Answered step by step

Verified Expert Solution

Question

1 Approved Answer

answer is not 170, showing as incorrect QUESTION 22 A 3-quarter interest rate swap (beginning at time 0) has a notional amount of 100,000. What

answer is not 170, showing as incorrect

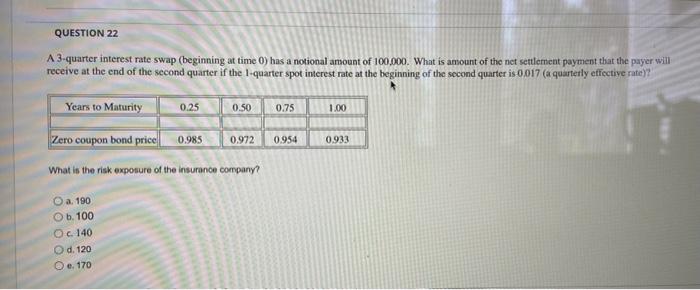

QUESTION 22 A 3-quarter interest rate swap (beginning at time 0) has a notional amount of 100,000. What is amount of the net settlement payment that the payer will receive at the end of the second quarter if the 1-quarter spot interest rate at the beginning of the second quarter is 0.017(a quarterly effective rate)? Years to Maturity 0.25 0.50 0.75 1.00 Zero coupon bond price 0.985 0.972 0.954 0.933 What is the risk exposure of the insurance company O a 190 Ob. 100 O c. 140 d. 120 e. 170 QUESTION 22 A 3-quarter interest rate swap (beginning at time 0) has a notional amount of 100,000. What is amount of the net settlement payment that the payer will receive at the end of the second quarter if the 1-quarter spot interest rate at the beginning of the second quarter is 0.017(a quarterly effective rate)? Years to Maturity 0.25 0.50 0.75 1.00 Zero coupon bond price 0.985 0.972 0.954 0.933 What is the risk exposure of the insurance company O a 190 Ob. 100 O c. 140 d. 120 e. 170 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investing In Bitcoin The Clear Explanation Of What Bitcoin Is

Authors: Russell Strassell

1st Edition

979-8353910404