Question: Answer question 13 only. Thanks. ' 66 Personal Financial Planning: Cases & Applications Textbook 10th Edition 2017-2018 Benjamin and Sarah Redding have great aspirations for

Answer question 13 only. Thanks.

'

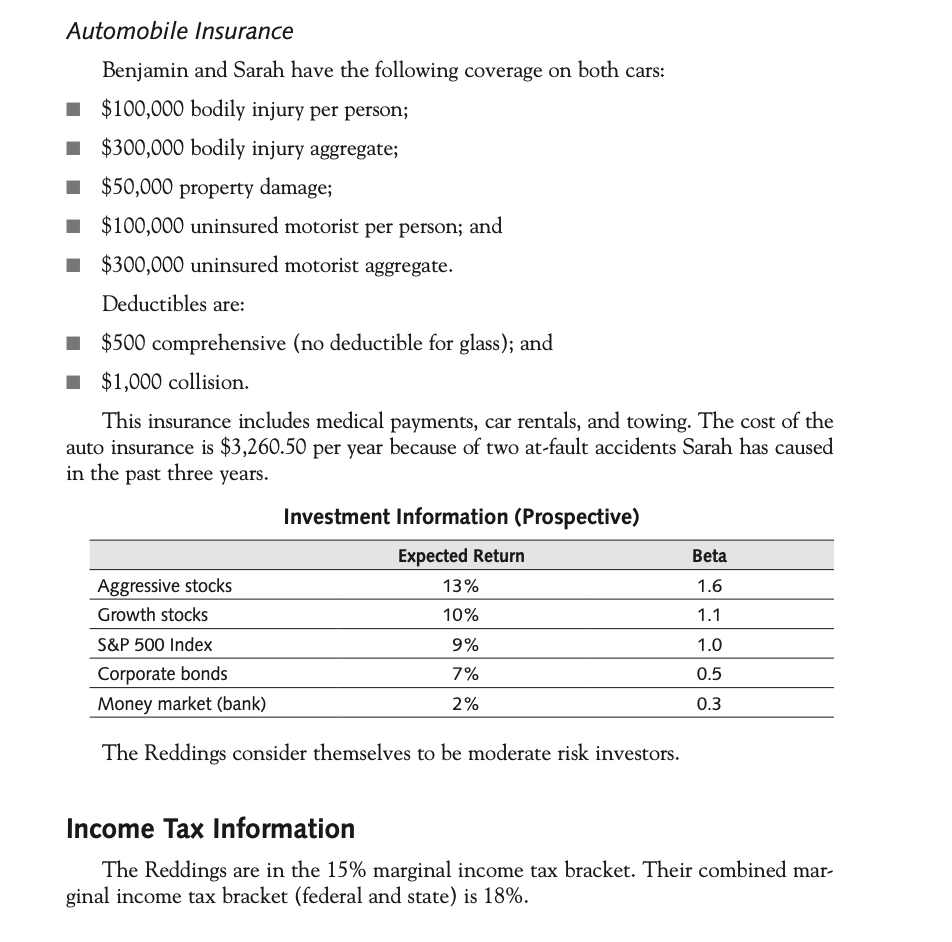

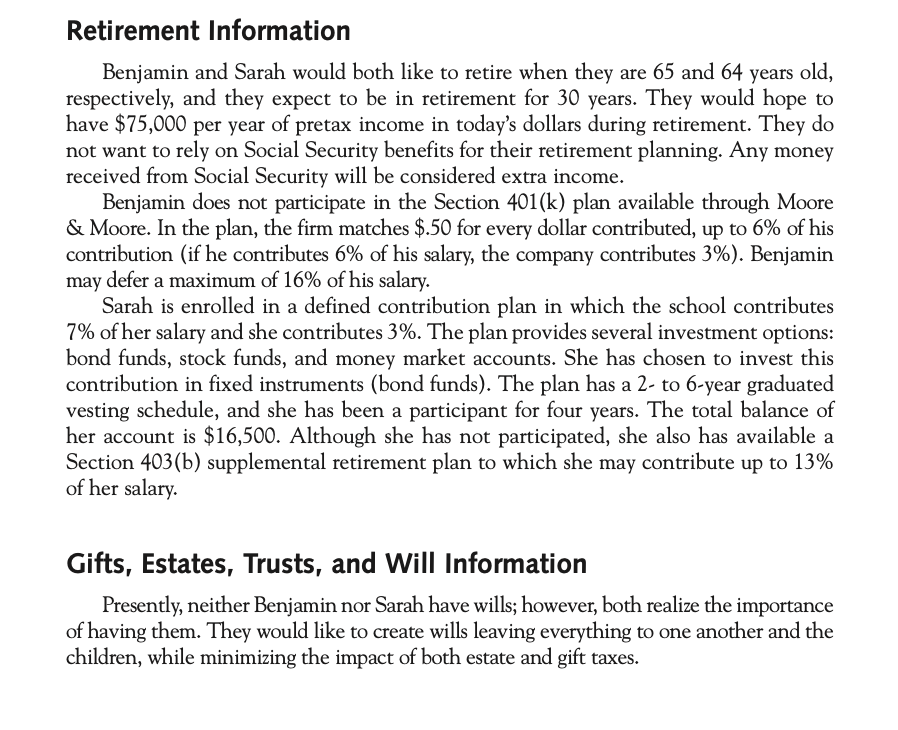

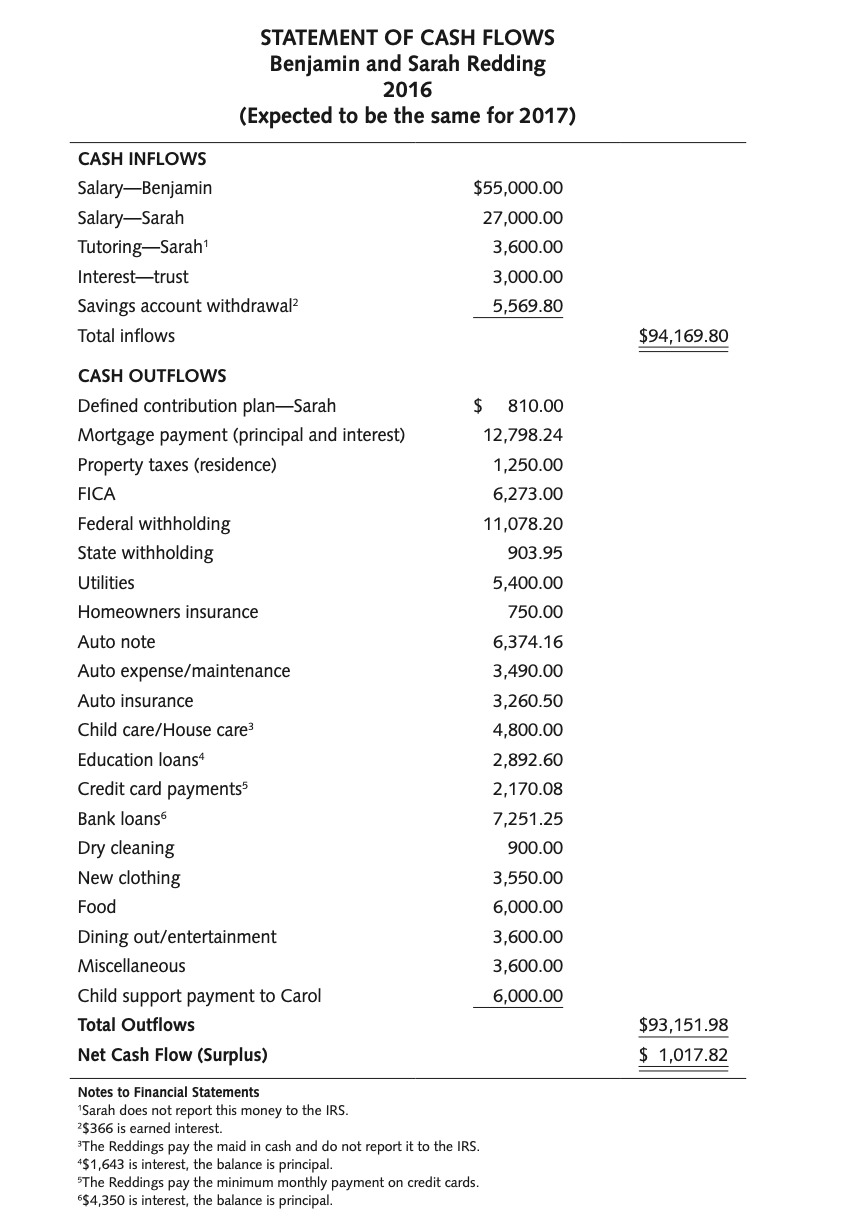

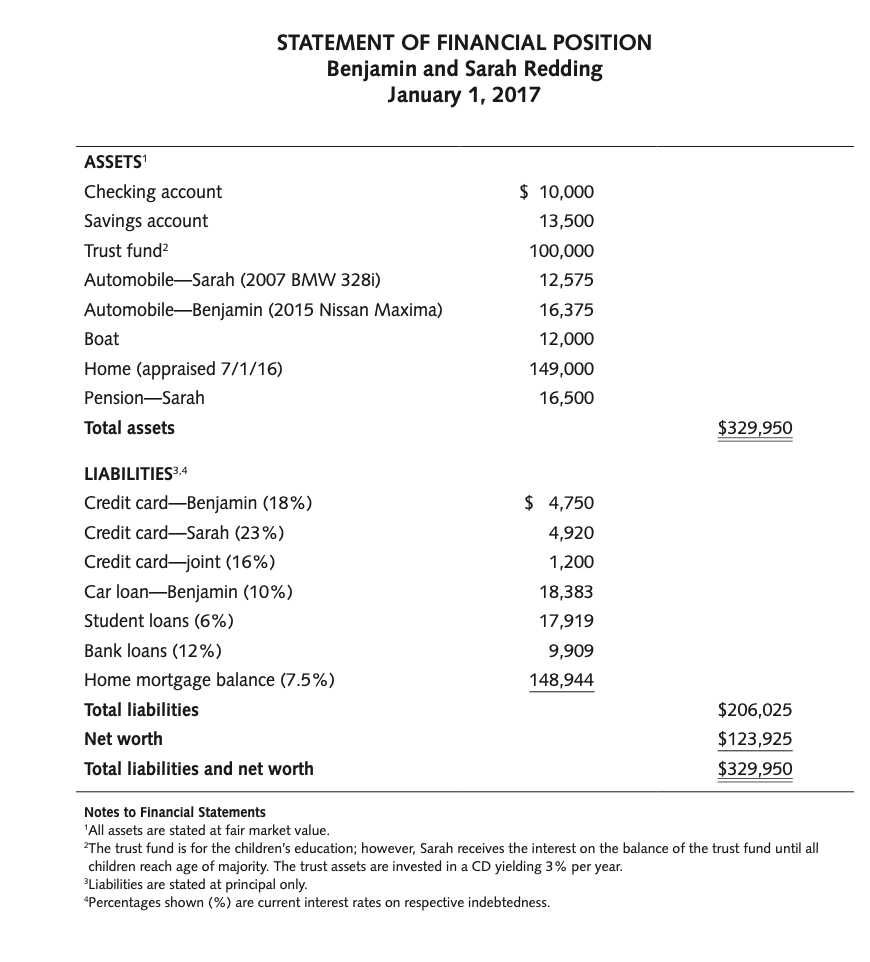

66 Personal Financial Planning: Cases & Applications Textbook 10th Edition 2017-2018 Benjamin and Sarah Redding have great aspirations for their future. They have only recently realized that they are not as financially secure as they had originally thought. They have come to you for advice on how to solve their current cash flow issues and to help them make plans to achieve their goals. Today is January 1, 2017. Personal Background and Information Benjamin Redding (Age 30) Benjamin Redding graduated from a state university seven years ago with a bach- elor of science degree in accounting. He has been employed for almost seven years at Moore & Moore, a small accounting firm (50 employees). Benjamin has been married to Sarah Steiner Redding for six years. Sarah Steiner Redding (Age 29) Sarah Steiner Redding grew up in a wealthy family. She graduated from a private university with a bachelor of science degree in elementary education. She is employed as a fourth grade teacher at a private school, Woodridge Preparatory School, and has been for the past five years. To further enrich her students (and for additional income), Sarah tutors three students each week. She incurs no expenses when providing this tutoring. Children Benjamin and Sarah have three children: Scott, age 4, and twin girls, Janice and Carly, age 1. Delores Vidalia The Reddings employ a young student, Delores Vidalia, to care for their children. Delores, age 21, is a part-time night student at a local community college. She cares for the children and cleans the Reddings' house in exchange for room, board, and a $100 stipend per week. The Reddings pay Delores in cash. Neither the Reddings nor Dolores report these transactions to the IRS. Delores works 48 weeks per year. Benjamin's Family George Redding married Julie Redding in 1985. They had two children, George Jr., and Benjamin. George Jr., died at age six months of sudden infant death syndrome. Benjamin's father, George Sr., died of a heart attack six years ago at age 50. He had ample insurance to cover all medical and funeral expenses. His mother, Julie, a chain-smoker for 37 years, is 53 years old. She was diagnosed with lung cancer three years ago. Because of her rapidly deteriorating health, her doc- tor has predicted that she probably will not live beyond five to seven years. She is receiving monthly chemotherapy treatments at a medical center ($200 out-of-pocket cost per visit). Her doctor has recommended that she be placed in a home with 24-hour care as soon as possible. The cost of this care, including room and board, is about $175 per day, or approximately $5,323 per month. Because of her increased medical expenses and need for constant care, Julie has decided to sell her home. She has contacted Jane Smith, a real estate agent, who has listed her home for $140,000. Julie is adamant that she will accept no less than $135,000. Benjamin and Sarah have been giving Julie $200 per month to help ease her finan- cial burden. They will be forced to incur most of her future expenses. They realize that the sale of the home will provide some assistance; however, the real estate market is soft, and they have had no offers on the house. Julie owns a paid-up whole life insur- ance policy on her own life with a face amount of $500,000 and a cash surrender value (CSV) of $75,000. The policy is not a modified endowment contract (MEC). Benjamin's Great Aunt Mabel plans to give Benjamin and Sarah $10,000 each at the beginning of 2017. Benjamin has always looked out for Mabel, and she wants to show him her gratitude through this gift. Sarah's Family Harry Steiner III married Alice Steiner in 1972. Sarah is an only child and the Steiners' pride and joy. Harry Steiner is a highly respected State Supreme Court justice. He has worked in the city for more than 30 years and is considered an extremely influential figure in the community. Harry and Alice's adjusted gross income (AGI) exceeds $275,000. Alice Steiner was born into a wealthy family. Before they were married, she and Harry decided that she would not work. She is, however, very active in the community through her volunteer work four days a week. The Steiners were happy to welcome Benjamin into their family. In fact, Harry was so excited that he presented Benjamin with a speedboat in hopes that he would get to spend time on the boat getting to know his future son-in-law. As a wedding gift, the Steiners gave Sarah and Benjamin $20,000 toward the purchase of a new home. In addition, the Steiners set up a $100,000 trust fund to assist their grandchildren with college education expenses. Sarah, the beneficiary of the trust fund, receives the monthly interest from the principal until the trust is dissolved, with first Benjamin and then Children's Hospital as successor beneficiaries in the event of Sarah's death. Upon Scott's enrollment in college, he will be given his third of the trust fund, $33,333. Sarah will continue to receive the interest on the remaining $66,666 until Janice and Carly begin college. If a child should die or decide not to go to college by age 22, that child's share would be donated to Children's Hospital. Benjamin was previously married to Carol, an attorney, and together they had one child, Stephen. Benjamin pays Carol $500 each month for child support. Carol's par- ents have agreed to pay 100% of Stephen's college tuition and expenses. Personal and Financial Objectives The Reddings listed the following financial objectives in direct order of importance to their family. 1. Provide private education for all three children at Woodridge Preparatory School for grades K-12. 2. Provide each child with up to $15,000 per year for college education for up to four years in addition to the trust fund. 3. Assist Julie with living and medical expenses until her death. 4. Purchase a home for $300,000 in eight years with a 20% down payment. (By that time, Benjamin should be a partner of the firm.) Housing costs are expected to increase with inflation. They intend to keep their current home as a rental prop- erty. 5. Be free of mortgage indebtedness by the time Benjamin is 55 years old. 6. Prepare a proper retirement plan allowing them a debt-free retirement. They feel that income of $75,000 in today's dollars per year will allow them to maintain their standard of living. 7. Rebuild their savings account/emergency fund to a minimum of $25,000. 8. Save for the twins' future weddings (estimated costs $15,000 each). Economic Information They expect inflation to average 4% annually. They expect Sarah's salary to increase each year by 5%. They expect Benjamin's salary to increase each year by 5%. Mortgage rates are 5.5% for a 15-year fixed and 6.0% for a 30-year fixed. Any refinancing will incur 3% of the mortgage amount as a closing cost. Insurance Information Health Insurance An HMO health insurance plan is provided for the entire family by Moore & Moore. Doctor visits are $10 per visit, while prescriptions are $5 for generic brands and $10 for other brands. There is no co-payment for hospitalization in semiprivate accommodations. Private rooms are provided when medically necessary. For emergency treatment, a $50 co-payment is required. Life Insurance Benjamin has a $110,000 group term life insurance policy through Moore & Moore. Highly compensated employees of Moore & Moore receive group term coverage in the amount of five times their salaries. Sarah has a $27,000 group term life insurance policy through Woodridge Preparatory School. The owners of the policies are Benjamin and Sarah, respectively, with each other as the beneficiary. Disability Insurance Benjamin has disability insurance through Moore & Moore. Short-term disability benefits begin for any absence due to sickness and accident more than six days and will continue for up to six months at 80% of his salary. Long-term disability benefits are available if disability continues more than six months. If Benjamin is unable to per- form the major and substantial duties of his current occupation, the coverage provides him with 60% of his salary while disabled until recovery, death, retirement, or age 65 (whichever occurs first). All disability insurance premiums are fully paid by Moore & Moore. Sarah has no disability insurance. Professional Liability Insurance Moore & Moore has professional liability insurance covering all employees. Homeowners Insurance The Reddings have an HO-3 policy with a $140,000 dwelling coverage limit and liability coverage of $100,000 endorsed to provide loss settlement on a replacement cost basis for personal property. Dwelling coverage is provided on an open peril basis and per- sonal property coverage is provided on a named peril basis. The deductible is $500 with an annual premium of $750. Automobile Insurance Benjamin and Sarah have the following coverage on both cars: $100,000 bodily injury per person; $300,000 bodily injury aggregate; $50,000 property damage; $100,000 uninsured motorist per person; and $300,000 uninsured motorist aggregate. Deductibles are: $500 comprehensive (no deductible for glass); and $1,000 collision. This insurance includes medical payments, car rentals, and towing. The cost of the auto insurance is $3,260.50 per year because of two at-fault accidents Sarah has caused in the past three years. Investment Information (Prospective) Expected Return Beta Aggressive stocks 13% 1.6 Growth stocks 10% 1.1 S&P 500 Index 9% 1.0 Corporate bonds 7% 0.5 Money market (bank) 2% 0.3 The Reddings consider themselves to be moderate risk investors. Income Tax Information The Reddings are in the 15% marginal income tax bracket. Their combined mar- ginal income tax bracket (federal and state) is 18%. Retirement Information Benjamin and Sarah would both like to retire when they are 65 and 64 years old, respectively, and they expect to be in retirement for 30 years. They would hope to have $75,000 per year of pretax income in today's dollars during retirement. They do not want to rely on Social Security benefits for their retirement planning. Any money received from Social Security will be considered extra income. Benjamin does not participate in the Section 401(k) plan available through Moore & Moore. In the plan, the firm matches $.50 for every dollar contributed, up to 6% of his contribution (if he contributes 6% of his salary, the company contributes 3%). Benjamin may defer a maximum of 16% of his salary. Sarah is enrolled in a defined contribution plan in which the school contributes 7% of her salary and she contributes 3%. The plan provides several investment options: bond funds, stock funds, and money market accounts. She has chosen to invest this contribution in fixed instruments (bond funds). The plan has a 2- to 6-year graduated vesting schedule, and she has been a participant for four years. The total balance of her account is $16,500. Although she has not participated, she also has available a Section 403 (b) supplemental retirement plan to which she may contribute up to 13% of her salary. Gifts, Estates, Trusts, and Will Information Presently, neither Benjamin nor Sarah have wills; however, both realize the importance of having them. They would like to create wills leaving everything to one another and the children, while minimizing the impact of both estate and gift taxes. STATEMENT OF CASH FLOWS Benjamin and Sarah Redding 2016 (Expected to be the same for 2017) $55,000.00 27,000.00 3,600.00 3,000.00 5,569.80 $ 810.00 12,798.24 1,250.00 6,273.00 11,078.20 903.95 5,400.00 750.00 6,374.16 3,490.00 3,260.50 4,800.00 2,892.60 2,170.08 7,251.25 900.00 3,550.00 6,000.00 3,600.00 3,600.00 6,000.00 CASH INFLOWS Salary-Benjamin Salary-Sarah Tutoring-Sarah Interest trust Savings account withdrawal Total inflows CASH OUTFLOWS Defined contribution plan-Sarah Mortgage payment (principal and interest) Property taxes (residence) FICA Federal withholding State withholding Utilities Homeowners insurance Auto note Auto expense/maintenance Auto insurance Child care/House care Education loans4 Credit card payments5 Bank loans Dry cleaning New clothing Food Dining out/entertainment Miscellaneous Child support payment to Carol Total Outflows Net Cash Flow (Surplus) Notes to Financial Statements Sarah does not report this money to the IRS. 2$366 is earned interest. The Reddings pay the maid in cash and do not report it to the IRS. 4$1,643 is interest, the balance is principal. "The Reddings pay the minimum monthly payment on credit cards. 6$4,350 is interest, the balance is principal. $94,169.80 $93,151.98 $ 1,017.82 STATEMENT OF FINANCIAL POSITION Benjamin and Sarah Redding January 1, 2017 ASSETS Checking account $ 10,000 Savings account 13,500 Trust fund 100,000 Automobile-Sarah (2007 BMW 328i) 12,575 Automobile-Benjamin (2015 Nissan Maxima) 16,375 Boat 12,000 Home (appraised 7/1/16) 149,000 Pension-Sarah 16,500 Total assets $329,950 LIABILITIES 3,4 Credit card-Benjamin (18%) $4,750 Credit card-Sarah (23%) 4,920 Credit card-joint (16%) 1,200 Car loan-Benjamin (10%) 18,383 Student loans (6%) 17,919 Bank loans (12%) 9,909 Home mortgage balance (7.5%) 148,944 Total liabilities $206,025 $123,925 Net worth Total liabilities and net worth $329,950 Notes to Financial Statements 'All assets are stated at fair market value. The trust fund is for the children's education; however, Sarah receives the interest on the balance of the trust fund until all children reach age of majority. The trust assets are invested in a CD yielding 3% per year. Liabilities are stated at principal only. 4Percentages shown (%) are current interest rates on respective indebtedness. Information Regarding Assets and Liabilities Employment Benjamin is currently employed as a senior accountant at Moore & Moore, earning an annual salary of $55,000. He expects to be promoted to manager within two years. Benjamin hopes to be a partner in eight years. Sarah earns $27,000 annually teaching at Woodridge Preparatory School. Annual salary increases range from 3-5%. She also earns approximately $3,600 each year tutor- ing. This money is received in cash. Although they should, she and Benjamin do not report her tutoring earnings on their tax returns. In addition, Sarah receives $3,000 a year, before taxes, on the interest earned from the children's trust fund. Benjamin and Sarah earn approximately 2% interest on their savings account. This is automatically credited on a quarterly basis to the account; however, they do not consider this small amount of interest to be income. This savings account/emergency fund began with an account balance of $25,000 when they were first married. In 2016, they withdrew $366 in interest income and $5,203.80 from the savings account to pay bills. Home Benjamin and Sarah purchased a four-bedroom house for $170,000 in a nice fam- ily neighborhood. They were among the first families to purchase a home in this new subdivision. The money received from Sarah's parents as a wedding gift was used for the down payment. The mortgage payment is $1,066.52 per month. The interest rate is 7.5%. The original mortgage was $152,531.47, and they have made 29 payments. Utilities range from $400-500 per month. Although the original value of the house was $170,000, a recent appraisal valued the house at $149,000. The decrease in value did not leave enough equity for the Reddings to be approved for a home equity loan. If the Reddings wanted to refinance (80% of the fair market value of the home), the 3% closing costs would have to be paid at closing and not financed. Automobiles In 2015, Benjamin purchased a new Nissan Maxima for $25,000. The current value of the car is $16,375, but the loan balance is $18,383.47. The term of the loan is 60 months at 10% interest. Benjamin has made 19 monthly payments of $531.18. Sarah won a new 2007 BMW 328i in a contest. The car has a current value of $12,575. Boat The current value of Benjamin's 18-foot boat with a 150 HP Mercury is $12,000. Though Benjamin and Sarah consider this a luxury item, they know that the sale of the boat may harm their relationship with Sarah's parents. Student Loans Benjamin put himself through school with part-time jobs and student loans. He originally borrowed money to pay for his education through a student loan program. He recently consolidated all of his student loans into one. The term of the loan is 10 years, and Benjamin is in his second year of payments. The current payment is $241.05 per month. Credit Cards Before marriage, Benjamin and Sarah each had their own credit cards, the balances of which are close to the maximum credit limits. After marriage, they applied for a joint credit card and planned to use it for emergencies only. The current interest rates, balances, limits, and annual fees on these cards are as follows. Interest Rate Balance Credit Limit Annual Fee Benjamin 18% $4,750 $5,000 $50 Sarah 23% $4,920 $5,000 $50 Joint 16% $1,200 $5,000 $50 Bank Loans During the past several years, Benjamin and Sarah have taken out loans to pay for vacations. The current payment is $604.27 per month. The balance of these loans is $9,909. To assist the Reddings with their immediate cash flow needs, you offer to loan them $20,000 at an annual interest rate of 10%. You explain that such a loan would allow them to pay off almost all of their credit cards and bank loans at a significantly reduced interest rate. You tell them they can repay the loan in full, if they wish, when they receive the expected gifts of $10,000 each from Benjamin's Great Aunt Mabel. Entertainment Because of Benjamin and Sarah's hectic work schedules and the three children, they rarely get to spend time alone together. Every Friday night, they go to a moder- ately priced restaurant for dinner. Sometimes they are joined by some of Benjamin's colleagues, and he uses this time to network. The approximate cost of dinner each Friday for Benjamin and Sarah is $50 including a gratuity. Friday nights are also a night out for the children. Delores brings the children to The Burger Barn for dinner. The approximate cost is $19 for all three children and Delores. Education Because of the quality of the schools in their state, Benjamin and Sarah want Scott, Janice, and Carly to go to private schools, but they are concerned about the cost. To assist in defraying the cost of educating the children, it is expected that all three children will attend Woodridge Preparatory School for K-12th grade. Sarah's position allows for tuition discounts (no additional multifamily discount) for teachers as follows: 50% discount on tuition for students in K-8th grades; and 75% discount on tuition for students in 9-12th grades. Current tuition is $3,665 per student per year. Tuition is expected to increase at 5% per year. Each child will begin kindergarten at age 5. Benjamin and Sarah would also like to provide financial assistance to their chil- dren while they attend college. They have decided to provide each child $15,000 (in today's dollars) per year for tuition, room, and board. Any additional funding will be provided by the trust, student loans, and part-time employment by the children. Today, tuition, fees, and other associated costs average $25,000 for a public university and are expected to increase at a rate of 5% per year. Each child is expected to begin college immediately after graduation from high school at age 18 and attend for four years. QUESTIONS 1. List the Reddings' financial strengths and weaknesses. 2. After reading the case, what additional information would you request from the Reddings to complete your data-gathering phase? 3. Calculate the following financial ratios for the Reddings. Liquid Assets Monthly Expenses Net Worth Total Assets Total Debt Total Assets Total Debt Annual Total Income* Annual Housing and Debt Payments Annual Gross Income Annual Housing Costs Annual Gross Income Investment Assets Annual Gross Income Annual Savings Annual Gross Income *Annual Total Income is the same as Annual Gross Income. 4. Comment on any of the above ratios that you think are important. 5. Briefly evaluate the Reddings' use of debt. 6. Assuming an earnings rate of 8%, calculate the amount needed today to fund the chil- dren's college education. 7. Assuming a rate of return of 8%, calculate the amount they need to save each month to fund the children's college education. Assume that savings will begin at the end of this month and continue until the youngest children begin college. 8. Assuming a rate of return of 8%, calculate the monthly savings needed for education assuming that savings will continue until the children's college education is completed. 9. Determine whether the Reddings will currently qualify to refinance their home. Is the house eligible for refinancing by a lender requiring a maximum loan-to-value ratio of 80%? How much cash would the Reddings need if they refinance? 10. Assuming that the Reddings decide to use their savings account to pay down the mort- gage so they are able to refinance their current mortgage, calculate the monthly pay- ment for each of the terms below. For purposes of this question, disregard whether the Reddings qualify to refinance their home. Assume they maintain the lender's loan-to- value ratio requirement. a. 15-year loan b. 30-year loan paid over 30 years c. 30-year loan paid over the remaining life of their current mortgage Calculate the total expected savings from the refinancing for each of the three loans mentioned in Question 10. Do they qualify for any of the loans in Question 10 if the bank requires a total housing cost ratio less than 28% and a total debt-to-payments income ratio of 36%? 13. If they do not qualify for any of the loans in Question 10 because the lender counts only $82,000 of income, what actions should they consider in order to qualify? 14. Calculate the total amount of money needed today to meet Julie's medical needs. Assume that she lives seven years and that the Reddings invest in corporate bonds. 15. How much do the Reddings need to save on a monthly basis beginning at the end of this month toward a down payment in order to purchase their future home for $300,000? Assume they invest at an interest rate equal to the expected return on the S&P 500 Index and pay all associated taxes out of their current budget. Does the trust fund of $100,000 belong on the Reddings' Statement of Financial Position? 17. What are the deficiencies in the presentation of the Statement of Financial Position? The Steiners decided to provide additional financial assistance to help with their grand- children's college education expenses. They planned to elect gift-splitting for any gifts they made, and they wanted to give as much as they could without incurring any gift tax. What was the maximum amount they could have contributed in 2016 and still have met these objectives using Coverdell Education Savings Accounts (CESAs) and Section 529 plans? 66 Personal Financial Planning: Cases & Applications Textbook 10th Edition 2017-2018 Benjamin and Sarah Redding have great aspirations for their future. They have only recently realized that they are not as financially secure as they had originally thought. They have come to you for advice on how to solve their current cash flow issues and to help them make plans to achieve their goals. Today is January 1, 2017. Personal Background and Information Benjamin Redding (Age 30) Benjamin Redding graduated from a state university seven years ago with a bach- elor of science degree in accounting. He has been employed for almost seven years at Moore & Moore, a small accounting firm (50 employees). Benjamin has been married to Sarah Steiner Redding for six years. Sarah Steiner Redding (Age 29) Sarah Steiner Redding grew up in a wealthy family. She graduated from a private university with a bachelor of science degree in elementary education. She is employed as a fourth grade teacher at a private school, Woodridge Preparatory School, and has been for the past five years. To further enrich her students (and for additional income), Sarah tutors three students each week. She incurs no expenses when providing this tutoring. Children Benjamin and Sarah have three children: Scott, age 4, and twin girls, Janice and Carly, age 1. Delores Vidalia The Reddings employ a young student, Delores Vidalia, to care for their children. Delores, age 21, is a part-time night student at a local community college. She cares for the children and cleans the Reddings' house in exchange for room, board, and a $100 stipend per week. The Reddings pay Delores in cash. Neither the Reddings nor Dolores report these transactions to the IRS. Delores works 48 weeks per year. Benjamin's Family George Redding married Julie Redding in 1985. They had two children, George Jr., and Benjamin. George Jr., died at age six months of sudden infant death syndrome. Benjamin's father, George Sr., died of a heart attack six years ago at age 50. He had ample insurance to cover all medical and funeral expenses. His mother, Julie, a chain-smoker for 37 years, is 53 years old. She was diagnosed with lung cancer three years ago. Because of her rapidly deteriorating health, her doc- tor has predicted that she probably will not live beyond five to seven years. She is receiving monthly chemotherapy treatments at a medical center ($200 out-of-pocket cost per visit). Her doctor has recommended that she be placed in a home with 24-hour care as soon as possible. The cost of this care, including room and board, is about $175 per day, or approximately $5,323 per month. Because of her increased medical expenses and need for constant care, Julie has decided to sell her home. She has contacted Jane Smith, a real estate agent, who has listed her home for $140,000. Julie is adamant that she will accept no less than $135,000. Benjamin and Sarah have been giving Julie $200 per month to help ease her finan- cial burden. They will be forced to incur most of her future expenses. They realize that the sale of the home will provide some assistance; however, the real estate market is soft, and they have had no offers on the house. Julie owns a paid-up whole life insur- ance policy on her own life with a face amount of $500,000 and a cash surrender value (CSV) of $75,000. The policy is not a modified endowment contract (MEC). Benjamin's Great Aunt Mabel plans to give Benjamin and Sarah $10,000 each at the beginning of 2017. Benjamin has always looked out for Mabel, and she wants to show him her gratitude through this gift. Sarah's Family Harry Steiner III married Alice Steiner in 1972. Sarah is an only child and the Steiners' pride and joy. Harry Steiner is a highly respected State Supreme Court justice. He has worked in the city for more than 30 years and is considered an extremely influential figure in the community. Harry and Alice's adjusted gross income (AGI) exceeds $275,000. Alice Steiner was born into a wealthy family. Before they were married, she and Harry decided that she would not work. She is, however, very active in the community through her volunteer work four days a week. The Steiners were happy to welcome Benjamin into their family. In fact, Harry was so excited that he presented Benjamin with a speedboat in hopes that he would get to spend time on the boat getting to know his future son-in-law. As a wedding gift, the Steiners gave Sarah and Benjamin $20,000 toward the purchase of a new home. In addition, the Steiners set up a $100,000 trust fund to assist their grandchildren with college education expenses. Sarah, the beneficiary of the trust fund, receives the monthly interest from the principal until the trust is dissolved, with first Benjamin and then Children's Hospital as successor beneficiaries in the event of Sarah's death. Upon Scott's enrollment in college, he will be given his third of the trust fund, $33,333. Sarah will continue to receive the interest on the remaining $66,666 until Janice and Carly begin college. If a child should die or decide not to go to college by age 22, that child's share would be donated to Children's Hospital. Benjamin was previously married to Carol, an attorney, and together they had one child, Stephen. Benjamin pays Carol $500 each month for child support. Carol's par- ents have agreed to pay 100% of Stephen's college tuition and expenses. Personal and Financial Objectives The Reddings listed the following financial objectives in direct order of importance to their family. 1. Provide private education for all three children at Woodridge Preparatory School for grades K-12. 2. Provide each child with up to $15,000 per year for college education for up to four years in addition to the trust fund. 3. Assist Julie with living and medical expenses until her death. 4. Purchase a home for $300,000 in eight years with a 20% down payment. (By that time, Benjamin should be a partner of the firm.) Housing costs are expected to increase with inflation. They intend to keep their current home as a rental prop- erty. 5. Be free of mortgage indebtedness by the time Benjamin is 55 years old. 6. Prepare a proper retirement plan allowing them a debt-free retirement. They feel that income of $75,000 in today's dollars per year will allow them to maintain their standard of living. 7. Rebuild their savings account/emergency fund to a minimum of $25,000. 8. Save for the twins' future weddings (estimated costs $15,000 each). Economic Information They expect inflation to average 4% annually. They expect Sarah's salary to increase each year by 5%. They expect Benjamin's salary to increase each year by 5%. Mortgage rates are 5.5% for a 15-year fixed and 6.0% for a 30-year fixed. Any refinancing will incur 3% of the mortgage amount as a closing cost. Insurance Information Health Insurance An HMO health insurance plan is provided for the entire family by Moore & Moore. Doctor visits are $10 per visit, while prescriptions are $5 for generic brands and $10 for other brands. There is no co-payment for hospitalization in semiprivate accommodations. Private rooms are provided when medically necessary. For emergency treatment, a $50 co-payment is required. Life Insurance Benjamin has a $110,000 group term life insurance policy through Moore & Moore. Highly compensated employees of Moore & Moore receive group term coverage in the amount of five times their salaries. Sarah has a $27,000 group term life insurance policy through Woodridge Preparatory School. The owners of the policies are Benjamin and Sarah, respectively, with each other as the beneficiary. Disability Insurance Benjamin has disability insurance through Moore & Moore. Short-term disability benefits begin for any absence due to sickness and accident more than six days and will continue for up to six months at 80% of his salary. Long-term disability benefits are available if disability continues more than six months. If Benjamin is unable to per- form the major and substantial duties of his current occupation, the coverage provides him with 60% of his salary while disabled until recovery, death, retirement, or age 65 (whichever occurs first). All disability insurance premiums are fully paid by Moore & Moore. Sarah has no disability insurance. Professional Liability Insurance Moore & Moore has professional liability insurance covering all employees. Homeowners Insurance The Reddings have an HO-3 policy with a $140,000 dwelling coverage limit and liability coverage of $100,000 endorsed to provide loss settlement on a replacement cost basis for personal property. Dwelling coverage is provided on an open peril basis and per- sonal property coverage is provided on a named peril basis. The deductible is $500 with an annual premium of $750. Automobile Insurance Benjamin and Sarah have the following coverage on both cars: $100,000 bodily injury per person; $300,000 bodily injury aggregate; $50,000 property damage; $100,000 uninsured motorist per person; and $300,000 uninsured motorist aggregate. Deductibles are: $500 comprehensive (no deductible for glass); and $1,000 collision. This insurance includes medical payments, car rentals, and towing. The cost of the auto insurance is $3,260.50 per year because of two at-fault accidents Sarah has caused in the past three years. Investment Information (Prospective) Expected Return Beta Aggressive stocks 13% 1.6 Growth stocks 10% 1.1 S&P 500 Index 9% 1.0 Corporate bonds 7% 0.5 Money market (bank) 2% 0.3 The Reddings consider themselves to be moderate risk investors. Income Tax Information The Reddings are in the 15% marginal income tax bracket. Their combined mar- ginal income tax bracket (federal and state) is 18%. Retirement Information Benjamin and Sarah would both like to retire when they are 65 and 64 years old, respectively, and they expect to be in retirement for 30 years. They would hope to have $75,000 per year of pretax income in today's dollars during retirement. They do not want to rely on Social Security benefits for their retirement planning. Any money received from Social Security will be considered extra income. Benjamin does not participate in the Section 401(k) plan available through Moore & Moore. In the plan, the firm matches $.50 for every dollar contributed, up to 6% of his contribution (if he contributes 6% of his salary, the company contributes 3%). Benjamin may defer a maximum of 16% of his salary. Sarah is enrolled in a defined contribution plan in which the school contributes 7% of her salary and she contributes 3%. The plan provides several investment options: bond funds, stock funds, and money market accounts. She has chosen to invest this contribution in fixed instruments (bond funds). The plan has a 2- to 6-year graduated vesting schedule, and she has been a participant for four years. The total balance of her account is $16,500. Although she has not participated, she also has available a Section 403 (b) supplemental retirement plan to which she may contribute up to 13% of her salary. Gifts, Estates, Trusts, and Will Information Presently, neither Benjamin nor Sarah have wills; however, both realize the importance of having them. They would like to create wills leaving everything to one another and the children, while minimizing the impact of both estate and gift taxes. STATEMENT OF CASH FLOWS Benjamin and Sarah Redding 2016 (Expected to be the same for 2017) $55,000.00 27,000.00 3,600.00 3,000.00 5,569.80 $ 810.00 12,798.24 1,250.00 6,273.00 11,078.20 903.95 5,400.00 750.00 6,374.16 3,490.00 3,260.50 4,800.00 2,892.60 2,170.08 7,251.25 900.00 3,550.00 6,000.00 3,600.00 3,600.00 6,000.00 CASH INFLOWS Salary-Benjamin Salary-Sarah Tutoring-Sarah Interest trust Savings account withdrawal Total inflows CASH OUTFLOWS Defined contribution plan-Sarah Mortgage payment (principal and interest) Property taxes (residence) FICA Federal withholding State withholding Utilities Homeowners insurance Auto note Auto expense/maintenance Auto insurance Child care/House care Education loans4 Credit card payments5 Bank loans Dry cleaning New clothing Food Dining out/entertainment Miscellaneous Child support payment to Carol Total Outflows Net Cash Flow (Surplus) Notes to Financial Statements Sarah does not report this money to the IRS. 2$366 is earned interest. The Reddings pay the maid in cash and do not report it to the IRS. 4$1,643 is interest, the balance is principal. "The Reddings pay the minimum monthly payment on credit cards. 6$4,350 is interest, the balance is principal. $94,169.80 $93,151.98 $ 1,017.82 STATEMENT OF FINANCIAL POSITION Benjamin and Sarah Redding January 1, 2017 ASSETS Checking account $ 10,000 Savings account 13,500 Trust fund 100,000 Automobile-Sarah (2007 BMW 328i) 12,575 Automobile-Benjamin (2015 Nissan Maxima) 16,375 Boat 12,000 Home (appraised 7/1/16) 149,000 Pension-Sarah 16,500 Total assets $329,950 LIABILITIES 3,4 Credit card-Benjamin (18%) $4,750 Credit card-Sarah (23%) 4,920 Credit card-joint (16%) 1,200 Car loan-Benjamin (10%) 18,383 Student loans (6%) 17,919 Bank loans (12%) 9,909 Home mortgage balance (7.5%) 148,944 Total liabilities $206,025 $123,925 Net worth Total liabilities and net worth $329,950 Notes to Financial Statements 'All assets are stated at fair market value. The trust fund is for the children's education; however, Sarah receives the interest on the balance of the trust fund until all children reach age of majority. The trust assets are invested in a CD yielding 3% per year. Liabilities are stated at principal only. 4Percentages shown (%) are current interest rates on respective indebtedness. Information Regarding Assets and Liabilities Employment Benjamin is currently employed as a senior accountant at Moore & Moore, earning an annual salary of $55,000. He expects to be promoted to manager within two years. Benjamin hopes to be a partner in eight years. Sarah earns $27,000 annually teaching at Woodridge Preparatory School. Annual salary increases range from 3-5%. She also earns approximately $3,600 each year tutor- ing. This money is received in cash. Although they should, she and Benjamin do not report her tutoring earnings on their tax returns. In addition, Sarah receives $3,000 a year, before taxes, on the interest earned from the children's trust fund. Benjamin and Sarah earn approximately 2% interest on their savings account. This is automatically credited on a quarterly basis to the account; however, they do not consider this small amount of interest to be income. This savings account/emergency fund began with an account balance of $25,000 when they were first married. In 2016, they withdrew $366 in interest income and $5,203.80 from the savings account to pay bills. Home Benjamin and Sarah purchased a four-bedroom house for $170,000 in a nice fam- ily neighborhood. They were among the first families to purchase a home in this new subdivision. The money received from Sarah's parents as a wedding gift was used for the down payment. The mortgage payment is $1,066.52 per month. The interest rate is 7.5%. The original mortgage was $152,531.47, and they have made 29 payments. Utilities range from $400-500 per month. Although the original value of the house was $170,000, a recent appraisal valued the house at $149,000. The decrease in value did not leave enough equity for the Reddings to be approved for a home equity loan. If the Reddings wanted to refinance (80% of the fair market value of the home), the 3% closing costs would have to be paid at closing and not financed. Automobiles In 2015, Benjamin purchased a new Nissan Maxima for $25,000. The current value of the car is $16,375, but the loan balance is $18,383.47. The term of the loan is 60 months at 10% interest. Benjamin has made 19 monthly payments of $531.18. Sarah won a new 2007 BMW 328i in a contest. The car has a current value of $12,575. Boat The current value of Benjamin's 18-foot boat with a 150 HP Mercury is $12,000. Though Benjamin and Sarah consider this a luxury item, they know that the sale of the boat may harm their relationship with Sarah's parents. Student Loans Benjamin put himself through school with part-time jobs and student loans. He originally borrowed money to pay for his education through a student loan program. He recently consolidated all of his student loans into one. The term of the loan is 10 years, and Benjamin is in his second year of payments. The current payment is $241.05 per month. Credit Cards Before marriage, Benjamin and Sarah each had their own credit cards, the balances of which are close to the maximum credit limits. After marriage, they applied for a joint credit card and planned to use it for emergencies only. The current interest rates, balances, limits, and annual fees on these cards are as follows. Interest Rate Balance Credit Limit Annual Fee Benjamin 18% $4,750 $5,000 $50 Sarah 23% $4,920 $5,000 $50 Joint 16% $1,200 $5,000 $50 Bank Loans During the past several years, Benjamin and Sarah have taken out loans to pay for vacations. The current payment is $604.27 per month. The balance of these loans is $9,909. To assist the Reddings with their immediate cash flow needs, you offer to loan them $20,000 at an annual interest rate of 10%. You explain that such a loan would allow them to pay off almost all of their credit cards and bank loans at a significantly reduced interest rate. You tell them they can repay the loan in full, if they wish, when they receive the expected gifts of $10,000 each from Benjamin's Great Aunt Mabel. Entertainment Because of Benjamin and Sarah's hectic work schedules and the three children, they rarely get to spend time alone together. Every Friday night, they go to a moder- ately priced restaurant for dinner. Sometimes they are joined by some of Benjamin's colleagues, and he uses this time to network. The approximate cost of dinner each Friday for Benjamin and Sarah is $50 including a gratuity. Friday nights are also a night out for the children. Delores brings the children to The Burger Barn for dinner. The approximate cost is $19 for all three children and Delores. Education Because of the quality of the schools in their state, Benjamin and Sarah want Scott, Janice, and Carly to go to private schools, but they are concerned about the cost. To assist in defraying the cost of educating the children, it is expected that all three children will attend Woodridge Preparatory School for K-12th grade. Sarah's position allows for tuition discounts (no additional multifamily discount) for teachers as follows: 50% discount on tuition for students in K-8th grades; and 75% discount on tuition for students in 9-12th grades. Current tuition is $3,665 per student per year. Tuition is expected to increase at 5% per year. Each child will begin kindergarten at age 5. Benjamin and Sarah would also like to provide financial assistance to their chil- dren while they attend college. They have decided to provide each child $15,000 (in today's dollars) per year for tuition, room, and board. Any additional funding will be provided by the trust, student loans, and part-time employment by the children. Today, tuition, fees, and other associated costs average $25,000 for a public university and are expected to increase at a rate of 5% per year. Each child is expected to begin college immediately after graduation from high school at age 18 and attend for four years. QUESTIONS 1. List the Reddings' financial strengths and weaknesses. 2. After reading the case, what additional information would you request from the Reddings to complete your data-gathering phase? 3. Calculate the following financial ratios for the Reddings. Liquid Assets Monthly Expenses Net Worth Total Assets Total Debt Total Assets Total Debt Annual Total Income* Annual Housing and Debt Payments Annual Gross Income Annual Housing Costs Annual Gross Income Investment Assets Annual Gross Income Annual Savings Annual Gross Income *Annual Total Income is the same as Annual Gross Income. 4. Comment on any of the above ratios that you think are important. 5. Briefly evaluate the Reddings' use of debt. 6. Assuming an earnings rate of 8%, calculate the amount needed today to fund the chil- dren's college education. 7. Assuming a rate of return of 8%, calculate the amount they need to save each month to fund the children's college education. Assume that savings will begin at the end of this month and continue until the youngest children begin college. 8. Assuming a rate of return of 8%, calculate the monthly savings needed for education assuming that savings will continue until the children's college education is completed. 9. Determine whether the Reddings will currently qualify to refinance their home. Is the house eligible for refinancing by a lender requiring a maximum loan-to-value ratio of 80%? How much cash would the Reddings need if they refinance? 10. Assuming that the Reddings decide to use their savings account to pay down the mort- gage so they are able to refinance their current mortgage, calculate the monthly pay- ment for each of the terms below. For purposes of this question, disregard whether the Reddings qualify to refinance their home. Assume they maintain the lender's loan-to- value ratio requirement. a. 15-year loan b. 30-year loan paid over 30 years c. 30-year loan paid over the remaining life of their current mortgage Calculate the total expected savings from the refinancing for each of the three loans mentioned in Question 10. Do they qualify for any of the loans in Question 10 if the bank requires a total housing cost ratio less than 28% and a total debt-to-payments income ratio of 36%? 13. If they do not qualify for any of the loans in Question 10 because the lender counts only $82,000 of income, what actions should they consider in order to qualify? 14. Calculate the total amount of money needed today to meet Julie's medical needs. Assume that she lives seven years and that the Reddings invest in corporate bonds. 15. How much do the Reddings need to save on a monthly basis beginning at the end of this month toward a down payment in order to purchase their future home for $300,000? Assume they invest at an interest rate equal to the expected return on the S&P 500 Index and pay all associated taxes out of their current budget. Does the trust fund of $100,000 belong on the Reddings' Statement of Financial Position? 17. What are the deficiencies in the presentation of the Statement of Financial Position? The Steiners decided to provide additional financial assistance to help with their grand- children's college education expenses. They planned to elect gift-splitting for any gifts they made, and they wanted to give as much as they could without incurring any gift tax. What was the maximum amount they could have contributed in 2016 and still have met these objectives using Coverdell Education Savings Accounts (CESAs) and Section 529 plans

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts