Question

Amber, a publicly held corporation, had been paying its chief executive officer (CEO) an annual salary of $900,000. Amber instituted a performance-based compensation plan, effective

Amber, a publicly held corporation, had been paying its chief executive officer (CEO) an annual salary of $900,000. Amber instituted a performance-based compensation plan, effective January 1, 2017, that increased the CEO's 2017 compensation by $300,000. It is anticipated that the plan will provide an additional $350,0000 in 2019.

Prepare a letter to Amber's board of directors explaining how much of the CEO's 2019 compensation is deductible and the consequences of any changes that might be made to the compensation plan in 2019. Address the letter to the board chairperson, Angela Riddle, whose address is 100 James Tower, Cleveland, OH 44106.

Drop Down Options: before; after

is not; was not

includes; excludes

will; will not

only a portion of; all of

make; do not make

not subject; subject

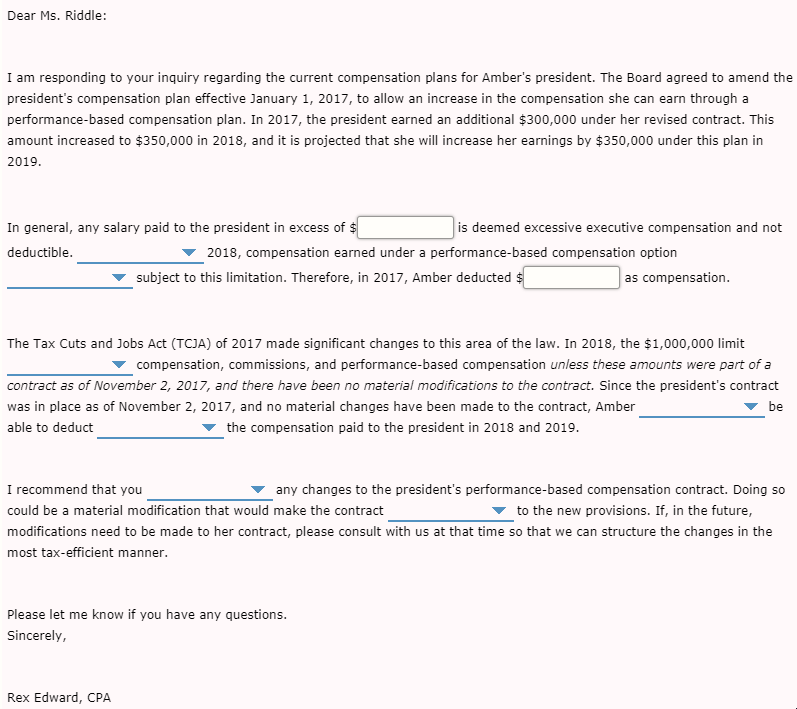

Dear Ms. Riddle: am responding to your inquiry regarding the current compensation plans for Amber's president. The Board agreed to amend the president's compensation plan effective January 1, 2017, to allow an increase in the compensation she can earn through a performance-based compensation plan. In 2017, the president earned an additional $300,000 under her revised contract. This amount increased to $350,000 in 2018, and it is projected that she will increase her earnings by $350,000 under this plan in 2019 In general, any salary paid to the president in excess of $ deductible is deemed excessive executive compensation and not 2018, compensation earned under a performance-based compensation option subject to this limitation. Therefore, in 2017, Amber deducted $ as compensation The Tax Cuts and Jobs Act (TCJA) of 2017 made significant changes to this area of the law. In 2018, the $1,000,000 limit compensation, commissions, and performance-based compensation unless these amounts were part of a contract as of November 2, 2017, and there have been no material modifications to the contract. Since the president's contract was in place as of November 2, 2017, and no material changes have been made to the contract, Amber be able to deduct the compensation paid to the president in 2018 and 2019. I recommend that you any changes to the president's performance-based compensation contract. Doing so could be a material modification that would make the contract to the new provisions. If, in the future, modifications need to be made to her contract, please consult with us at that time so that we can structure the changes in the most tax-efficient manner. Please let me know if you have any questions. Sincerely, Rex Edward, CPA Dear Ms. Riddle: am responding to your inquiry regarding the current compensation plans for Amber's president. The Board agreed to amend the president's compensation plan effective January 1, 2017, to allow an increase in the compensation she can earn through a performance-based compensation plan. In 2017, the president earned an additional $300,000 under her revised contract. This amount increased to $350,000 in 2018, and it is projected that she will increase her earnings by $350,000 under this plan in 2019 In general, any salary paid to the president in excess of $ deductible is deemed excessive executive compensation and not 2018, compensation earned under a performance-based compensation option subject to this limitation. Therefore, in 2017, Amber deducted $ as compensation The Tax Cuts and Jobs Act (TCJA) of 2017 made significant changes to this area of the law. In 2018, the $1,000,000 limit compensation, commissions, and performance-based compensation unless these amounts were part of a contract as of November 2, 2017, and there have been no material modifications to the contract. Since the president's contract was in place as of November 2, 2017, and no material changes have been made to the contract, Amber be able to deduct the compensation paid to the president in 2018 and 2019. I recommend that you any changes to the president's performance-based compensation contract. Doing so could be a material modification that would make the contract to the new provisions. If, in the future, modifications need to be made to her contract, please consult with us at that time so that we can structure the changes in the most tax-efficient manner. Please let me know if you have any questions. Sincerely, Rex Edward, CPA

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advice And Assistance Of The Court Of Audit To Public Authorities Critical Analysis Of Law 5516

Authors: Thami Boudiab

1st Edition

6205921456, 978-6205921456