Answered step by step

Verified Expert Solution

Question

1 Approved Answer

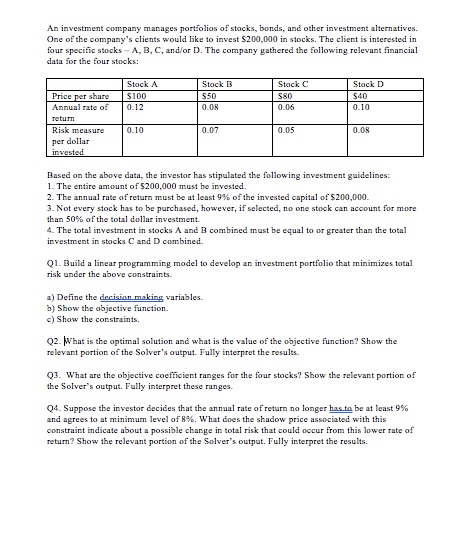

An investment company manages portfolios of stocks, bonds, and other investment alternatives. One of the company's clients would like to invest $200,000 in stocks. The

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Small Business Management Launching & Growing Entrepreneurial Ventures

Authors: Justin Longenecker, William Petty, Leslie Palich, Frank Hoy

17th edition

9781285972565, 1133947751, 1285972562, 978-1133947752