Answered step by step

Verified Expert Solution

Question

1 Approved Answer

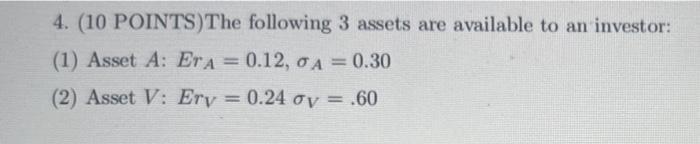

answer each part part step by step clearly 4. (10 POINTS)The following 3 assets are available to an investor: (1) Asset A: ErA=0.12,A=0.30 (2) Asset

answer each part part step by step clearly

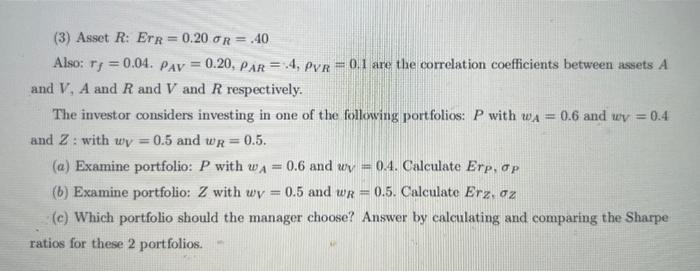

4. (10 POINTS)The following 3 assets are available to an investor: (1) Asset A: ErA=0.12,A=0.30 (2) Asset V:ErV=0.24V=.60 (3) Asset R:ErR=0.20R=.40 Also: rf=0.04. AV=0.20,AR=.4,VR=0.1 are the correlation coefficients between assets A and V,A and R and V and R respectively. The investor considers investing in one of the following port folios: P with wA=0.6 and wV=0.4 and Z : with wV=0.5 and wR=0.5. (a) Examine portfolio: P with wA=0.6 and wV=0.4. Calculate ErP,P (b) Examine portfolio: Z with wV=0.5 and wR=0.5. Calculate ErZ,Z (c) Which portfolio should the manager choose? Answer by calculating and comparing the Sharpe ratios for these 2 portfolios Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Harvey Rosen

6th International Edition

0071121234, 978-0071121231