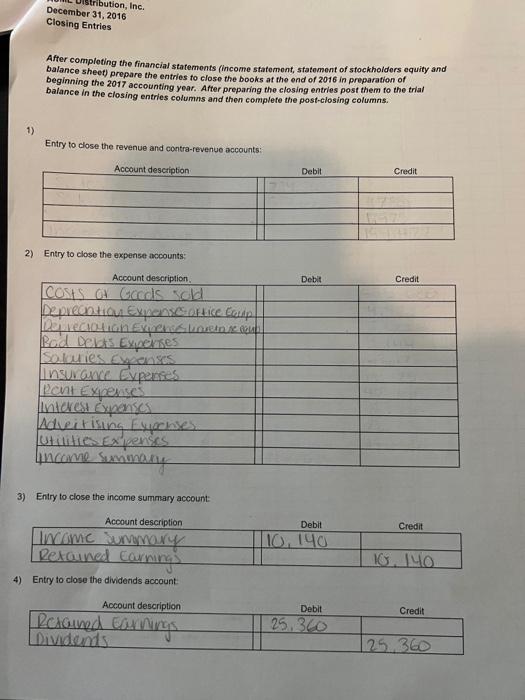

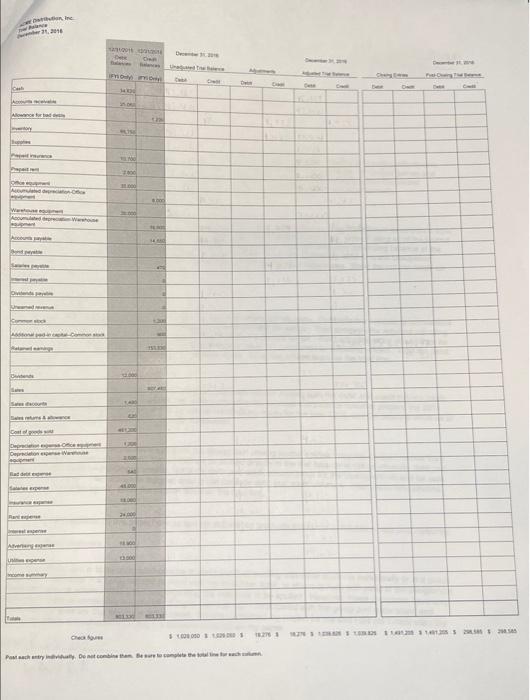

After completeing the financial statements (income statement, statement of stockholders equity and balance sheet) prepare the entries for close the books at the end of 2016 in preparation of beginning the 2017 accounting year. After preparing the closing entries post them to the trial balance in the closing entries columns and then complete the post-closing columns.

These are the problems I have filled out. I need help filling out the 2016 values and the closing entries sheet. I'm also not sure if the boxes I have filled in on the closing entries sheet are right.. I also need help with the trial balance sheet too please.

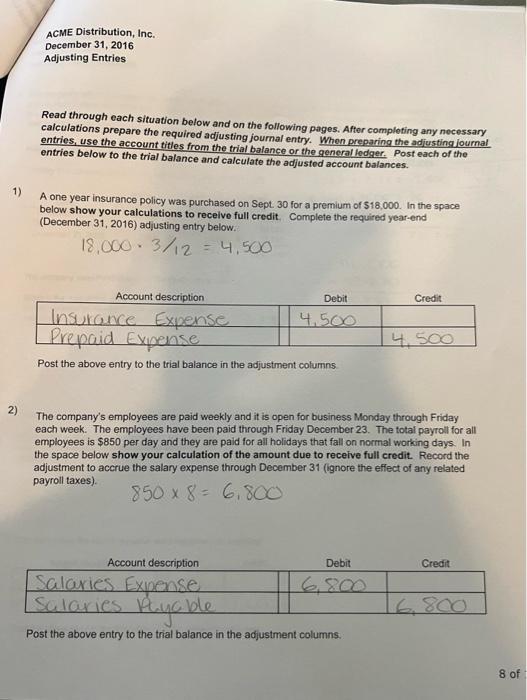

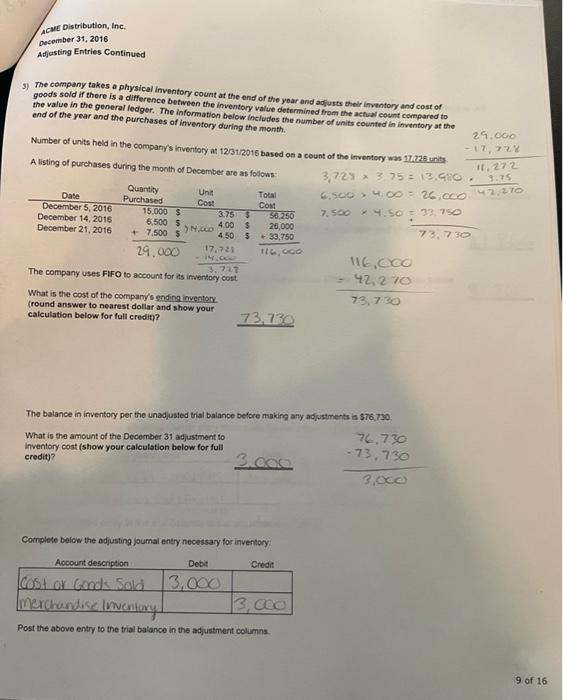

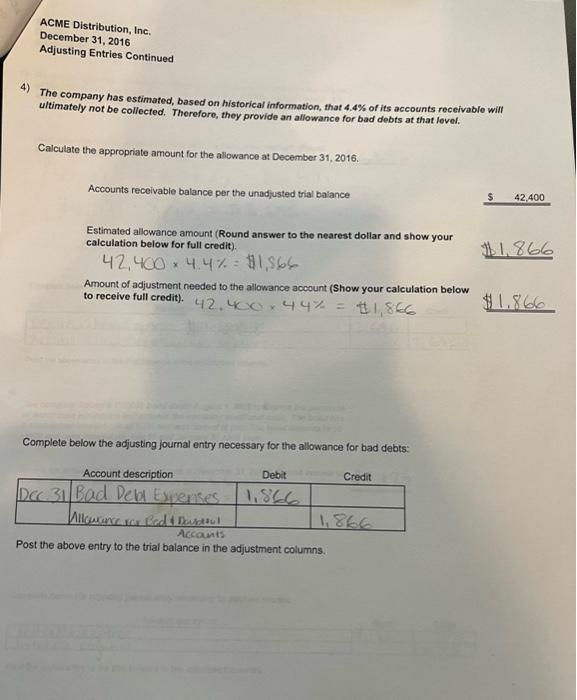

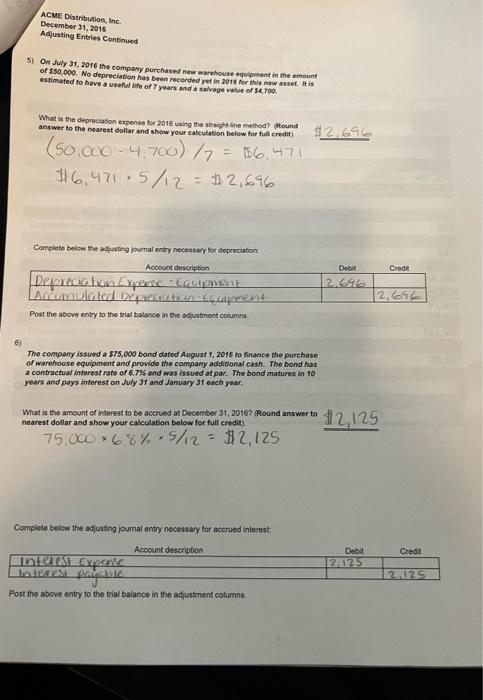

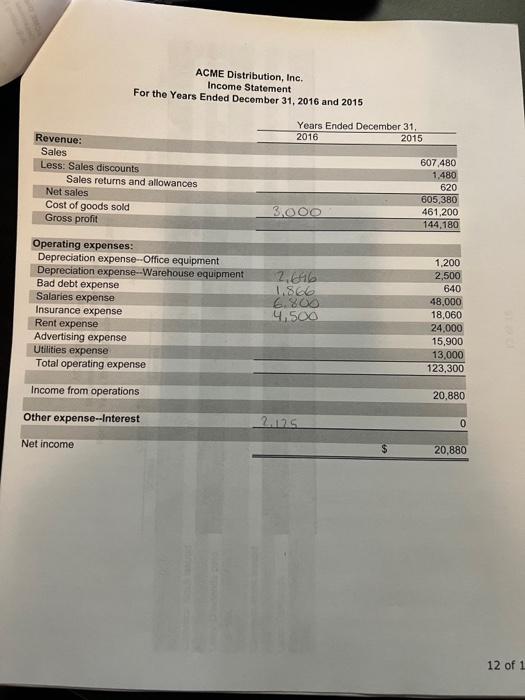

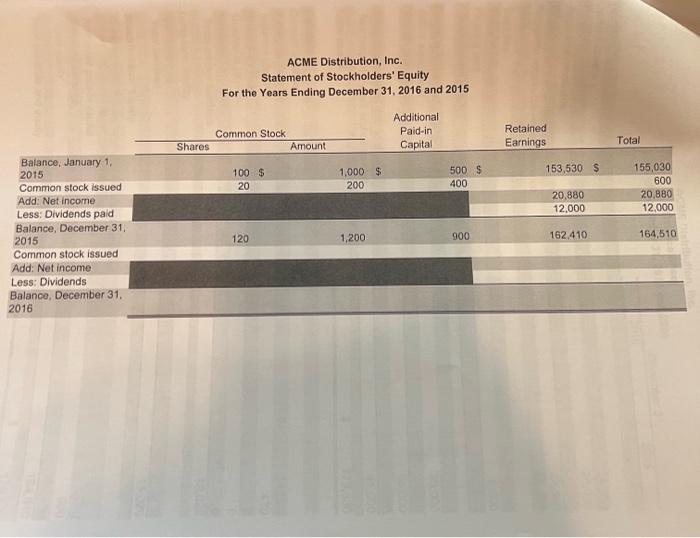

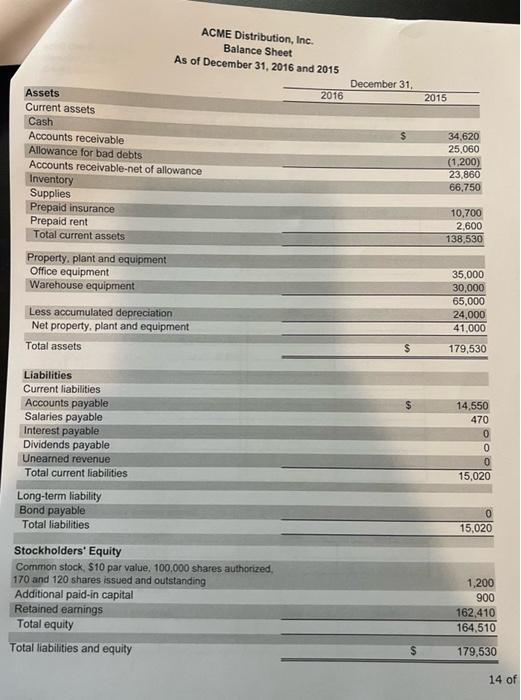

ACME Distribution, Inc. December 31, 2016 Adjusting Entries Read through each situation below and on the following pages. After completing any necessary calculations prepare the required adjusting journal entry. When preparing the adjusting journal entries, use the account titles from the trial balance or the general ledger. Post each of the entries below to the trial balance and calculate the adjusted account balances. 1) A one year insurance policy was purchased on Sept. 30 for a premium of $18,000. In the space below show your calculations to receive full credit. Complete the required year-end (December 31, 2016) adjusting entry below. 18,000 - 3/12 = 4,500 Account description Debit Credit 4,500 Insurance Expense Prepaid Expense 4,500 Post the above entry to the trial balance in the adjustment columns 2) The company's employees are paid weekly and it is open for business Monday through Friday each week. The employees have been paid through Friday December 23. The total payroll for all employees is $850 per day and they are paid for all holidays that fall on normal working days. In the space below show your calculation of the amount due to receive full credit. Record the adjustment to accrue the salary expense through December 31 (ignore the effect of any related payroll taxes). 850 x 8 = 6,800 Account description Debit Credit Salaries Expense Salaries Payable 16,800 6.800 Post the above entry to the trial balance in the adjustment columns. 8 of ACME Distribution, Inc. December 31, 2016 Adjusting Entries Continued 3) The company takes a physical inventory count at the end of the year and adjusts their inventory and cost of goods sold if there is a difference between the inventory value determined from the actual count compared to the value in the general ledger. The information below includes the number of units counted in inventory at the end of the year and the purchases of inventory during the month. Number of units held in the company's inventory at 12/31/2016 based on a count of the inventory was 17.728 units 29.000 -17,72% 11,272 A listing of purchases during the month of December are as follows: 3,72% x 375 = 13.980. 3.75 42,270 Quantity Purchased Unit Total Date .500 4.00= 26,000 Cost Cost December 5, 2016 15,000 $ 7.500x4.50 = 33, 750 3.75 $ December 14, 2016 December 21, 2016 6,500 $ +7,500 $ N.000 4.00 4.50 73,730 29,000 17,721 116,000 3.722 The company uses FIFO to account for its inventory cost = 42,270 73,7:30 What is the cost of the company's ending inventory. (round answer to nearest dollar and show your calculation below for full credit)? 73,730 The balance in inventory per the unadjusted trial balance before making any adjustments is $76,730. 76.730 What is the amount of the December 31 adjustments inventory cost (show your calculation below for full credit)? -73,730 3.000 3,000 Complete below the adjusting journal entry necessary for inventory: Account description Debit Credit Cost or Gonds Sold 3,000 Merchandise Inventory! 3,000 Post the above entry to the trial balance in the adjustment columns 56.250 26,000 $ $33,750 116,000 9 of 16 ACME Distribution, Inc. December 31, 2016 Adjusting Entries Continued 4) The company has estimated, based on historical information, that 4.4% of its accounts receivable will ultimately not be collected. Therefore, they provide an allowance for bad debts at that level. Calculate the appropriate amount for the allowance at December 31, 2016. Accounts receivable balance per the unadjusted trial balance $ 42,400 Estimated allowance amount (Round answer to the nearest dollar and show your calculation below for full credit). $1.866 42,400 4.4% = $1,566 x Amount of adjustment needed to the allowance account (Show your calculation below to receive full credit). 42.400 44% = $1.866 X #1,866 Complete below the adjusting journal entry necessary for the allowance for bad debts: Account description Debit Credit Dec 31 Bad Dell Expenses 1,866 Alloucence for Bed & Devattul 1,866 Accounts Post the above entry to the trial balance in the adjustment columns. ACME Distribution, Inc. December 31, 2016 Adjusting Entries Continued 5) On July 31, 2016 the company purchased new warehouse equipment in the amount of $50,000. No depreciation has been recorded yet in 2016 for this new asset. It is estimated to have a useful life of 7 years and a salvage value of $4,700. What is the depreciation expense for 2016 using the straight-line method? (Round answer to the nearest dollar and show your calculation below for full credit) (50.000-4.700)/7 = $6.471 $6,471 5/12 = #2,696 Y Complete below the adjusting journal entry necessary for depreciation Account description Depreciation Experce-Equipment Accumulated Depresication Equipment Post the above entry to the trial balance in the adjustment columns The company issued a $75,000 bond dated August 1, 2016 to finance the purchase of warehouse equipment and provide the company additional cash. The bond has a contractual interest rate of 6.7% and was issued at par. The bond matures in 10 years and pays interest on July 31 and January 31 each year. What is the amount of interest to be accrued at December 31, 20167 (Round answer to nearest dollar and show your calculation below for full credit) . 75,000 * 6.8% 5/12 = $2,125 y Complete below below the adjusting journal entry necessary for accrued interest Account description [interest Expensic able Post the above entry to the trial balance in the adjustment columns $2,696 Debit 12.696 Credit 2,696 $2,125 Debit 2.125 Credit 2.125 ACME Distribution, Inc. Income Statement For the Years Ended December 31, 2016 and 2015 Revenue: Sales Less: Sales discounts Sales returns and allowances Net sales Cost of goods sold Gross profit Operating expenses: Depreciation expense-Office equipment Depreciation expense-Warehouse equipment Bad debt expense Salaries expense Insurance expense Rent expense Advertising expense Utilities expense Total operating expense Income from operations Other expense-Interest Net income Years Ended December 31, 2016 2015 3,000 2.6416 1.866 6.800 4,500 2.125 607,480 1,480 620 605,380 461,200 144,180 1,200 2,500 640 48,000 18,060 24,000 15,900 13,000 123,300 20,880 0 20,880 12 of 1 ACME Distribution, Inc. Statement of Stockholders' Equity For the Years Ending December 31, 2016 and 2015 Common Stock Shares Amount Additional Pald-in Capital Retained Earnings Total 153,530 $ 100 $ 20 1,000 $ 200 500 S 400 155,030 600 20,880 12,000 20,880 12.000 Balance, January 1, 2015 Common stock issued Add: Net income Less: Dividends paid Balance, December 31 2015 Common stock issued Add: Net income Less: Dividends Balance, December 31, 2016 120 1,200 900 162.410 164,510 ACME Distribution, Inc. Balance Sheet As of December 31, 2016 and 2015 2016 Assets Current assets Cash Accounts receivable Allowance for bad debts Accounts receivable-net of allowance Inventory Supplies Prepaid insurance Prepaid rent Total current assets. Property, plant and equipment Office equipment Warehouse equipment Less accumulated depreciation Net property, plant and equipment Total assets Liabilities Current liabilities Accounts payable Salaries payable Interest payable Dividends payable Unearned revenue Total current liabilities Long-term liability Bond payable Total liabilities Stockholders' Equity Common stock, $10 par value, 100,000 shares authorized, 170 and 120 shares issued and outstanding Additional paid-in capital Retained earnings Total equity Total liabilities and equity December 31, $ 2015 34,620 25,060 (1,200) 23,860 66,750 10,700 2,600 138,530 35,000 30,000 65,000 24,000 41,000 179,530 14,550 470 0 0 0 15,020 15,020 1,200 900 162,410 164,510 179,530 14 of stribution, Inc. December 31, 2016 Closing Entries After completing the financial statements (income statement, statement of stockholders equity and balance sheet) prepare the entries to close the books at the end of 2016 in preparation of beginning the 2017 accounting year. After preparing the closing entries post them to the trial balance in the closing entries columns and then complete the post-closing columns. 1) Entry to close the revenue and contra-revenue accounts: Account description Debit Credit 2) Entry to close the expense accounts: Debit Credit Account description costs or Goods sold Deprecation Expenses oftice Coup Davidian Eve Losto de ROL DELS Expenses Soluties coses Insurance Evperses Pont Expense Latest expenses Advertising wees income Swinan 3) Entry to close the income summary account: Account description Debit Credit Income Summary Retained carming 110, 140 16. NO 4) Entry to close the dividends account Account description Debit Credit Beauverd waarines 25.300 Dividends 125.360 Ca pabution, Inc. Balance 21, 2016 JA Allowance for ad p insurance Prop O Accumulated datin pent Warehouse en Accumulated deprem Warehouse Accounts paya p Sa Dividend pay Co ends -Co Sales Sedcourts retum &alowance Cost of E Depreciation expec Depreciation expense opment ad de exper expense 201 De IFY Day 34830 25.0 MOSE 1700 2800 31000 3000 12.000 14 Balanc 4000 14 A LER SLIDE NOT A 420 2000 SA 41.000 24,000 Rant expe per 100 Atvenergexenas 13000 Us expense come summary MILK Check ques Postachentry individually. Do not combine them Be sure to complete the De $10080001526 O 3 Ow Den ONN D Pt-Ching The 18.275 182N 3 AZMANTOMES $14012052208585