Question

Answer the following questions: a. How much goodwill will be attributed to Paris? How much to the non-controlling shareholders? Did Paris pay a control premium,

Answer the following questions:

a. How much goodwill will be attributed to Paris? How much to the non-controlling shareholders? Did Paris pay a control premium, and if so how much?

b. Write all the 2015 equity method journal entries that Paris makes for its internal books. Identify what each entry is for.

c. Directly calculate the Equity Investment balance at the beginning of 2015. Show your work.

d. Write all the necessary 2015 consolidating entries necessary to generate the firms consolidated financial statements.

e. Write the I entries Paris must make for the equipment purchase in 2013?

f. Complete Pariss 2015 consolidated statements.

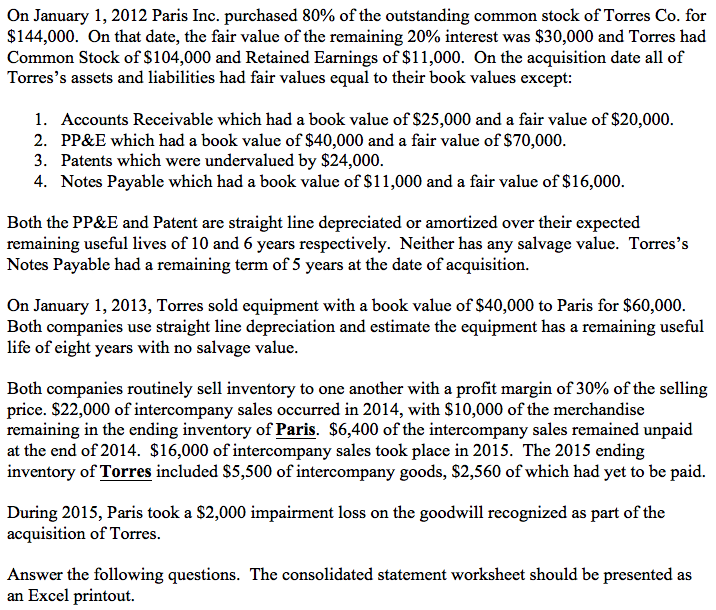

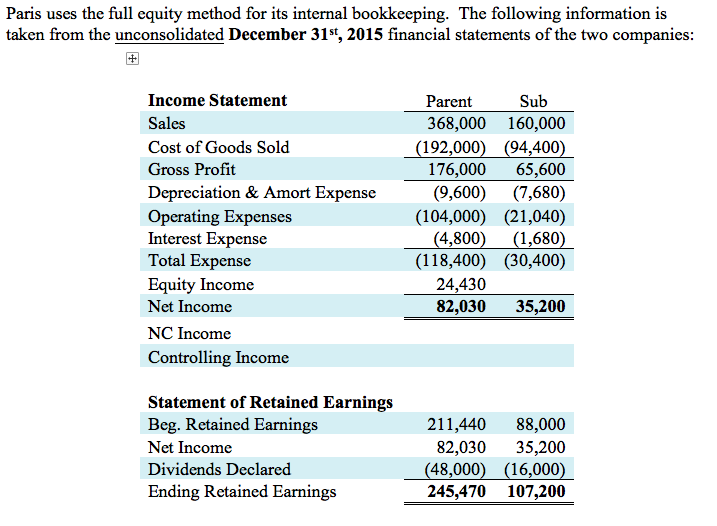

On January 1, 2012 Paris Inc. purchased 80% of the outstanding common stock of Torres Co. for $144,000. On that date, the fair value of the remaining 20% interest was $30,000 and Torres had Common Stock of S104,000 and Retained Earnings of $11,000. On the acquisition date all of Torres's assets and liabilities had fair values equal to their book values except 1. Accounts Receivable which had a book value of $25,000 and a fair value of $20,000 2. PP&E which had a book value of $40,000 and a fair value of S70,000 3. Patents which were undervalued by $24,000 4. Notes Payable which had a book value of S11,000 and a fair value of $16,000 Both the PP&E and Patent are straight line depreciated or amortized over their expected remaining useful lives of 10 and 6 years respectively. Neither has any salvage value. Torres's Notes Payable had a remaining term of 5 years at the date of acquisition. On January 1, 2013, Torres sold equipment with a book value of $40,000 to Paris for $60,000 Both companies use straight line depreciation and estimate the equipment has a remaining useful life of eight years with no salvage value Both companies routinely sell inventory to one another with a profit margin of 30% of the selling price. $22,000 of intercompany sales occurred in 2014, with $10,000 of the merchandise remaining in the ending inventory of Paris. $6,400 of the intercompany sales remained unpaid at the end of 2014. S16,000 of intercompany sales took place in 2015. The 2015 ending inventory of Torres included S5,500 of intercompany goods, $2,560 of which had yet to be paid. During 2015, Paris took a $2,000 impairment loss on the goodwill recognized as part of the acquisition of Torres Answer the following questions. The consolidated statement worksheet should be presented as an Excel printout. On January 1, 2012 Paris Inc. purchased 80% of the outstanding common stock of Torres Co. for $144,000. On that date, the fair value of the remaining 20% interest was $30,000 and Torres had Common Stock of S104,000 and Retained Earnings of $11,000. On the acquisition date all of Torres's assets and liabilities had fair values equal to their book values except 1. Accounts Receivable which had a book value of $25,000 and a fair value of $20,000 2. PP&E which had a book value of $40,000 and a fair value of S70,000 3. Patents which were undervalued by $24,000 4. Notes Payable which had a book value of S11,000 and a fair value of $16,000 Both the PP&E and Patent are straight line depreciated or amortized over their expected remaining useful lives of 10 and 6 years respectively. Neither has any salvage value. Torres's Notes Payable had a remaining term of 5 years at the date of acquisition. On January 1, 2013, Torres sold equipment with a book value of $40,000 to Paris for $60,000 Both companies use straight line depreciation and estimate the equipment has a remaining useful life of eight years with no salvage value Both companies routinely sell inventory to one another with a profit margin of 30% of the selling price. $22,000 of intercompany sales occurred in 2014, with $10,000 of the merchandise remaining in the ending inventory of Paris. $6,400 of the intercompany sales remained unpaid at the end of 2014. S16,000 of intercompany sales took place in 2015. The 2015 ending inventory of Torres included S5,500 of intercompany goods, $2,560 of which had yet to be paid. During 2015, Paris took a $2,000 impairment loss on the goodwill recognized as part of the acquisition of Torres Answer the following questions. The consolidated statement worksheet should be presented as an Excel printoutStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Guide To Audit Data Analytics

Authors: AICPA

1st Edition

1945498641, 978-1945498640