Answered step by step

Verified Expert Solution

Question

1 Approved Answer

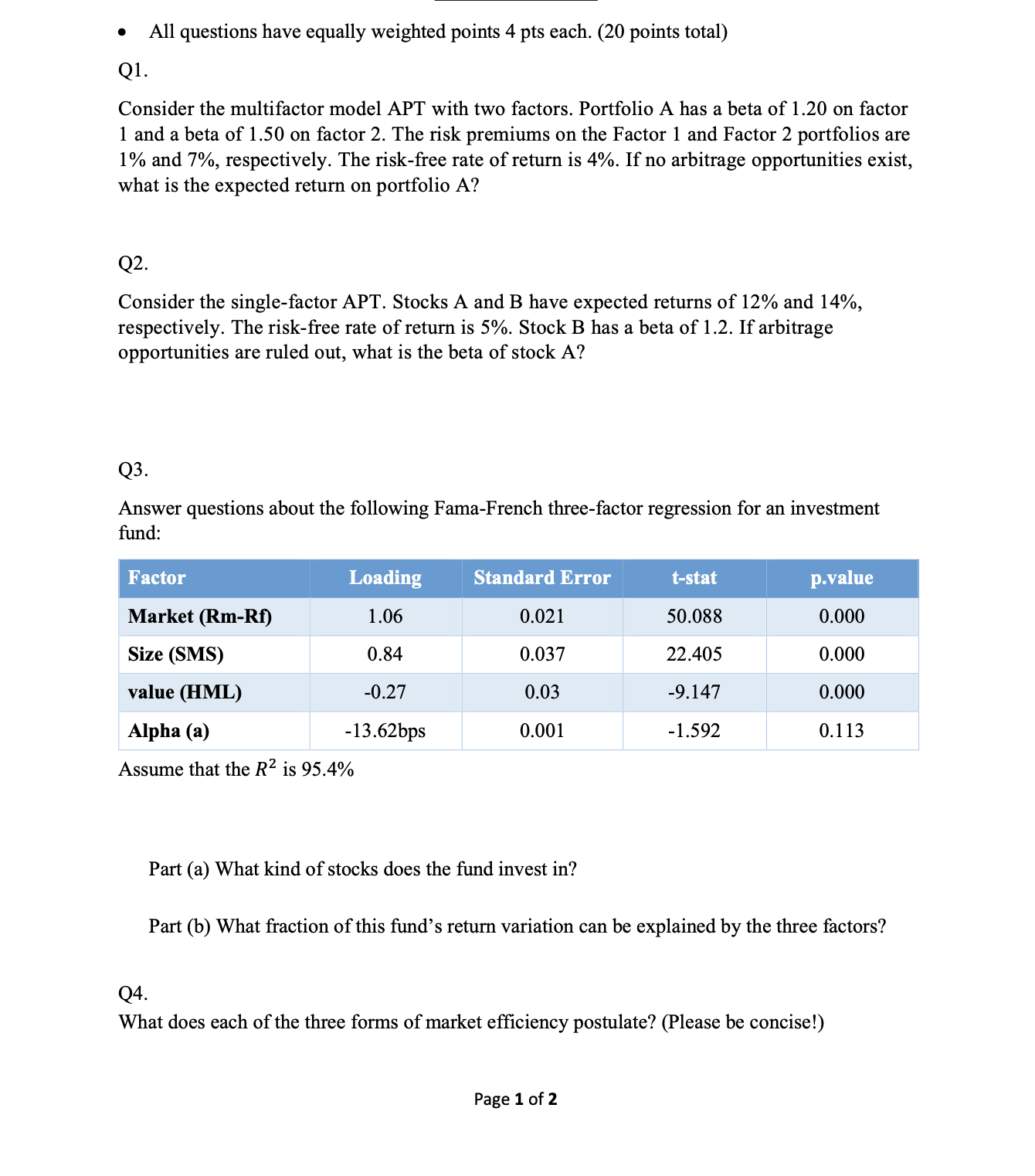

All questions have equally weighted points 4 pts each. (20 points total) Q1. Consider the multifactor model APT with two factors. Portfolio A has

All questions have equally weighted points 4 pts each. (20 points total) Q1. Consider the multifactor model APT with two factors. Portfolio A has a beta of 1.20 on factor 1 and a beta of 1.50 on factor 2. The risk premiums on the Factor 1 and Factor 2 portfolios are 1% and 7%, respectively. The risk-free rate of return is 4%. If no arbitrage opportunities exist, what is the expected return on portfolio A? Q2. Consider the single-factor APT. Stocks A and B have expected returns of 12% and 14%, respectively. The risk-free rate of return is 5%. Stock B has a beta of 1.2. If arbitrage opportunities are ruled out, what is the beta of stock A? Q3. Answer questions about the following Fama-French three-factor regression for an investment fund: Factor Loading Standard Error t-stat p.value Market (Rm-Rf) 1.06 0.021 50.088 0.000 Size (SMS) 0.84 0.037 22.405 0.000 value (HML) -0.27 0.03 -9.147 0.000 Alpha (a) -13.62bps 0.001 -1.592 0.113 Assume that the R is 95.4% Q4. Part (a) What kind of stocks does the fund invest in? Part (b) What fraction of this fund's return variation can be explained by the three factors? What does each of the three forms of market efficiency postulate? (Please be concise!) Page 1 of 2 Q5. List all forms of market efficiency that the momentum anomaly violates. Page 2 of 2

Step by Step Solution

★★★★★

3.42 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

Q1 Expected return on portfolio A in the multifactor APT To calculate the expected return on portfolio A in the multifactor APT we use the formula Exp...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Corporate Finance

Authors: Richard A. Brealey, Stewart C. Myers

7th edition

72869461, 72467665, 9780072467666, 978-0072869460