Answer the following problems

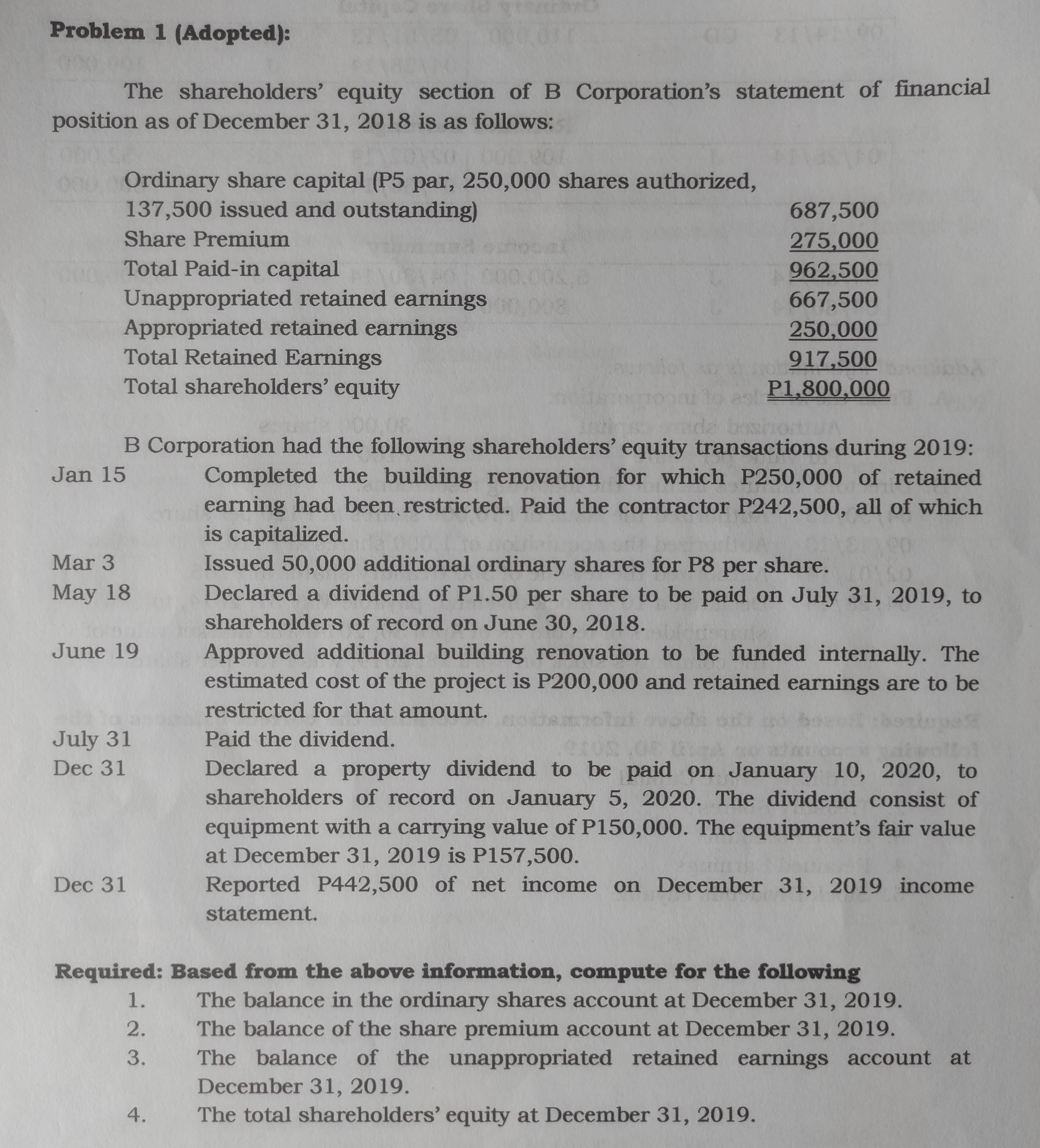

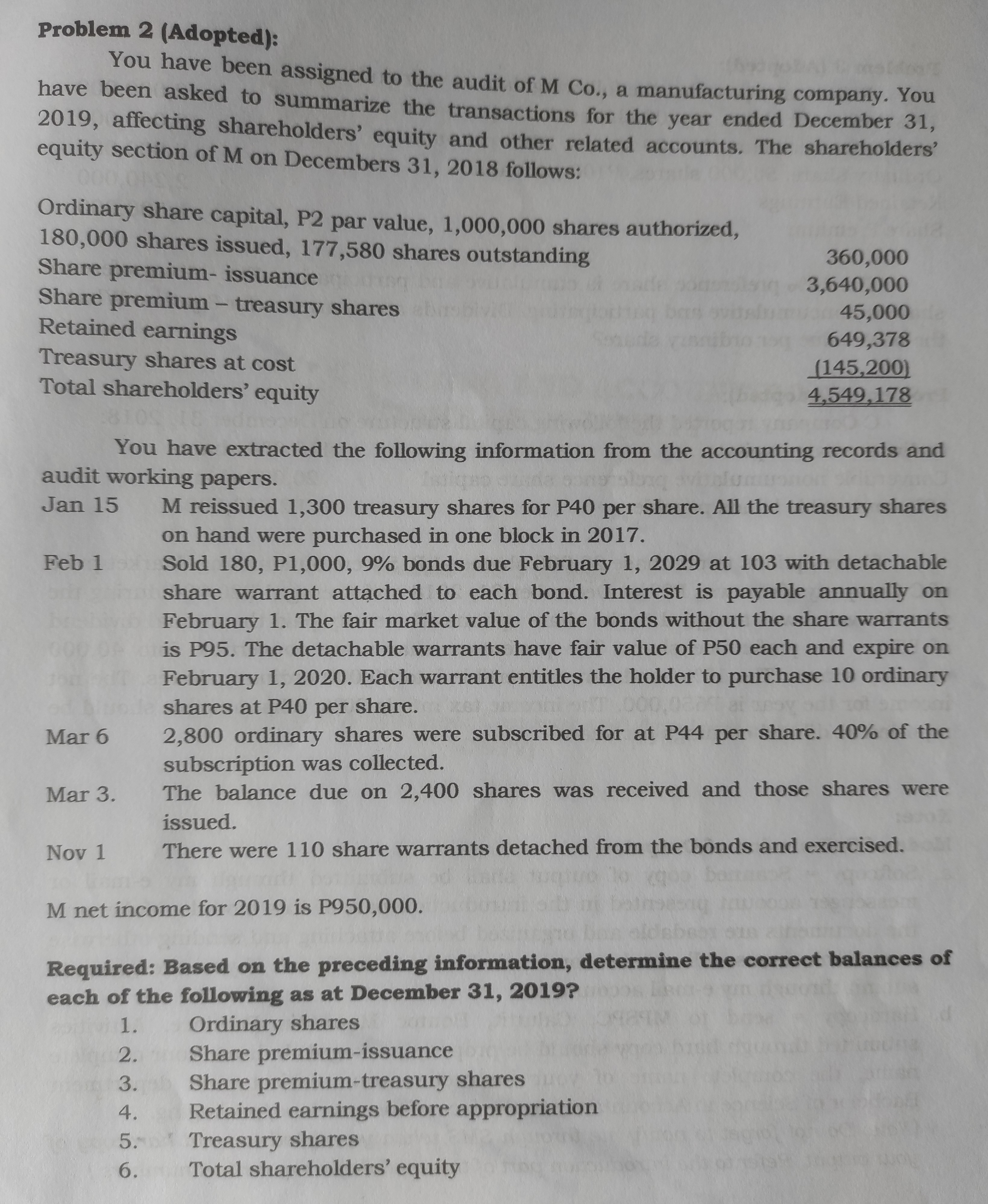

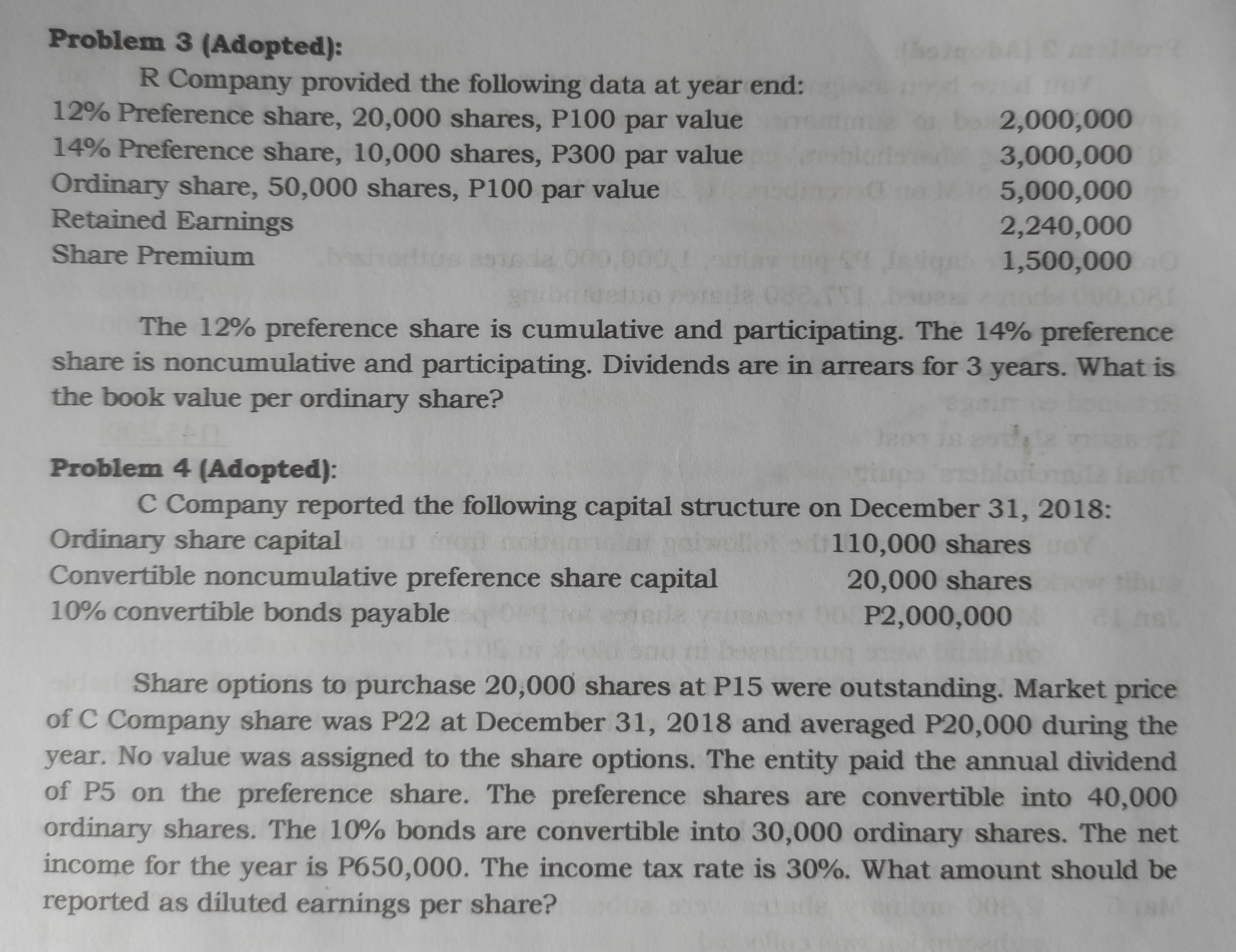

Problem 1 (Adopted): The shareholders' equity section of B Corporation's statement of financial position as of December 31, 2018 is as follows: Ordinary share capital (P5 par, 250,000 shares authorized, 137,500 issued and outstanding) 687,500 Share Premium 275,000 Total Paid-in capital 00.00 962,500 Unappropriated retained earnings 667,500 Appropriated retained earnings 250,000 Total Retained Earnings 917,500 Total shareholders' equity P1,800,000 B Corporation had the following shareholders' equity transactions during 2019: Jan 15 Completed the building renovation for which P250,000 of retained earning had been restricted. Paid the contractor P242,500, all of which is capitalized. Mar 3 Issued 50,000 additional ordinary shares for P8 per share. May 18 Declared a dividend of P1.50 per share to be paid on July 31, 2019, to shareholders of record on June 30, 2018. June 19 Approved additional building renovation to be funded internally. The estimated cost of the project is P200,000 and retained earnings are to be restricted for that amount. July 31 Paid the dividend. Dec 31 Declared a property dividend to be paid on January 10, 2020, to shareholders of record on January 5, 2020. The dividend consist of equipment with a carrying value of P150,000. The equipment's fair value at December 31, 2019 is P157,500. Dec 31 Reported P442,500 of net income on December 31, 2019 income statement. Required: Based from the above information, compute for the following 1. The balance in the ordinary shares account at December 31, 2019. 2 . The balance of the share premium account at December 31, 2019. 3 . The balance of the unappropriated retained earnings account at December 31, 2019. 4. The total shareholders' equity at December 31, 2019.Problem 2 (Adopted): You have been assigned to the audit of M Co., a manufacturing company. You have been asked to summarize the transactions for the year ended December 31, 2019, affecting shareholders' equity and other related accounts. The shareholders' equity section of M on Decembers 31, 2018 follows: Ordinary share capital, P2 par value, 1,000,000 shares authorized, 180,000 shares issued, 177,580 shares outstanding 360,000 Share premium- issuance 3,640,000 Share premium - treasury shares 45,000 Retained earnings 649,378 Treasury shares at cost (145,200) Total shareholders' equity 4,549,178 You have extracted the following information from the accounting records and audit working papers. Jan 15 M reissued 1,300 treasury shares for P40 per share. All the treasury shares on hand were purchased in one block in 2017. Feb 1 Sold 180, P1,000, 9% bonds due February 1, 2029 at 103 with detachable share warrant attached to each bond. Interest is payable annually on February 1. The fair market value of the bonds without the share warrants is P95. The detachable warrants have fair value of P50 each and expire on February 1, 2020. Each warrant entitles the holder to purchase 10 ordinary shares at P40 per share. Mar 6 2,800 ordinary shares were subscribed for at P44 per share. 40% of the subscription was collected. Mar 3. The balance due on 2,400 shares was received and those shares were issued. Nov 1 There were 110 share warrants detached from the bonds and exercised. bor M net income for 2019 is P950,000. Required: Based on the preceding information, determine the correct balances of each of the following as at December 31, 2019? 1. Ordinary shares 2 . Share premium-issuance 3. Share premium-treasury shares 4 . Retained earnings before appropriation 5. Treasury shares 6 . Total shareholders' equityProblem 3 (Adopted): R Company provided the following data at year end: 12% Preference share, 20,000 shares, P100 par value 2,000,000 14% Preference share, 10,000 shares, P300 par value 3,000,000 Ordinary share, 50,000 shares, P100 par value 5,000,000 Retained Earnings 2,240,000 Share Premium 1,500,000 The 12% preference share is cumulative and participating. The 14% preference share is noncumulative and participating. Dividends are in arrears for 3 years. What is the book value per ordinary share? Problem 4 (Adopted): C Company reported the following capital structure on December 31, 2018: Ordinary share capital 110,000 shares or Convertible noncumulative preference share capital 20,000 shares Frow fiber 10% convertible bonds payable P2,000,000 Share options to purchase 20,000 shares at P15 were outstanding. Market price of C Company share was P22 at December 31, 2018 and averaged P20,000 during the year. No value was assigned to the share options. The entity paid the annual dividend of P5 on the preference share. The preference shares are convertible into 40,000 ordinary shares. The 10% bonds are convertible into 30,000 ordinary shares. The net income for the year is P650,000. The income tax rate is 30%. What amount should be reported as diluted earnings per share