Answered step by step

Verified Expert Solution

Question

1 Approved Answer

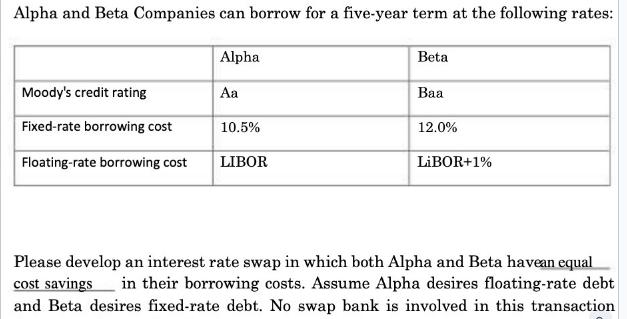

Alpha and Beta Companies can borrow for a five-year term at the following rates: Alpha Beta Moody's credit rating Aa Baa Fixed-rate borrowing cost

Alpha and Beta Companies can borrow for a five-year term at the following rates: Alpha Beta Moody's credit rating Aa Baa Fixed-rate borrowing cost 10.5% 12.0% Floating-rate borrowing cost LIBOR LIBOR+1% Please develop an interest rate swap in which both Alpha and Beta havean equal cost savings in their borrowing costs. Assume Alpha desires floating-rate debt and Beta desires fixed-rate debt. No swap bank is involved in this transaction

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To create an interest rate swap where both Alpha and Beta have equal cost savings in their borrowing ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657