimating & design Total cost The following additional information are available: 10,000 7,000 10,000 163,500 (i) Materials Estimates are based on original cost. The company has 500 units of A in stock - it has no other use other than resale at OMR 30 per unit or as a substitute for another type of material which costs OMR 40 per unit. Material B is in short supply and fresh supplies are not expected in the near future; it is used on a regular product line which has the following details: OMR Material B-2 units 440 Other variable costs 350 Fixed costs 100 Total cost 890 Profit 110 Selling price 1.200 (ii) Labour These consist of the wages of full time, permanent staff in two categories: skilled staff, 1,000 hours at OMR10 per hour and unskilled staff, 500 hours at OMR 5 per hour. Skilled staff is currently working at full capacity and any additional work will require overtime working at a 50% premium. Unskilled staff levels are in excess of current requirements. If this contract is not obtained, some unskilled staff will be laid off at a cost of OMR1,500. (iii) Overheads The overheads comprise variable overhead incurred at a rate of OMR5 per labour hour and general fixed overheads of the business charged at a rate of 100% of variable overhead. (iv) Supervisors' wages consist of OMR7,000 of existing supervisors' salaries plus an overtime allowance of OMR500 which would have to be paid if this contract is won. (v) Estimating & design costs were incurred to prepare the drawings and plans for this contract. Ali is facing a problem of estimating the cost based on the relevant costing principle, on the context of relevant costing principle and in the light of the above data available for ABC advice Ali bypreparinga report addressing the following: A. Discuss the concept and importance of relevant coting (10 marks) B. Calculate the cost estimate based on the relevant costing principle. (10 marks) C. Clearly state any assumptions made. (10 marks) D. Discuss importance of relevant costing principle for decision making. (10 marks) Task 2 (1500 words equivalent) The principle of relevant costing is primarily applicable where decisions have to be made. The inclusion of irrelevant information during the process, could lead to the incorrect decision being made. A relevant cost/income is any cost/income that will NOT be incurred if one decision is made instead of another. In the light of the discussion, analyse and answer the question below. Ali is a Manager of the ABC who was asked to quote for a contract and prepare the following cost estimate for the job. OMR 50,000 41,000 5,000 40,500 20,000 Materials - 500 units of A Materials - 200 units of B Other direct materials Labour costs Overheads Sub contracted work Supervisors' wages Estimating & design Total cost The following additional information are available: 10,000 7,000 10,000 163,500 (i) Materials Estimates are based on original cost. The company has 500 units of A in stock - it has no other use other than resale at OMR 30 per unit or as a substitute for another type of material which costs OMR 40 per unit. Material B is in short supply and fresh supplies are not expected in the near future; it is used on a regular product line which has the following details: OMR Material B-2 units 440 Other variable costs 350 Fixed costs 100 Total cost 890 Profit 110 Selling price 1.200 (ii) Labour These consist of the wages of full time, permanent staff in two categories: skilled staff, 1,000 hours at OMR10 per hour and unskilled staff, 500 hours at OMR 5 per hour. Skilled staff is currently working at full capacity and any additional work will require overtime working at a 50% premium. Unskilled staff levels are in excess of current requirements. If this contract is not obtained, some unskilled staff will be laid off at a cost of OMR1,500. (iii) Overheads The overheads comprise variable overhead incurred at a rate of OMR5 per labour hour and general fixed overheads of the business charged at a rate of 100% of variable overhead. (iv) Supervisors' wages consist of OMR7,000 of existing supervisors' salaries plus an overtime allowance of OMR500 which would have to be paid if this contract is won. (v) Estimating & design costs were incurred to prepare the drawings and plans for this contract. Ali is facing a problem of estimating the cost based on the relevant costing principle, on the context of relevant costing principle and in the light of the above data available for ABC advice Ali bypreparinga report addressing the following: A. Discuss the concept and importance of relevant coting (10 marks) B. Calculate the cost estimate based on the relevant costing principle. (10 marks) C. Clearly state any assumptions made. (10 marks) D. Discuss importance of relevant costing principle for decision making. (10 marks)