Answered step by step

Verified Expert Solution

Question

1 Approved Answer

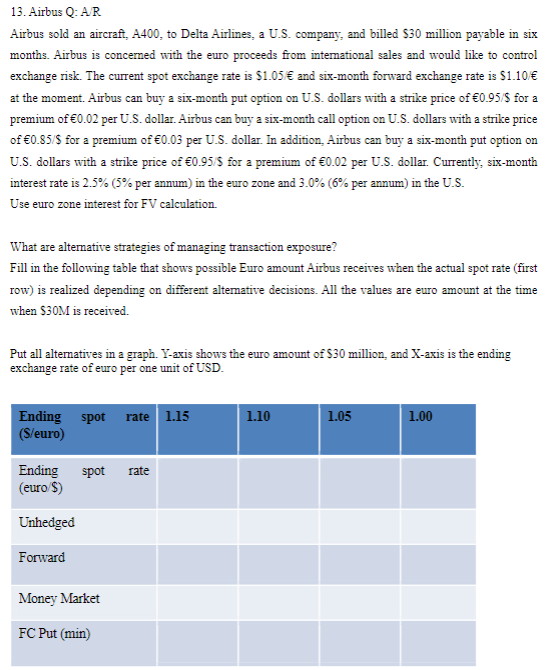

Airbus Q: A / R Airbus sold an aircraft, A 4 0 0 , to Delta Airlines, a U . S . company, and billed

Airbus Q: AR Airbus sold an aircraft, A to Delta Airlines, a US company, and billed $ million payable in six months. Airbus is concerned with the euro proceeds from international sales and would like to control exchange risk. The current spot exchange rate is $ and sixmonth forward exchange rate is $ at the moment. Airbus can buy a sixmonth put option on US dollars with a strike price of for a premium of per US dollar. Airbus can buy a sixmonth call option on US dollars with a strike price of for a premium of per US dollar. In addition, Airbus can buy a sixmonth put option on US dollars with a strike price of for a premium of per US dollar. Currently, sixmonth interest rate is per annum in the euro zone and per annum in the US Use euro zone interest for FV calculation. What are alternative strategies of managing transaction exposure? Fill in the following table that shows possible Euro amount Airbus receives when the actual spot rate first row is realized depending on different alternative decisions. All the values are euro amount at the time when $ is received. Put all alternatives in a graph. axis shows the euro amount of $ million, and axis is the ending exchange rate of euro per one unit of USD.

Airbus Q: AR

Airbus sold an aircraft, A to Delta Airlines, a US company, and billed $ million payable in six

months. Airbus is concerned with the euro proceeds from international sales and would like to control

exchange risk. The current spot exchange rate is $ and sixmonth forward exchange rate is $

at the moment. Airbus can buy a sixmonth put option on US dollars with a strike price of for a

premium of per US dollar. Airbus can buy a sixmonth call option on US dollars with a strike price

of for a premium of per US dollar. In addition, Airbus can buy a sixmonth put option on

US dollars with a strike price of for a premium of per US dollar. Currently, sixmonth

interest rate is per annum in the euro zone and per annum in the US

Use euro zone interest for FV calculation.

What are alternative strategies of managing transaction exposure?

Fill in the following table that shows possible Euro amount Airbus receives when the actual spot rate first

row is realized depending on different alternative decisions. All the values are euro amount at the time

when $ is received.

Put all alternatives in a graph. axis shows the euro amount of $ million, and axis is the ending

exchange rate of euro per one unit of USD.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook On Second Lien Loans & Intercreditor Agreements

Authors: Mark N. Berman, Jo Ann J. Brighton

1st Edition

0981865593, 978-0981865591