Answer the following by showing the computations:

Partnership Dissolution

ratio of 3:2. They have a desperate need for cash and they agree to admit Andre as a new partner with a 1/3 interest in both capital and profits upon the latter's capital infusion of P30,000. No goodwill is to be recognized. After Andre's admission, the respective capital balances of Ming, Piw and Andre are: a. 50,000, 50,000 & 50,000. c. 68,000, 32,000 & 50,000. b. 66,667, 33,333 & 50,000. d. 80,000, 40,000 & 30,000. (RPCPA - Adapted) 9. Blau and Rubi are partners who share profits and losses in the ratio of 6:4, respectively. On May 1, 2003, their respective capital accounts were as follows: Blau 60,000 Rubi 50,000 On that date, Lind was admitted as a partner with a one-third interest in capital and profits for an investment of P40,000. The new partnership began with a total capital of P150,000. Immediately after Lind's admission, Blau's capital should be a. 50,000. c. 56,667. b. - 54,000. (AICPA) d. 60,000. Use the following information for items 10 and 11: The partners in ABC Co. had the following capital balances and P/L sharing percentages: A (50%) P320,000; B (30%) P192,000; and C (20%) P128,000. 10. A decided to retire and sold his interest to B for P360,000. The entry on A's retirement included a a. debit to B's capital for P24,000. b. debit to C's capital for P16,000. c. credit to B's capital for P360,000. d. credit to B's capital for P320,000.The following adjustments are determined: The recoverable amount of the accounts receivable is P116,400. A P25,000 recovery of a previous write-down on the inventory should be recognized. Prepaid assets of P3,600 and accrued liabilities of P4,000 should be recognized. (AICPA - Adapted) 1. C acquires half of B's interest in the partnership for P100,000. How much is the capital balance of B after the admission of C? a. 47,000 c. 51,200 b. 21,500 d. 182,600 2. C invests P71,250 cash for a 20% interest in the net assets and profits of the partnership. C's capital account is credited for the fair value of the 20% interest he acquired. How much is the capital balance of B after the admission of C? a. 102,400 c. 86,400 b. 94,000 d. 120,400 3. C invests P100,000 cash for a 20% interest in the partnership's net assets and profits. If the bonus method is used, how much is the capital balance of B after the admission of C? a. 165,350 c. 100,000 b. 111,600 d. 77,000 4. If no bonus is allowed, how much should C invest in order to obtain 2/5 interest in the partnership? a. 190,000 c. 285,000 b. 185,000 d. 220,000 5. A, B and C are partners with the following capital balances and interests: A (20%) P50,000; B (30%) P70,000; and C (50%) P130,000. D purchases 10% partnership interest from A and B for P30,000. How much would be credited to D's capital under the following scenarios?Cha b. reduction in capital of P7,500 each for A and B only. c. reduction in capital of P15,000 for C. d. reduction in capital of P55,000 for C. (RPCPA) 15. The amount of the note issued to C is a. 120,000. .c. 145,000. b. 135,000. d. 150,000. (RPCPA)11. A withdrew and the partnership paid him P360,000. How much is the capital balance of C after A's withdrawal? a. 112,000 c. 168,000 b. 116,800 d. 172,000 12. ABC Partnership's net assets were P1,000,000 as of Jan. 1, 20x1. Partner A retires from the partnership on June 30, 20x1. The partnership earned profit of P300,000 for the six months ended June 30, 20x1. Partners A, B and C share profits and losses equally. If Partner A was paid P200,000 for his interest in the partnership, how much is the adjusted net assets of the partnership immediately after Partner A's retirement? (No goodwill is recognized.) a. 800,000 c. 1,100,000 b. 900,000 d. Answer cannot be determined 13. The net assets of ABC Co. on June 30, 20x1 before closing entries consisted of the following: A (20%), P300,000; B (30%), P500,000; and C (50%), P200,000. Profit for the six months ended June 30, 20x1 was P1,800,000. C withdraws on July 1, 20x1 and receives P1,000,000 cash and fully depreciated equipment with fair value of P600,000 from the partnership. What is the capital balance of A right after C's withdrawal? a. 780,000 c. 700,000 b. 1,220,000 d. 1,800,000 Use the following information for items 14 and 15: A, B and C are partners with capital balances of P300,000, P300,000 and P200,000, respectively. The partners share in profits and losses equally. C is to retire and it is agreed that he would take furniture with carrying amount of P65,000 and a note for the balance of his interest. The fair value of the furniture is P50,000; however, a brand-new furniture would cost P80,000. 14. C's acquisition of the furniture would result in a. reduction in capital of P5,000 each for A and B only..

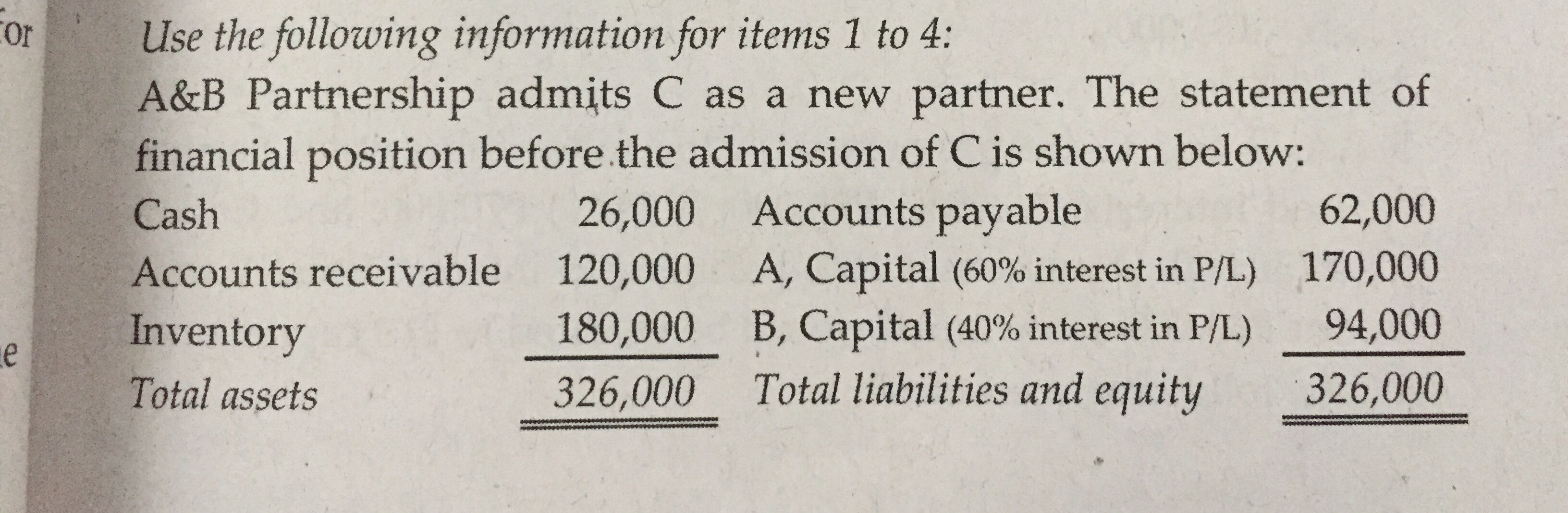

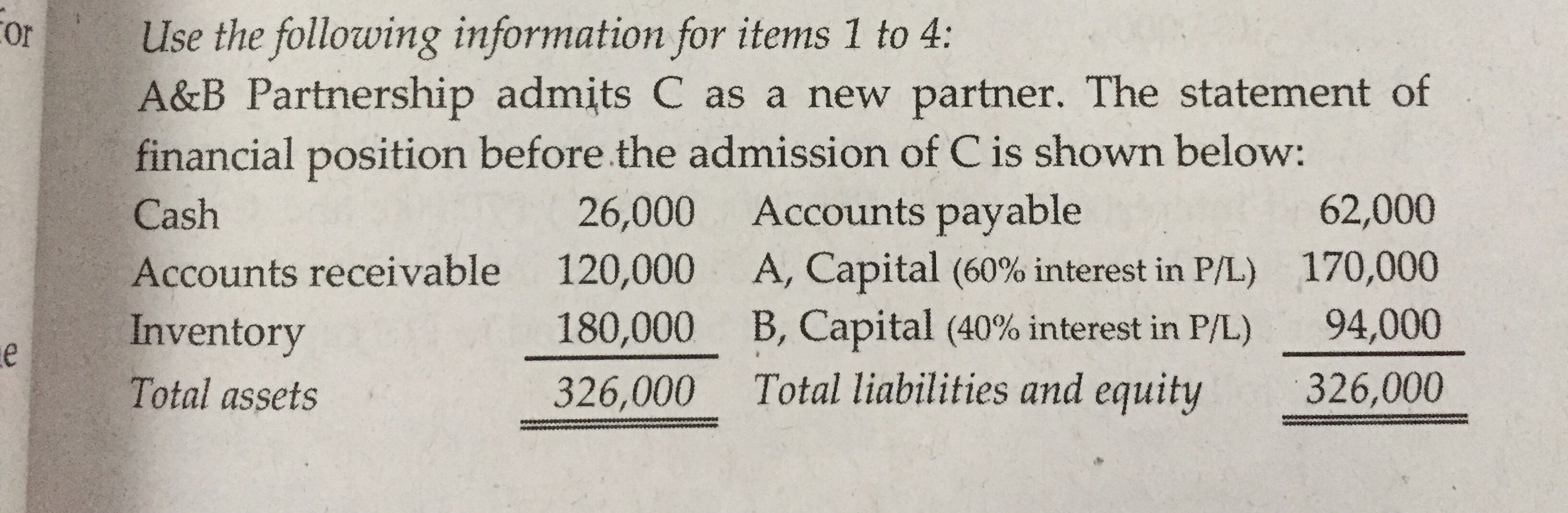

D's capital credit is based on the book values of the selling partners' capital balances. . D's capital credit reflects the fair value of his interest in the partnership's net assets. The partnership's net assets on D's admission date are fairly valued. a. 12,000 25,000 c. 25,000 30,000 b. 25,000 12,000 d. 12,000 30,000 6. The admission of a new partner to a 20% interest in a partnership for an investment of P18,000, but with a capital credit based on P75,000 total contributed capital, will result in a. . bonus to the old partners. b. bonus to the new partner. c. goodwill to the old partners. d. goodwill to the new partner. (RPCPA - Adapted) 7. The capital accounts and profit and loss sharing ratios of A, B and C are as follows: Capital PIL 139,200 1/2 B 208,800 1/3 96,000 1/6 On this date, D is admitted to the partnership when he purchased, for P132,000, a proportionate interest from A and B in the net assets and profits of the partnership. As a result of the transaction, D acquired one-fifth interest in the net assets and profits of the firm. What is the combined gain realized by A and B upon the sale of a portion of their interest in the partnership to D? a. 0 b. 43,200 c. 62,400 (AICPA) d. 82,000 8. The capital balances of partners Ming and Piw are P80,000 and P40,000, respectively. They share in profits and losses in theOr Use the following information for items 1 to 4: A&B Partnership admits C as a new partner. The statement of financial position before the admission of C is shown below: Cash 26,000 Accounts payable 62,000 Accounts receivable 120,000 A, Capital (60% interest in P/L) 170,000 e Inventory 180,000 B, Capital (40% interest in P/L) 94,000 Total assets 326,000 Total liabilities and equity 326,000