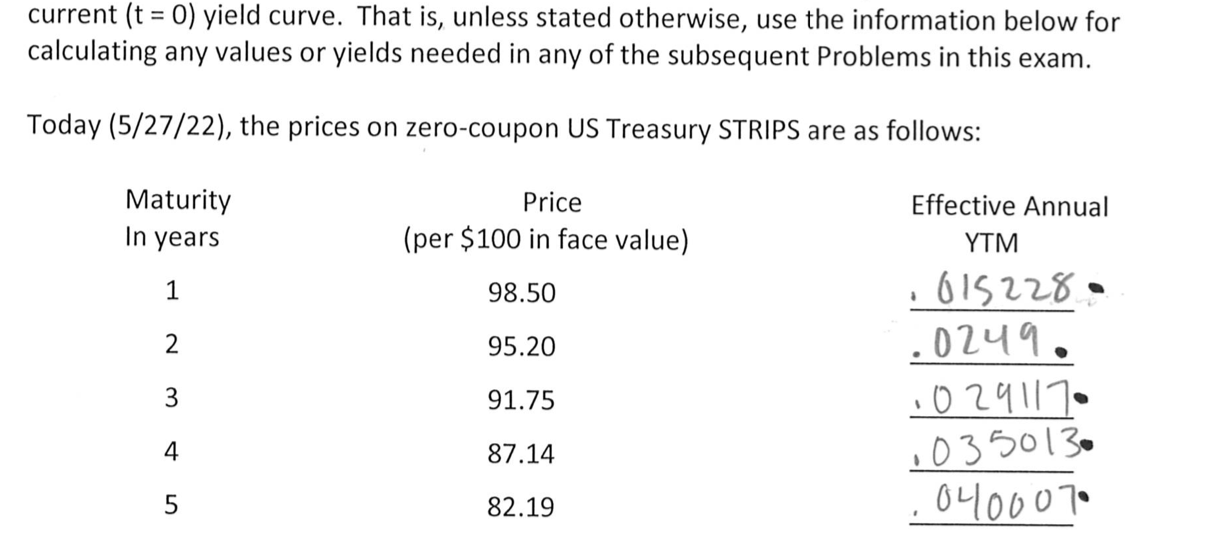

Again, use the data on the current yield curve from Problem 2. Steve Inc. has someone (Steve) in it's treasury department who thinks he can exploit some mis- pricings in the bond market. On behalf of Steve Inc., Steve issues one thousand (1000) 2-year two-percent annual pay coupon bonds, each with a face value of $1000; each of the 1000 bonds pays its 2% coupons once a year (at the end of the year). The market perceives that Steve Inc. has no risk of default. Steve uses the proceeds from this sale to invest in 3-year zeros, as priced in Problem 2 above. current (t = 0) yield curve. That is, unless stated otherwise, use the information below for calculating any values or yields needed in any of the subsequent Problems in this exam. Today (5/27/22), the prices on zero-coupon US Treasury STRIPS are as follows: Maturity Price Effective Annual YTM In years (per $100 in face value) 1 98.50 015228. 2 95.20 .0249. 3 91.75 0291170 4 87.14 1035013. 0400070 5 82.19 If Steve buys as many 3-year zeros as he can with the proceeds from the sale of the 2%- coupon, 2-year bonds, how many 3-year zeros (per $100 in face value) will Steve Inc. get? These bonds are Steve Inc.'s assets. (3 points) What is the duration of the 3-year zeros? (3 points) Again, use the data on the current yield curve from Problem 2. Steve Inc. has someone (Steve) in it's treasury department who thinks he can exploit some mis- pricings in the bond market. On behalf of Steve Inc., Steve issues one thousand (1000) 2-year two-percent annual pay coupon bonds, each with a face value of $1000; each of the 1000 bonds pays its 2% coupons once a year (at the end of the year). The market perceives that Steve Inc. has no risk of default. Steve uses the proceeds from this sale to invest in 3-year zeros, as priced in Problem 2 above. current (t = 0) yield curve. That is, unless stated otherwise, use the information below for calculating any values or yields needed in any of the subsequent Problems in this exam. Today (5/27/22), the prices on zero-coupon US Treasury STRIPS are as follows: Maturity Price Effective Annual YTM In years (per $100 in face value) 1 98.50 015228. 2 95.20 .0249. 3 91.75 0291170 4 87.14 1035013. 0400070 5 82.19 If Steve buys as many 3-year zeros as he can with the proceeds from the sale of the 2%- coupon, 2-year bonds, how many 3-year zeros (per $100 in face value) will Steve Inc. get? These bonds are Steve Inc.'s assets. (3 points) What is the duration of the 3-year zeros? (3 points)