Answered step by step

Verified Expert Solution

Question

1 Approved Answer

all the questions are listed from A through D = Chegg Books Study Writing Flashcards Math Solver Internships + Et mortive fund before foes =

all the questions are listed from A through D

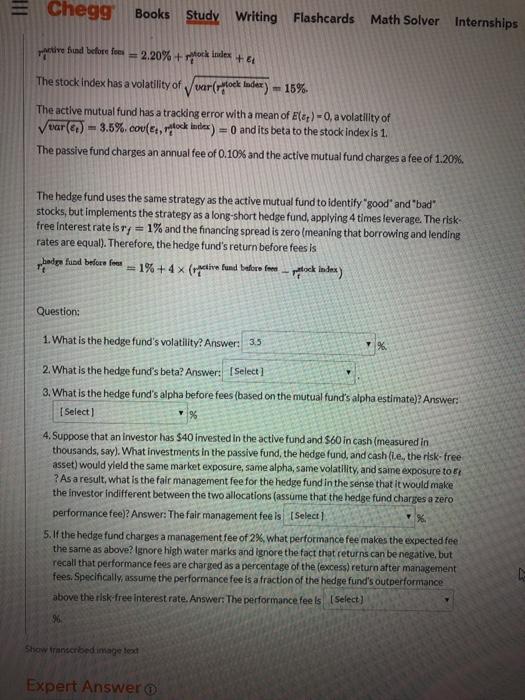

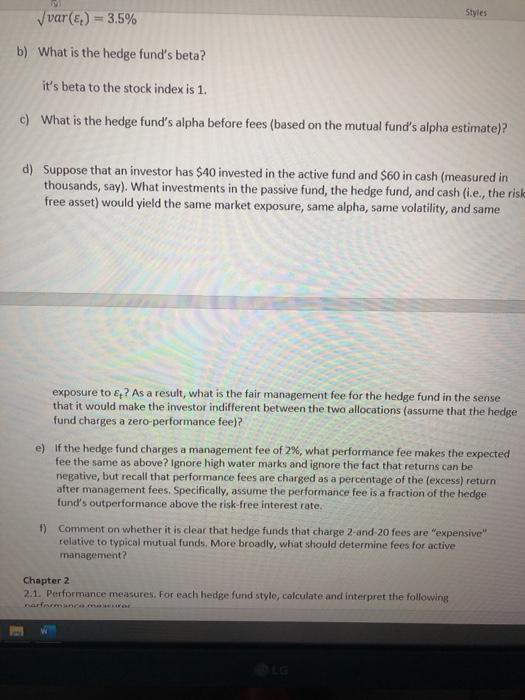

= Chegg Books Study Writing Flashcards Math Solver Internships + Et mortive fund before foes = 2.20% + minork index The stock index has a volatility of var(lock Inder) -15% The active mutual fund has a tracking error with a mean of Elep)-0, a volatility of var() = 3.5%. couler, dock index) = 0 and its beta to the stock Index is 1. The passive fund charges an annual fee of 0.10% and the active mutual fund charges a fee of 1.20%. The hedge fund uses the same strategy as the active mutual fund to identify "good" and "bad" stocks, but implements the strategy as a long-short hedge fund, applying 4 times leverage. The risk free interest rateisty=1% and the financing spread is zero meaning that borrowing and lending rates are equal). Therefore, the hedge fund's return before fees is palga fund befur foes = 1%+4 x (riptive fund telefon - pada da) Question: 1. What is the hedge fund's volatility? Answer: 3.5 2. What is the hedge fund's beta? Answer: [Select] 3.What is the hedge fund's alpha before fees (based on the mutual fund's alpha estimate)? Answer: Select) 4. Suppose that an investor has $40 invested in the active fund and $60 in cash (measured in thousands, say). What investments in the passive fund, the hedge fund, and cash (ie, the risk-free asset) would yield the same market exposure, same alpha, same volatility, and saine exposure to ? As a result what is the fair management fee for the hedge fund in the sense that it would make the investor indifferent between the two allocations (assume that the hedge fund charges a zero performance fee)? Answer: The fair management fee is (Select] 5. If the hedge fund charges a management fee of 2% what performance fee makes the expected fee the same as above? ignore high water marks and ignore the fact that returns can be negative, but recall that performance fees are charged as a percentage of the (excess) return after management fees. Specifically, assume the performance fee is a fraction of the hedge fund's outperformance above the risk-free interest rate. Answer: The performance feels Select] 9 Show Transcribed image de Expert Answer var(E-) = 3.5% Styles b) What is the hedge fund's beta? it's beta to the stock index is 1. c) What is the hedge fund's alpha before fees (based on the mutual fund's alpha estimate)? d) Suppose that an investor has $40 invested in the active fund and $60 in cash (measured in thousands, say). What investments in the passive fund, the hedge fund, and cash (i.e., the risk free asset) would yield the same market exposure, same alpha, same volatility, and same exposure to e,? As a result, what is the fair management fee for the hedge fund in the sense that it would make the investor indifferent between the two allocations (assume that the hedge fund charges a zero-performance fee)? e) If the hedge fund charges a management fee of 2%, what performance fee makes the expected fee the same as above? Ignore high water marks and ignore the fact that returns can be negative, but recall that performance fees are charged as a percentage of the (excess) return after management fees. Specifically, assume the performance fee is a fraction of the hedge fund's outperformance above the risk-free interest rate. 1) Comment on whether it is clear that hedge funds that charge 2-and-20 fees are expensive" relative to typical mutual funds. More broadly, what should determine fees for active management? Chapter 2 2.1. Performance measures. For each hedge fund stylo, calculate and interpret the following = Chegg Books Study Writing Flashcards Math Solver Internships + Et mortive fund before foes = 2.20% + minork index The stock index has a volatility of var(lock Inder) -15% The active mutual fund has a tracking error with a mean of Elep)-0, a volatility of var() = 3.5%. couler, dock index) = 0 and its beta to the stock Index is 1. The passive fund charges an annual fee of 0.10% and the active mutual fund charges a fee of 1.20%. The hedge fund uses the same strategy as the active mutual fund to identify "good" and "bad" stocks, but implements the strategy as a long-short hedge fund, applying 4 times leverage. The risk free interest rateisty=1% and the financing spread is zero meaning that borrowing and lending rates are equal). Therefore, the hedge fund's return before fees is palga fund befur foes = 1%+4 x (riptive fund telefon - pada da) Question: 1. What is the hedge fund's volatility? Answer: 3.5 2. What is the hedge fund's beta? Answer: [Select] 3.What is the hedge fund's alpha before fees (based on the mutual fund's alpha estimate)? Answer: Select) 4. Suppose that an investor has $40 invested in the active fund and $60 in cash (measured in thousands, say). What investments in the passive fund, the hedge fund, and cash (ie, the risk-free asset) would yield the same market exposure, same alpha, same volatility, and saine exposure to ? As a result what is the fair management fee for the hedge fund in the sense that it would make the investor indifferent between the two allocations (assume that the hedge fund charges a zero performance fee)? Answer: The fair management fee is (Select] 5. If the hedge fund charges a management fee of 2% what performance fee makes the expected fee the same as above? ignore high water marks and ignore the fact that returns can be negative, but recall that performance fees are charged as a percentage of the (excess) return after management fees. Specifically, assume the performance fee is a fraction of the hedge fund's outperformance above the risk-free interest rate. Answer: The performance feels Select] 9 Show Transcribed image de Expert Answer var(E-) = 3.5% Styles b) What is the hedge fund's beta? it's beta to the stock index is 1. c) What is the hedge fund's alpha before fees (based on the mutual fund's alpha estimate)? d) Suppose that an investor has $40 invested in the active fund and $60 in cash (measured in thousands, say). What investments in the passive fund, the hedge fund, and cash (i.e., the risk free asset) would yield the same market exposure, same alpha, same volatility, and same exposure to e,? As a result, what is the fair management fee for the hedge fund in the sense that it would make the investor indifferent between the two allocations (assume that the hedge fund charges a zero-performance fee)? e) If the hedge fund charges a management fee of 2%, what performance fee makes the expected fee the same as above? Ignore high water marks and ignore the fact that returns can be negative, but recall that performance fees are charged as a percentage of the (excess) return after management fees. Specifically, assume the performance fee is a fraction of the hedge fund's outperformance above the risk-free interest rate. 1) Comment on whether it is clear that hedge funds that charge 2-and-20 fees are expensive" relative to typical mutual funds. More broadly, what should determine fees for active management? Chapter 2 2.1. Performance measures. For each hedge fund stylo, calculate and interpret the followingStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management for Public Health and Not for Profit Organizations

Authors: Steven A. Finkler, Thad Calabrese

4th edition

133060411, 132805669, 9780133060416, 978-0132805667