Answered step by step

Verified Expert Solution

Question

1 Approved Answer

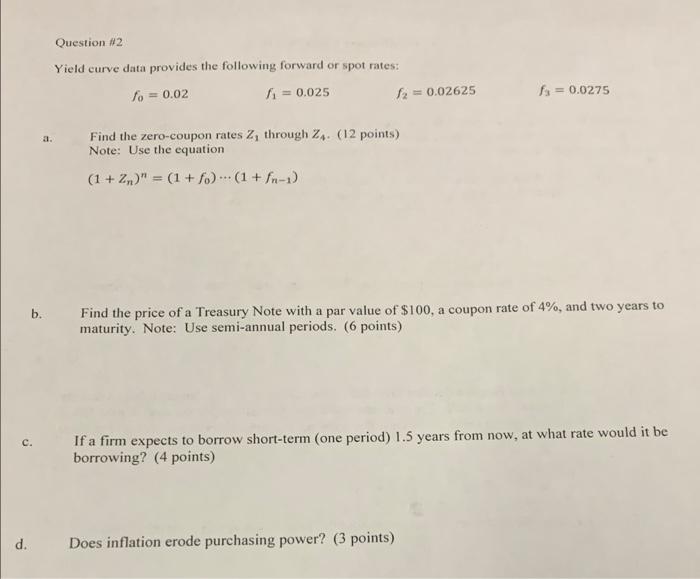

answer all and show full work. Question 2 Yield curve data provides the following forward or spot rates: fo = 0.02 f = 0.025 12

answer all and show full work.

Question 2 Yield curve data provides the following forward or spot rates: fo = 0.02 f = 0.025 12 0.02625 f = 0.0275 a. Find the zero-coupon rates 2, through Z. (12 points) Note: Use the equation (1 + 2n" = (1 + f2) (1 + fn-1) b. Find the price of a Treasury Note with a par value of $100, a coupon rate of 4%, and two years to maturity. Note: Use semi-annual periods. (6 points) c. If a firm expects to borrow short-term (one period) 1.5 years from now, at what rate would it be borrowing? (4 points) d. Does inflation erode purchasing power? (3 points) Question 2 Yield curve data provides the following forward or spot rates: fo = 0.02 f = 0.025 12 0.02625 f = 0.0275 a. Find the zero-coupon rates 2, through Z. (12 points) Note: Use the equation (1 + 2n" = (1 + f2) (1 + fn-1) b. Find the price of a Treasury Note with a par value of $100, a coupon rate of 4%, and two years to maturity. Note: Use semi-annual periods. (6 points) c. If a firm expects to borrow short-term (one period) 1.5 years from now, at what rate would it be borrowing? (4 points) d. Does inflation erode purchasing power? (3 points) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading Option Trading Strategies For Beginners

Authors: Alan Richards

1st Edition

153274479X, 978-1532744792