Question

Answer for the question is given below: 1. Net fair value of identifiable assets and liabilities of Thomas Ltd = ($130,000 + $50,000 + $40,500)

Answer for the question is given below:

1.

Net fair value of identifiable assets and liabilities of Thomas Ltd = ($130,000 + $50,000 + $40,500) (equity)

+ $8,000 (1 30%) (inventory)

+ $10,000 (1 30%) (plant)

+ $20,000 (1 30%) (land)

+ $12,000 (1 30%) (internally generated brand)

- $15,000 (1 30%) (provision for damages)

- $5,000 (goodwill)

= $220,500 + $5,600 + $7,000 + $14,000 + $8,400 - $10,500 - $5000

= $240,000

Consideration transferred = $246,000

Goodwill = $246,000 - $240,000

= $6,000

Goodwill recorded = $5,000

Unrecorded goodwill = $1,000

Explanation:

Goodwill is the difference between the price paid for acquiring the business and the net fair value of indentifiable assets and liabilities of the company being acquired.

| Date | Account | Dr | Cr |

| 2022-06-30 | Accumulated Depreciation | $30,000 | |

| Property, Plant and Equipment | $20,000 | ||

| Deferred Tax Liability | $3,000 | ||

| BCVR | $7,000 |

| Date | Account | Dr | Cr |

| 2022-06-30 | Depreciation Expense | $4,000 | |

| Accumulated Depreciation | $4,000 | ||

| ($10,000*2/5) |

| Date | Account | Dr | Cr |

| 2022-06-30 | Deferred Tax Liability | $1,200 | |

| Income Tax Expense (Benefit) | $1,200 | ||

| $4000*30% |

| Date | Account | Dr | Cr |

| 2022-06-30 | Land and Land Improvements | $20,000 | |

| Deferred Tax Liability | $6,000 | ||

| BCVR | $14,000 |

| Date | Account | Dr | Cr |

| 2022-06-30 | Inventory | $8,000 | |

| Deferred Tax Liability | $2,400 | ||

| BCVR | $5,600 |

| Date | Account | Dr | Cr |

| 2022-06-30 | Accumulated Impairment Loss | $13,000 | |

| Goodwill | $12,000 | ||

| BCVR | $1,000 |

| Date | Account | Dr | Cr |

| 2022-06-30 | Intangible Assets Excluding Goodwill | $12,000 | |

| Deferred Tax Liability | $3,600 | ||

| BCVR | $8,400 |

| Date | Account | Dr | Cr |

| 2022-06-30 | BCVR | $10,500 | |

| Deferred Tax Asset | $4,500 | ||

| Provisions (contingent liabilities) | $15,000 |

| Date | Account | Dr | Cr |

| 2022-09-30 | Retained Earnings | $40,500 | |

| Common Equity, Stock | $130,000 | ||

| General Reserve | $50,000 | ||

| BCVR | $25,500 | ||

| Shares in Thomas Ltd | $246,000 |

CAN YOU PLEASE GIVE REMAINING ANSWER AFTER THIS SOLUTION , I WILL GIVE YOU TWO UPVOTE FROM TWO ACCOUNT

|

| Jonathan Ltd | Thomas Ltd |

| Adjustments |

| Group | |

| Dr | Cr |

| |||||

| Revenues | 90 000 | 64 000 |

|

|

|

|

|

| Expenses | 34 000 | 42 000 |

|

|

|

|

|

| Trading profit | 56 000 | 22 000 |

|

|

|

|

|

| Gains (losses) on sale of non-current assets | 8 000 | 8 000 |

|

|

|

|

|

| Profit before tax | 64 000 | 30 000 |

|

|

|

|

|

| Income tax expense | 12 000 | 5 000 |

|

|

|

|

|

| Profit | 52 000 | 25 000 |

|

|

|

|

|

| Retained earnings (1/7/21) | 103 000 | 55 000 |

|

|

|

|

|

| Transfer from BCVR | 0 | 0 |

|

|

|

|

|

| Transfer from general reserve | 30 000 | 15 000 |

|

|

|

|

|

|

| 185 000 | 95 000 |

|

|

|

|

|

| Dividend paid | 20 000 | 0 |

|

|

|

|

|

| Retained earnings (30/6/22) | 165 000 | 95 000 |

|

|

|

|

|

| Share capital | 150 000 | 130 000 |

|

|

|

|

|

| General reserve | 10 000 | 20 000 |

|

|

|

|

|

| BCVR | 0 | 0 |

|

|

|

|

|

|

| 325 000 | 245 000 |

|

|

|

|

|

| Other components of equity (1/7/21) | 30 000 | 15 000 |

|

|

|

|

|

| Increases/Decreases | 5 000 | 3 000 |

|

|

|

|

|

| Other components of equity (30/6/22) | 35 000 | 18 000 |

|

|

|

|

|

| Total equity | 360 000 | 263 000 |

|

|

|

|

|

| Accounts payable | 30 000 | 10 000 |

|

|

|

|

|

| Deferred tax liability | 18 000 | 10 000 |

|

|

|

|

|

| Other liabilities | 250 000 | 230 000 |

|

|

|

|

|

|

| 658 000 | 513 000 |

|

|

|

|

|

| Goodwill | 20 000 | 18 000 |

|

|

|

|

|

| Accumulated impairment losses | 0 | (13 000) |

|

|

|

|

|

| Inventory | 40 000 | 30 000 |

|

|

|

|

|

| Cash | 10 000 | 5 000 |

|

|

|

|

|

| Financial assets | 110 000 | 207 000 |

|

|

|

|

|

| Shares in Francis Ltd | 246 000 | 0 |

|

|

|

|

|

| Land | 20 000 | 20 000 |

|

|

|

|

|

| Brands | 80 000 | 0 |

|

|

|

|

|

| Plant | 314 000 | 466 000 |

|

|

|

|

|

| Accum depreciation | (182 000) | (220 000) |

|

|

|

|

|

|

| 658 000 | 513 000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Complete the consolidated worksheet for 30 June 2022 ,

Prepare the consolidated financial statements at 30 June 2022 ,

Write a report to explain the consolidation process as per AASB10 for wholly ownedentities.

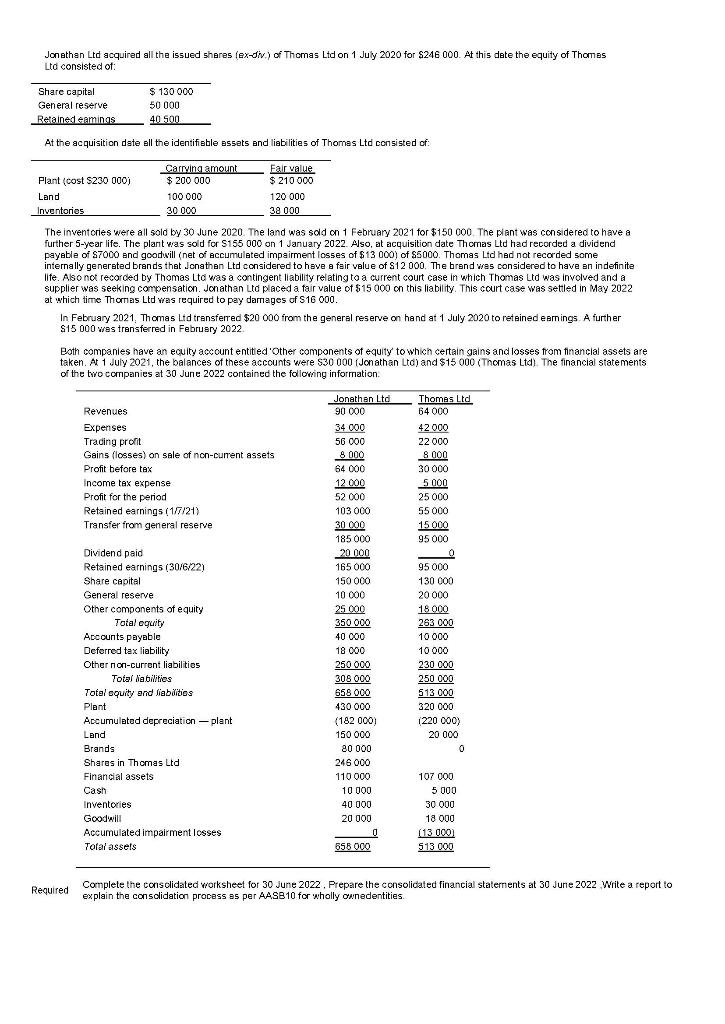

Jonathan Ltd acquired all the issued sheres (ex-div,) of Thomas Ltd on 1 July 2020 for $246000. At this dete the equity of Thomes Lto consisted of: At the acquisition date all the identifibble assets and liabilities of Thomas Ltd consisted of: The inventcries were all sold by 30 June 2020 . The land was sold on 1 February 2021 for $150000. The plant was conside red to have a further 5 -year life. The plant eras sold for $155000 on 1 January 2022. Aso, at acquisition date Thomas Ltd had recorded a dividend payable of $7000 and goodwill (net of accumulated impairment losses of $13000 ) of $5000. Thomas Ltd had not recorded some internally generated brands that Jonathen Ltd considered to have a fair value of S12 000 . The brand was considered to have an indefinite lite. Also not recorded by Thomas Lto was a contingent liability relating to a current court case in which Thomas Ltd was involved and a supplier was seeking compensation. Jonathan Lto placed a tair value of $15000 on this liability. This court case was setted in May 2022 at which time Thomas Ltd was required to pay damages of S16000. In February 2021. Thomas Lid transferred $20000 from the general reserve on hand at 1 July 2020 to retained eam ings. A further $15000 was transferred in February 2022. Eoth companles have an eculty account entited 'Other components of equity' to which certain gains and losses from financial assets are taken. Ak 1 duly 2021, the balances of these accounts were $30000 (Jonathan Lto) and $15000 (Thomas Ltd). The financial statements of the two companies at 30 June 2022 contained the following information. Required Complete the corsclidated worksheet for 30 June 2022 . Prepare the consolidated financial statements at 30 June 2022 Write a report to explain the consolidation process as per AASB10 for wholly ownedentities. Jonathan Ltd acquired all the issued sheres (ex-div,) of Thomas Ltd on 1 July 2020 for $246000. At this dete the equity of Thomes Lto consisted of: At the acquisition date all the identifibble assets and liabilities of Thomas Ltd consisted of: The inventcries were all sold by 30 June 2020 . The land was sold on 1 February 2021 for $150000. The plant was conside red to have a further 5 -year life. The plant eras sold for $155000 on 1 January 2022. Aso, at acquisition date Thomas Ltd had recorded a dividend payable of $7000 and goodwill (net of accumulated impairment losses of $13000 ) of $5000. Thomas Ltd had not recorded some internally generated brands that Jonathen Ltd considered to have a fair value of S12 000 . The brand was considered to have an indefinite lite. Also not recorded by Thomas Lto was a contingent liability relating to a current court case in which Thomas Ltd was involved and a supplier was seeking compensation. Jonathan Lto placed a tair value of $15000 on this liability. This court case was setted in May 2022 at which time Thomas Ltd was required to pay damages of S16000. In February 2021. Thomas Lid transferred $20000 from the general reserve on hand at 1 July 2020 to retained eam ings. A further $15000 was transferred in February 2022. Eoth companles have an eculty account entited 'Other components of equity' to which certain gains and losses from financial assets are taken. Ak 1 duly 2021, the balances of these accounts were $30000 (Jonathan Lto) and $15000 (Thomas Ltd). The financial statements of the two companies at 30 June 2022 contained the following information. Required Complete the corsclidated worksheet for 30 June 2022 . Prepare the consolidated financial statements at 30 June 2022 Write a report to explain the consolidation process as per AASB10 for wholly ownedentitiesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Leadership Style At PT Tekstil Bandung A Management Audit Investigation Following The Prolonged Economic Slowdown In Indonesia

Authors: Samuel P.D. Anantadjaya, Irma M. Nawangwulan

1st Edition

3659328979, 978-3659328978