Answered step by step

Verified Expert Solution

Question

1 Approved Answer

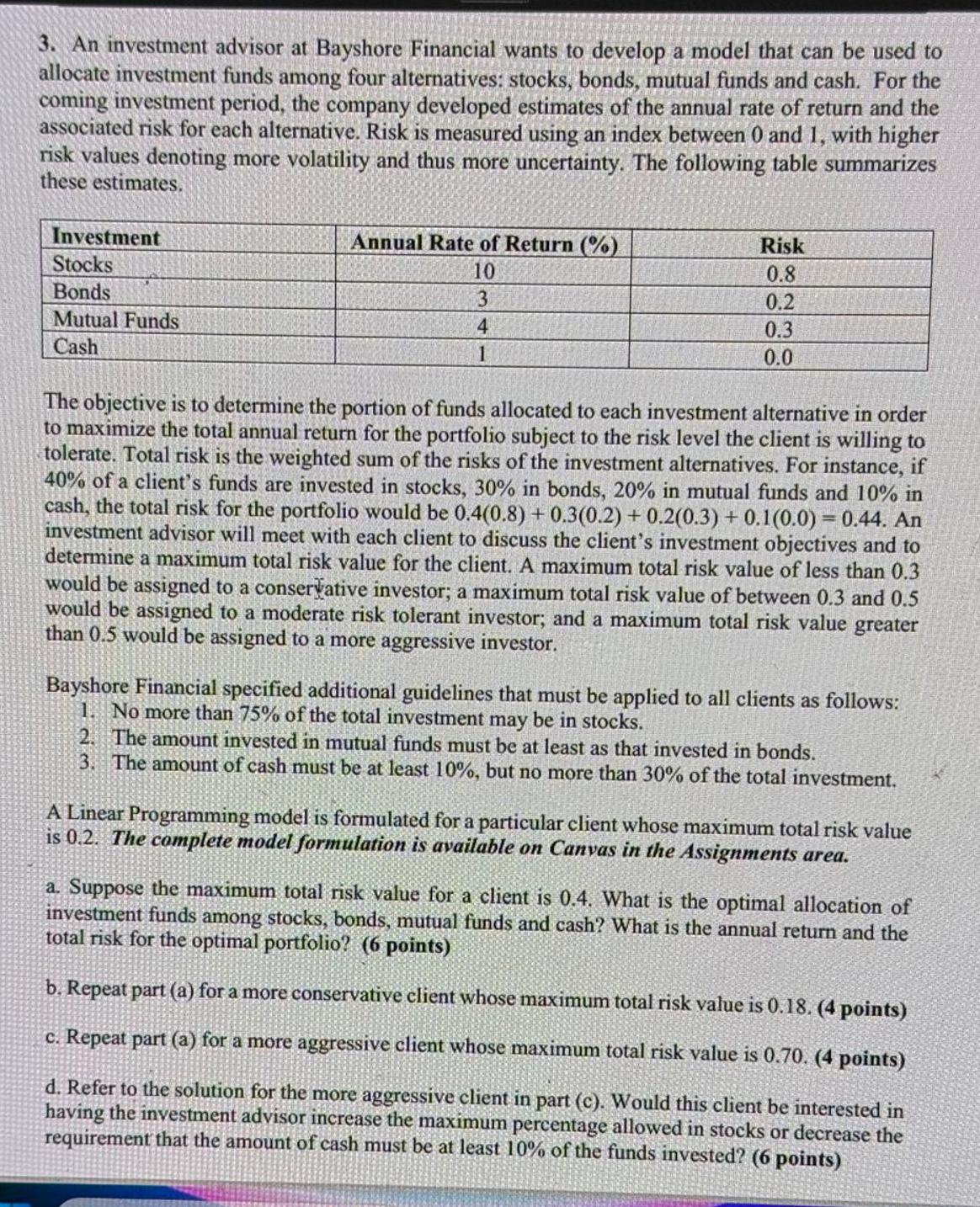

An investment advisor at Bayshore Financial wants to develop a model that can be used to allocate investment funds among four alternatives: stocks, bonds, mutual

An investment advisor at Bayshore Financial wants to develop a model that can be used to

allocate investment funds among four alternatives: stocks, bonds, mutual funds and cash. For the

coming investment period, the company developed estimates of the annual rate of return and the

associated risk for each alternative. Risk is measured using an index between and with higher

risk values denoting more volatility and thus more uncertainty. The following table summarizes

these estimates.

The objective is to determine the portion of funds allocated to each investment alternative in order

to maximize the total annual return for the portfolio subject to the risk level the client is willing to

tolerate. Total risk is the weighted sum of the risks of the investment alternatives. For instance, if

of a client's funds are invested in stocks, in bonds, in mutual funds and in

cash, the total risk for the portfolio would be An

investment advisor will meet with each client to discuss the client's investment objectives and to

determine a maximum total risk value for the client. A maximum total risk value of less than

would be assigned to a conser ative investor; a maximum total risk value of between and

would be assigned to a moderate risk tolerant investor; and a maximum total risk value greater

than would be assigned to a more aggressive investor.

Bayshore Financial specified additional guidelines that must be applied to all clients as follows:

No more than of the total investment may be in stocks.

The amount invested in mutual funds must be at least as that invested in bonds.

The amount of cash must be at least but no more than of the total investment.

A Linear Programming model is formulated for a particular client whose maximum total risk value

is The complete model formulation is available on Canvas in the Assignments area.

a Suppose the maximum total risk value for a client is What is the optimal allocation of

investment funds among stocks, bonds, mutual funds and cash? What is the annual return and the

total risk for the optimal portfolio? points

b Repeat part a for a more conservative client whose maximum total risk value is points

c Repeat part a for a more aggressive client whose maximum total risk value is points

d Refer to the solution for the more aggressive client in part c Would this client be interested in

having the investment advisor increase the maximum percentage allowed in stocks or decrease the

requirement that the amount of cash must be at least of the funds invested? points

Let

S the proportion of funds invested in stocks

B the proportion of funds invested in bonds

M the proportion of funds invested in mutual funds

C the proportion of funds invested in cash

The LP formulation for a client whose maximum total risk is follows.

Max S B M C

st

S B M C

S B M

S

B M

C

C

S B M C

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stocks And Forex Trading How To Win

Authors: Daryl Guppy ,karen Wong

1st Edition

9811237646, 978-9811237645