Answered step by step

Verified Expert Solution

Question

1 Approved Answer

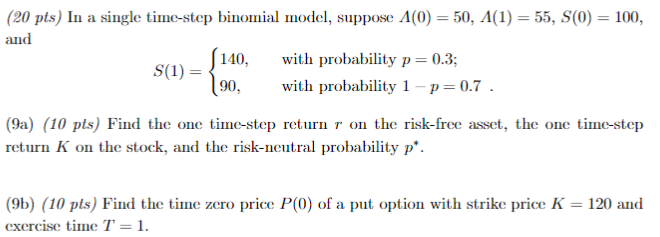

and (20 pts) In a single time-step binomial model, suppose A(0) = 50, A(1) = 55, S(0) = 100, ( 140, with probability p=0.3; S(1)=

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Personal Finance

Authors: Sally R. Campbell, Robert L. Dansby

9th Edition

1619603578, 9781619603578