Answered step by step

Verified Expert Solution

Question

1 Approved Answer

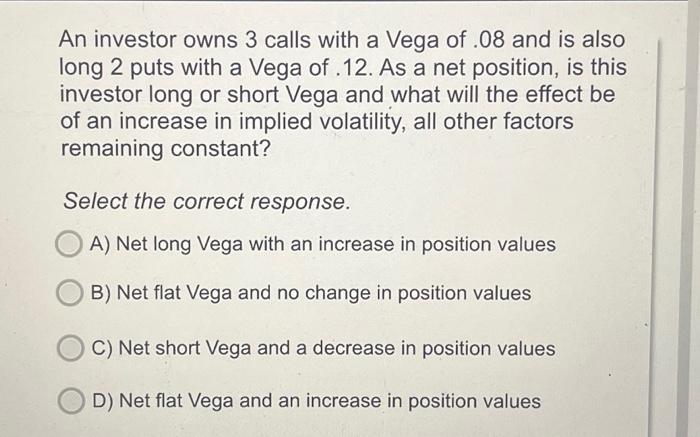

An investor owns 3 calls with a Vega of .08 and is also long 2 puts with a Vega of .12. As a net position,

An investor owns 3 calls with a Vega of .08 and is also long 2 puts with a Vega of .12. As a net position, is this investor long or short Vega and what will the effect be of an increase in implied volatility, all other factors remaining constant? Select the correct response. A) Net long Vega with an increase in position values B) Net flat Vega and no change in position values C) Net short Vega and a decrease in position values D) Net flat Vega and an increase in position values

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing Finance

Authors: CMI Books

1st Edition

1781252181, 978-1781252185