Answered step by step

Verified Expert Solution

Question

1 Approved Answer

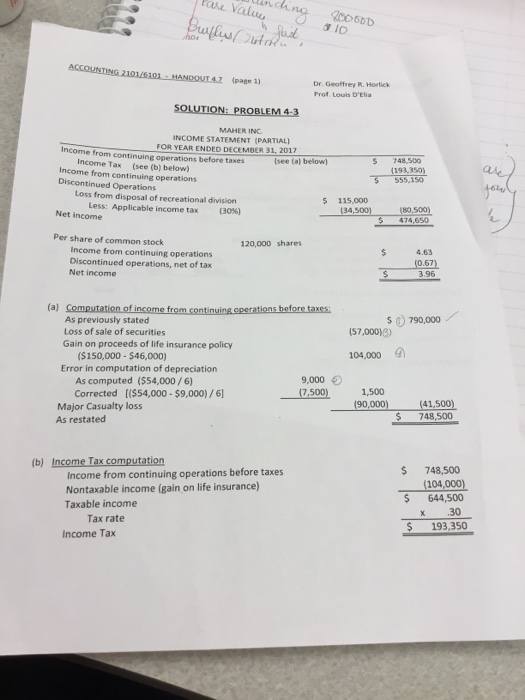

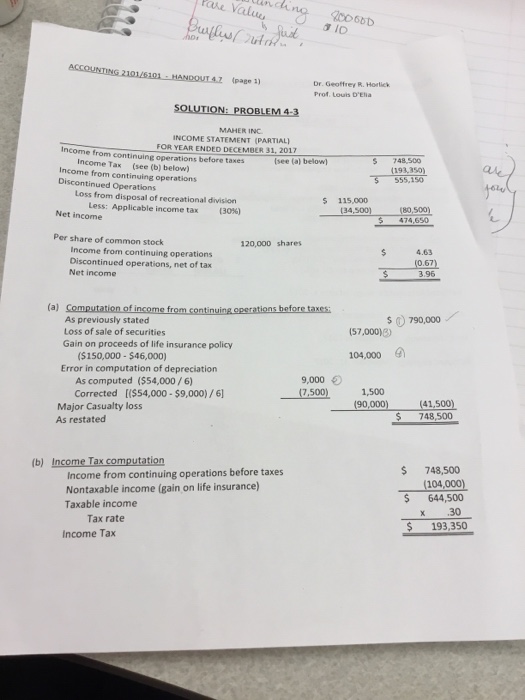

alu 40066D (page 1) Dr. Geoffrey R. Horlick Prof. Louis D'Eia SOLUTION: PROBLEM 4-3 MAHER INC INCOME STATEMENT (PARTIAL) FOR YEAR ENDED DECEMBER 31. 2017

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Decision Making And Control

Authors: Jerold Zimmerman

10th Edition

1259969495, 978-1259969492