Answered step by step

Verified Expert Solution

Question

1 Approved Answer

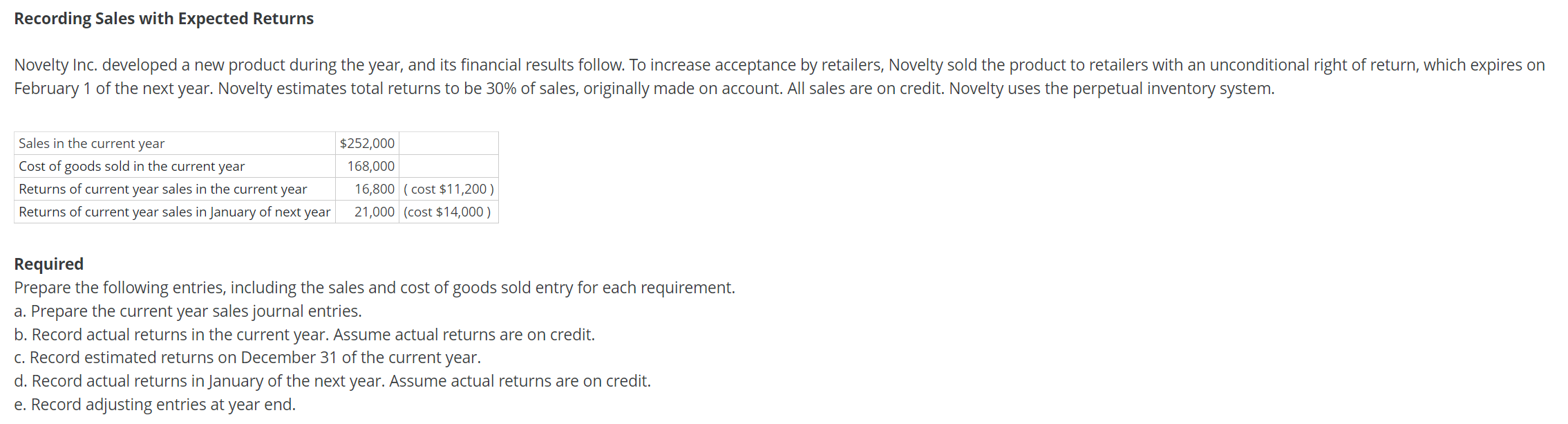

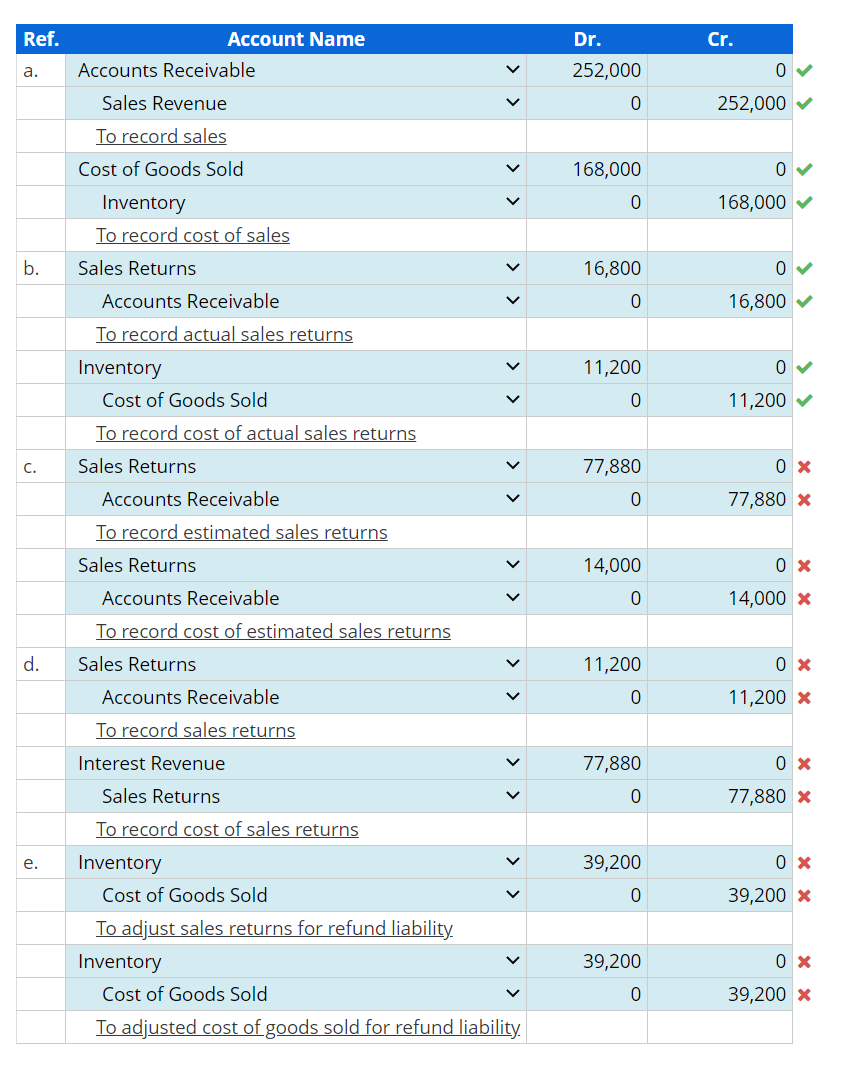

ANSWER PARTS C, D, and E. Make sure your answers are actually correct. Recording Sales with Expected Returns February 1 of the next year. Novelty

ANSWER PARTS C, D, and E.

Make sure your answers are actually correct.

Recording Sales with Expected Returns February 1 of the next year. Novelty estimates total returns to be 30% of sales, originally made on account. All sales are on credit. Novelty uses the perpetual inventory system. Required Prepare the following entries, including the sales and cost of goods sold entry for each requirement. a. Prepare the current year sales journal entries. b. Record actual returns in the current year. Assume actual returns are on credit. c. Record estimated returns on December 31 of the current year. d. Record actual returns in January of the next year. Assume actual returns are on credit. e. Record adjusting entries at year endStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mastering ISO Auditing A Comprehensive Guide To Learn ISO Auditing

Authors: Cybellium Ltd, Kris Hermans

1st Edition

B0CHL9PQFC, 979-8861285858