Question

An individual has $40,000 invested in a stock with a beta of 0.5 and another $40,000 invested in a stock with a beta of 1.9.

An individual has $40,000 invested in a stock with a beta of 0.5 and another $40,000 invested in a stock with a beta of 1.9. If these are the only two investments in her portfolio, what is her portfolio's beta? Do not round intermediate calculations. Round your answer to two decimal places.

Assume that the risk-free rate is 6.5% and the required return on the market is 9%. What is the required rate of return on a stock with a beta of 3? Round your answer to two decimal places.

%

Calculate the required rate of return for Mudd Enterprises assuming that investors expect a 3.2% rate of inflation in the future. The real risk-free rate is 1.0%, and the market risk premium is 6.5%. Mudd has a beta of 1.6, and its realized rate of return has averaged 10.0% over the past 5 years. Round your answer to two decimal places.

%

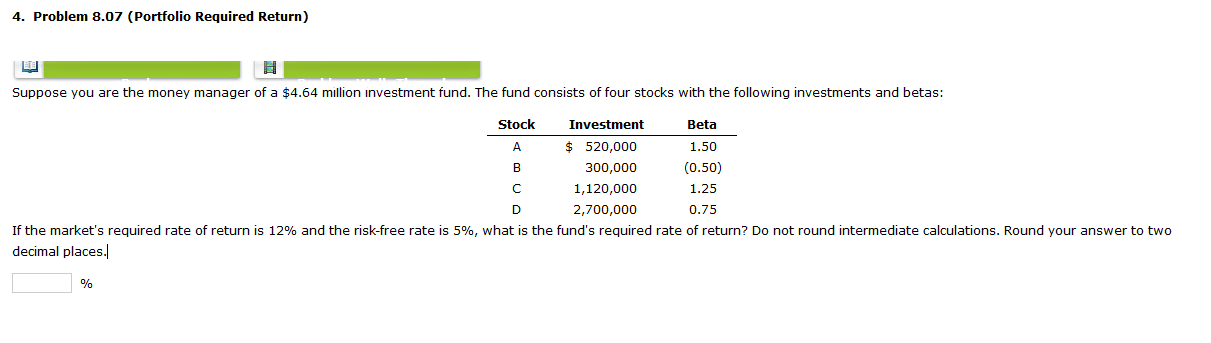

4. Problem 8.07 (Portfolio Required Return) ED Suppose you are the money manager of a $4.64 million investment fund. The fund consists of four stocks with the following investments and betas: Stock Investment Beta $ 520,000 1.50 B 300,000 (0.50) 1,120,000 1.25 2,700,000 If the market's required rate of return is 12% and the risk-free rate is 5%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. 0.75 %Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Growing Enterprises

Authors: Edward W. Davis, Roger Buckland

1st Edition

1138679941, 978-1138679948