Aleida Diaz has been referred to you by a mutual friend as she needs some assistance to sort out her investments outside of her superannuation. During your initial meeting, Aleida provides you with the following information about her current personal situation and financial position. Aleida turned 37 years old in November 2021. Aleida is enjoying her single life and has no family to support financially. She is also not looking for a serious relationship at this point in her life and wants to set things up to ensure she is financial independent. Although COVID has caused some issues with how she works, Aleidas employment is secure and she currently earns a good salary of $124,000 plus employer superannuation guarantee contributions working as a marketing manager. She owns and lives in a townhouse in Shalvey.

She purchased this property in 2013 for $290,000. Aleida believes the property is worth approximately $660,000 today as one of the neighbours sold their unit in January for that price. There is a mortgage on the property of $127,000. Aleida has her personal contents insured with GIO, with cover in place for $62,000. The building is insured through the strata. Before he died in 2021, Aleidas father gifted her his 2002 Holden Calais, which he said, was a great investment. The last time Aleida got the car valued, she was told it was worth somewhere between $15,000 and $17,000. Although she rarely uses the car she keeps it in the garage in memory of her late father. It costs her $2500 a year in insurance fees and $3000 annually for maintenance and registration. Aleidas daily use car is a 2-year-old Toyota Corolla, which is insured comprehensively for $28,000. Aleida is quite worried about debt although she has a credit card with a balance of $28,000 and a limit of $29,000. Aleida is keen to get rid of this debt but does not have a plan on how to pay this off. She knows her annual living expenses (including costs listed above) add to a total of $65,000. She knows she has $4,600 of tax-deductible expenses each year.

She completed her own tax return yearly through MyGov. One of the main reasons that Aleida is seeking advice from you is that her last surviving family member, her sister, recently passed away and as Aleida was the sole beneficiary she will inherit substantial funds from her sisters estate. Aleida expects to be receiving $350,000 after all the estate expenses are accounted for and has been told the funds will be available in June 2022. Aleida is not sure what to do with these funds when she gets them. She has been considering an investment property but is not sure if that is an appropriate investment option as she has read recently that property prices have been falling in Sydney. Aleida keeps about $2,000 in her everyday bank account so there is cash available if needed. Last year Aleida read about a new investment and although not really understanding it decided to have a go and invested. She has received a holding statement which shows she has 2,000 units in the Pengana Private Equity Trust. It says this investment is listed on the ASX with a stock code of PE1. She has not really had time to see how it has performed and is not really sure if it is a share or some other form of investment. As Aleida is earning a good salary and can easily cover living expenses, she is not in need of additional income from investments. While not a top priority, Aleida would like to structure her investments to take advantage of any tax advantages that may be available. You have completed a risk profile with Aleida and the result was that she is effectively a BALANCED investor.

She wants a good return on her investments, but does not want to take a lot of risk. Your licensee has provided risk profile definitions, research and recommended asset allocations for three (3) different risk profiles which can be found below: Conservative Balanced Growth

You are required to produce an Investment Report addressed to the client covering the goals, objectives and issues raised in the case study provided.

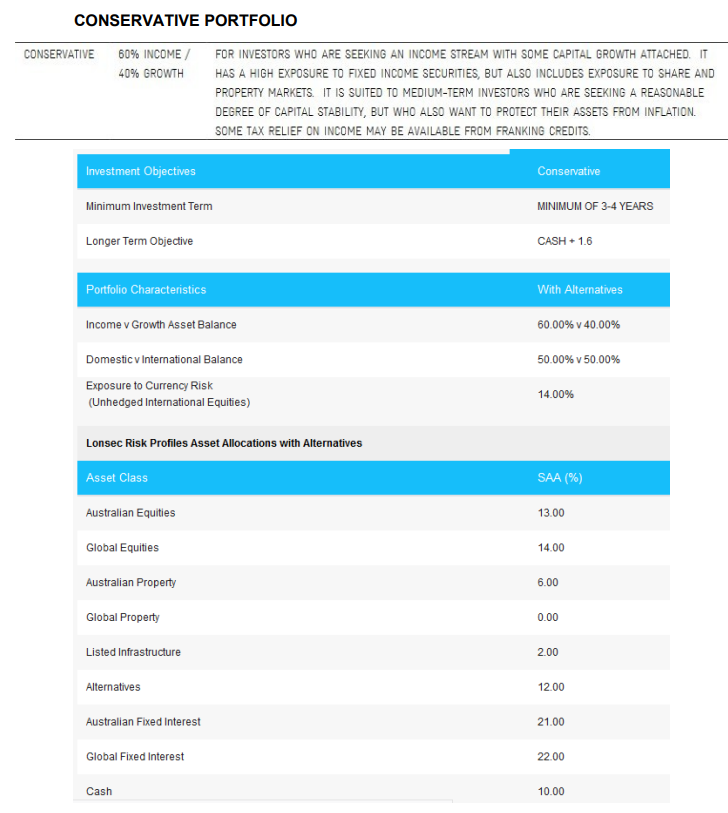

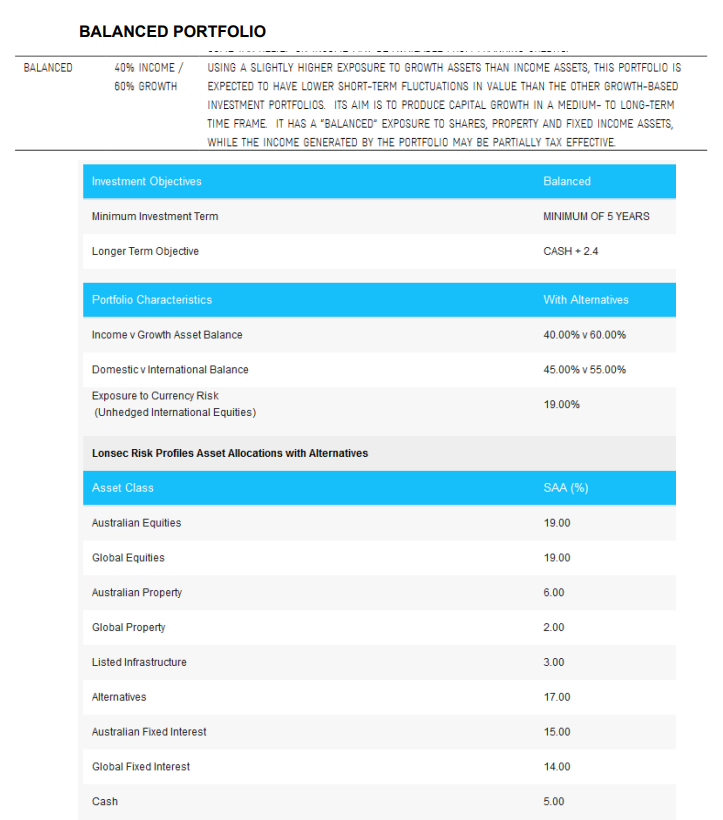

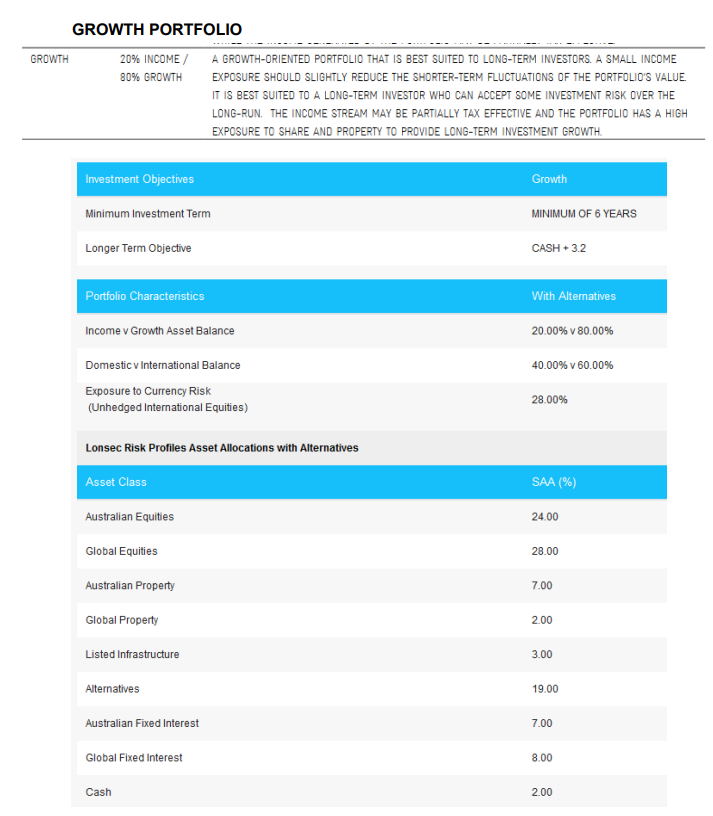

CONSERVATIVE PORTFOLIO CONSERVATIVE 60% INCOME FOR INVESTORS WHO ARE SEEKING AN INCOME STREAM WITH SOME CAPITAL GROWTH ATTACHED. IT 40% GROWTH HAS A HIGH EXPOSURE TO FIXED INCOME SECURITIES, BUT ALSO INCLUDES EXPOSURE TO SHARE AND PROPERTY MARKETS. IT IS SUITED TO MEDIUM-TERM INVESTORS WHO ARE SEEKING A REASONABLE DEGREE OF CAPITAL STABILITY, BUT WHO ALSO WANT TO PROTECT THEIR ASSETS FROM INFLATION. SOME TAX RELIEF ON INCOME MAY BE AVAILABLE FROM FRANKING CREDITS. Investment Objectives Conservative Minimum Investment Term MINIMUM OF 3-4 YEARS Longer Term Objective CASH + 1.6 Portfolio Characteristics With Alternatives Income v Growth Asset Balance 60.00% v 40.00% 50.00% v 50.00% Domestic v International Balance Exposure to Currency Risk (Unhedged International Equities) 14.00% Lonsec Risk Profiles Asset Allocations with Alternatives Asset Class SAA (%) Australian Equities 13.00 Global Equities 14.00 Australian Property 6.00 Global Property 0.00 Listed Infrastructure 2.00 Alternatives 12.00 Australian Fixed Interest 21.00 Global Fixed Interest 22.00 Cash 10.00 BALANCED PORTFOLIO BALANCED 40% INCOME / USING A SLIGHTLY HIGHER EXPOSURE TO GROWTH ASSETS THAN INCOME ASSETS, THIS PORTFOLIO IS 60% GROWTH EXPECTED TO HAVE LOWER SHORT-TERM FLUCTUATIONS IN VALUE THAN THE OTHER GROWTH-BASED INVESTMENT PORTFOLIOS. ITS AIM IS TO PRODUCE CAPITAL GROWTH IN A MEDIUM- TO LONG-TERM TIME FRAME. IT HAS A "BALANCED" EXPOSURE TO SHARES, PROPERTY AND FIXED INCOME ASSETS, WHILE THE INCOME GENERATED BY THE PORTFOLIO MAY BE PARTIALLY TAX EFFECTIVE Investment Objectives Balanced Minimum Investment Term MINIMUM OF 5 YEARS Longer Term Objective CASH +2.4 Portfolio Characteristics With Alternatives Income v Growth Asset Balance 40.00% V 60.00% 45.00% v 55.00% Domestic v International Balance Exposure to Currency Risk (Unhedged International Equities) 19.00% Lonsec Risk Profiles Asset Allocations with Alternatives Asset Class SAA (%) Australian Equities 19.00 Global Equities 19.00 Australian Property 6.00 Global Property 2.00 Listed Infrastructure 3.00 Alternatives 17.00 Australian Fixed Interest 15.00 Global Fixed Interest 14.00 Cash 5.00 GROWTH PORTFOLIO GROWTH 20% INCOME/ A GROWTH-ORIENTED PORTFOLIO THAT IS BEST SUITED TO LONG-TERM INVESTORS. A SMALL INCOME 80% GROWTH EXPOSURE SHOULD SLIGHTLY REDUCE THE SHORTER-TERM FLUCTUATIONS OF THE PORTFOLIO'S VALUE IT IS BEST SUITED TO A LONG-TERM INVESTOR WHO CAN ACCEPT SOME INVESTMENT RISK OVER THE LONG-RUN. THE INCOME STREAM MAY BE PARTIALLY TAX EFFECTIVE AND THE PORTFOLIO HAS A HIGH EXPOSURE TO SHARE AND PROPERTY TO PROVIDE LONG-TERM INVESTMENT GROWTH. Investment Objectives Growth Minimum Investment Term MINIMUM OF 6 YEARS Longer Term Objective CASH + 3.2 Portfolio Characteristics With Alternatives Income v Growth Asset Balance 20.00% v 80.00% 40.00% v 60.00% Domestic v International Balance Exposure to Currency Risk (Unhedged International Equities) 28.00% Lonsec Risk Profiles Asset Allocations with Alternatives Asset Class SAA (%) Australian Equities 24.00 Global Equities 28.00 Australian Property 7.00 Global Property 2.00 Listed Infrastructure 3.00 Alternatives 19.00 Australian Fixed Interest 7.00 Global Fixed Interest 8.00 Cash 2.00 CONSERVATIVE PORTFOLIO CONSERVATIVE 60% INCOME FOR INVESTORS WHO ARE SEEKING AN INCOME STREAM WITH SOME CAPITAL GROWTH ATTACHED. IT 40% GROWTH HAS A HIGH EXPOSURE TO FIXED INCOME SECURITIES, BUT ALSO INCLUDES EXPOSURE TO SHARE AND PROPERTY MARKETS. IT IS SUITED TO MEDIUM-TERM INVESTORS WHO ARE SEEKING A REASONABLE DEGREE OF CAPITAL STABILITY, BUT WHO ALSO WANT TO PROTECT THEIR ASSETS FROM INFLATION. SOME TAX RELIEF ON INCOME MAY BE AVAILABLE FROM FRANKING CREDITS. Investment Objectives Conservative Minimum Investment Term MINIMUM OF 3-4 YEARS Longer Term Objective CASH + 1.6 Portfolio Characteristics With Alternatives Income v Growth Asset Balance 60.00% v 40.00% 50.00% v 50.00% Domestic v International Balance Exposure to Currency Risk (Unhedged International Equities) 14.00% Lonsec Risk Profiles Asset Allocations with Alternatives Asset Class SAA (%) Australian Equities 13.00 Global Equities 14.00 Australian Property 6.00 Global Property 0.00 Listed Infrastructure 2.00 Alternatives 12.00 Australian Fixed Interest 21.00 Global Fixed Interest 22.00 Cash 10.00 BALANCED PORTFOLIO BALANCED 40% INCOME / USING A SLIGHTLY HIGHER EXPOSURE TO GROWTH ASSETS THAN INCOME ASSETS, THIS PORTFOLIO IS 60% GROWTH EXPECTED TO HAVE LOWER SHORT-TERM FLUCTUATIONS IN VALUE THAN THE OTHER GROWTH-BASED INVESTMENT PORTFOLIOS. ITS AIM IS TO PRODUCE CAPITAL GROWTH IN A MEDIUM- TO LONG-TERM TIME FRAME. IT HAS A "BALANCED" EXPOSURE TO SHARES, PROPERTY AND FIXED INCOME ASSETS, WHILE THE INCOME GENERATED BY THE PORTFOLIO MAY BE PARTIALLY TAX EFFECTIVE Investment Objectives Balanced Minimum Investment Term MINIMUM OF 5 YEARS Longer Term Objective CASH +2.4 Portfolio Characteristics With Alternatives Income v Growth Asset Balance 40.00% V 60.00% 45.00% v 55.00% Domestic v International Balance Exposure to Currency Risk (Unhedged International Equities) 19.00% Lonsec Risk Profiles Asset Allocations with Alternatives Asset Class SAA (%) Australian Equities 19.00 Global Equities 19.00 Australian Property 6.00 Global Property 2.00 Listed Infrastructure 3.00 Alternatives 17.00 Australian Fixed Interest 15.00 Global Fixed Interest 14.00 Cash 5.00 GROWTH PORTFOLIO GROWTH 20% INCOME/ A GROWTH-ORIENTED PORTFOLIO THAT IS BEST SUITED TO LONG-TERM INVESTORS. A SMALL INCOME 80% GROWTH EXPOSURE SHOULD SLIGHTLY REDUCE THE SHORTER-TERM FLUCTUATIONS OF THE PORTFOLIO'S VALUE IT IS BEST SUITED TO A LONG-TERM INVESTOR WHO CAN ACCEPT SOME INVESTMENT RISK OVER THE LONG-RUN. THE INCOME STREAM MAY BE PARTIALLY TAX EFFECTIVE AND THE PORTFOLIO HAS A HIGH EXPOSURE TO SHARE AND PROPERTY TO PROVIDE LONG-TERM INVESTMENT GROWTH. Investment Objectives Growth Minimum Investment Term MINIMUM OF 6 YEARS Longer Term Objective CASH + 3.2 Portfolio Characteristics With Alternatives Income v Growth Asset Balance 20.00% v 80.00% 40.00% v 60.00% Domestic v International Balance Exposure to Currency Risk (Unhedged International Equities) 28.00% Lonsec Risk Profiles Asset Allocations with Alternatives Asset Class SAA (%) Australian Equities 24.00 Global Equities 28.00 Australian Property 7.00 Global Property 2.00 Listed Infrastructure 3.00 Alternatives 19.00 Australian Fixed Interest 7.00 Global Fixed Interest 8.00 Cash 2.00