Answered step by step

Verified Expert Solution

Question

1 Approved Answer

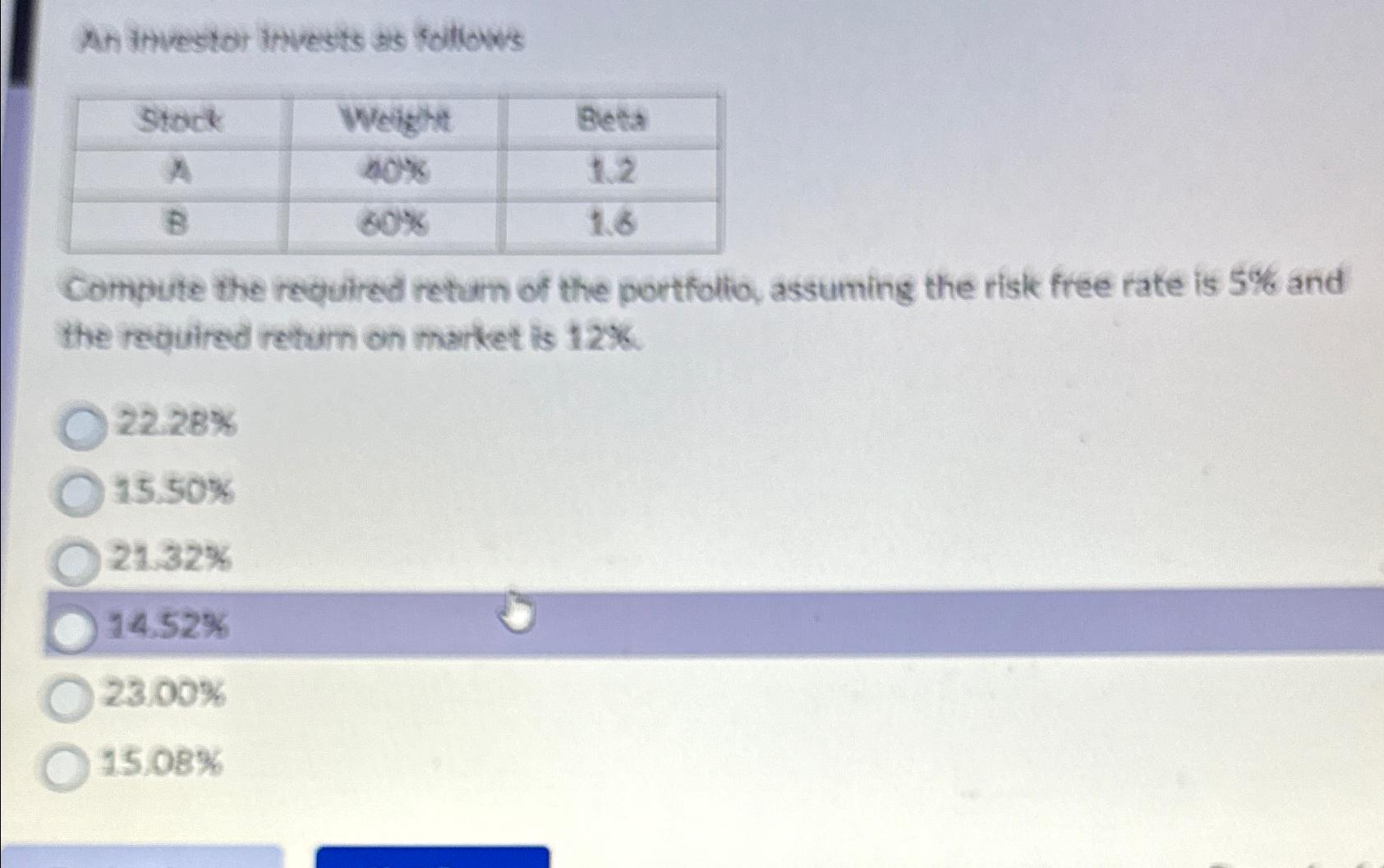

An itriestor invests as follows table[[Stack,Werght,Beta],[A, 40x ,1.2],[B, 60% ,1.6]] Compute the required retam of the portfolio, assuming the risk free rate is 5% and

An itriestor invests as follows\ \\\\table[[Stack,Werght,Beta],[A,

40x,1.2],[B,

60%,1.6]]\ Compute the required retam of the portfolio, assuming the risk free rate is

5%and the reailed retarn on market is

12%.\

22.28%\

15.50%\

21.32%\

14.52%\

2300%\

15.08%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started