Answered step by step

Verified Expert Solution

Question

1 Approved Answer

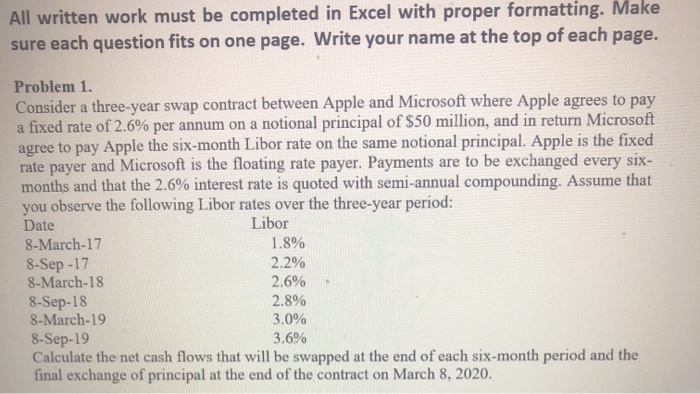

All written work must be completed in Excel with proper formatting. Make sure each question fits on one page. Write your name at the top

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Raising Venture Capital

Authors: Rupert Pearce, Simon Barnes

1st Edition

0470027576, 978-0470027578