Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Answer the following questions about LIABILITY INSURANCE: - Provide correct calculations of the current position - Provide applicable recommendations and a hood explanation Thanks! MINI

Answer the following questions about LIABILITY INSURANCE:

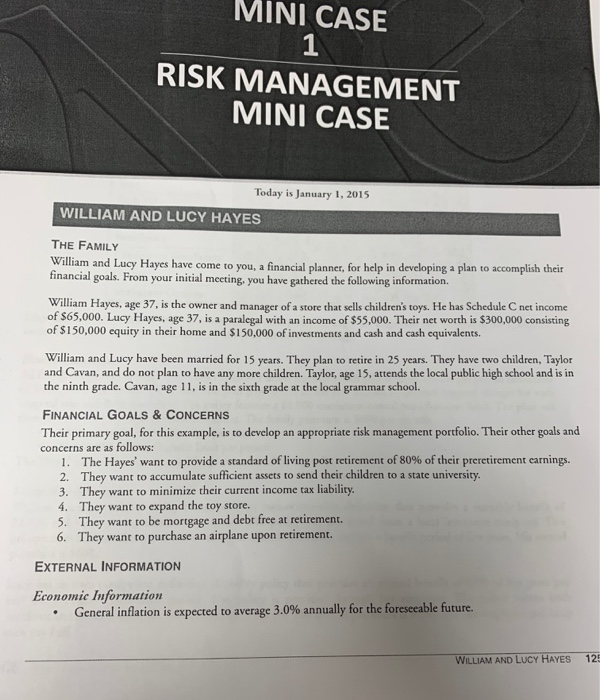

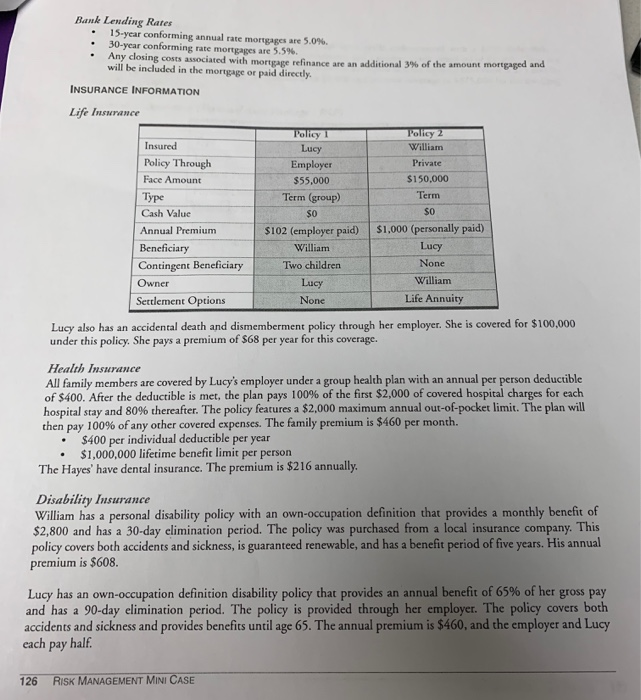

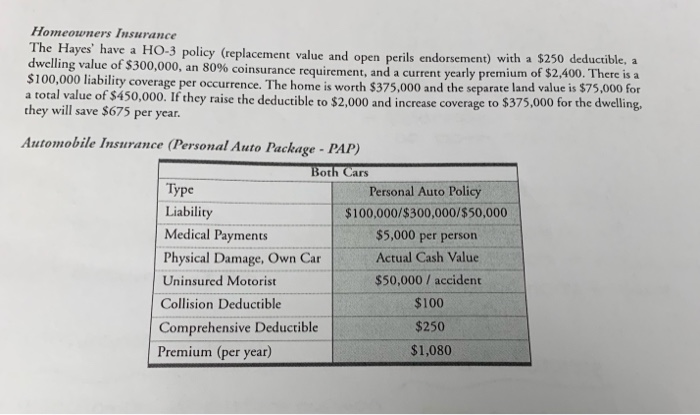

MINI CASE 1 RISK MANAGEMENT MINI CASE Today is January 1, 2015 WILLIAM AND LUCY HAYES THE FAMILY William and Lucy Hayes have come to you, a financial planner, for help in developing a plan to accomplish their financial goals. From your initial meeting, you have gathered the following information William Hayes, age 37, is the owner and manager of a store that sells children's toys. He has Schedule C net income of $65,000. Lucy Hayes, age 37, is a paralegal with an income of $55,000. Their net worth is $300,000 consisting of $150,000 equity in their home and $150,000 of investments and cash and cash equivalents. William and Lucy have been married for 15 years. They plan to retire in 25 years. They have two children, Taylor and Cavan, and do not plan to have any more children. Taylor, age 15, attends the local public high school and is in the ninth grade. Cavan, age 11, is in the sixth grade at the local grammar school. FINANCIAL GOALS & CONCERNS Their primary goal, for this example, is to develop an appropriate risk management portfolio. Their other goals and concerns are as follows: 1. The Hayes' want to provide a standard of living post retirement of 80% of their preretirement carnings. 2. They want to accumulate sufficient assets to send their children to a state university 3. They want to minimize their current income tax liability. 4. They want to expand the toy store. 5. They want to be mortgage and debt free at retirement. 6. They want to purchase an airplane upon retirement. EXTERNAL INFORMATION Economic Information General inflation is expected to average 3.0% annually for the foreseeable future. WILLIAM AND LUCY HAYES 125 Bank Lending Rates 15 year conforming annual rate mortgages are 5.0%. 30-year conforming rate mortgages are 5.5 Any closing costs associated with mortgage refinance are an additional will be included in the mortgage or paid directly. of the amount mortgaged and INSURANCE INFORMATION Life Insurance Policy 1 Insured Lucy Policy 2 William Private $150,000 "Term Policy Through Face Amount Type Cash Value Annual Premium Beneficiary Contingent Beneficiary Owner Settlement Options Employer $55,000 Term (group) $0 $102 (employer paid) William Two children Lucy None $1.000 (personally paid) Lucy None William Life Annuity Lucy also has an accidental death and dismemberment policy through her employer. She is covered for $100,000 under this policy. She pays a premium of $68 per year for this coverage. Health Insurance All family members are covered by Lucy's employer under a group health plan with an annual per person deductible of $400. After the deductible is met, the plan pays 100% of the first $2,000 of covered hospital charges for each hospital stay and 80% thereafter. The policy features a $2.000 maximum annual out-of-pocket limit. The plan will then pay 100% of any other covered expenses. The family premium is $460 per month. $400 per individual deductible per year $1,000,000 lifetime benefic limit per person The Hayes' have dental insurance. The premium is $216 annually. Disability Insurance William has a personal disability policy with an own-occupation definition that provides a monthly benefit of $2,800 and has a 30-day elimination period. The policy was purchased from a local insurance company. This policy covers both accidents and sickness, is guaranteed renewable, and has a benefit period of five years. His annual premium is $608. Lucy has an own-occupation definition disability policy that provides an annual benefit of 65% of her gross pay and has a 90-day elimination period. The policy is provided through her employer. The policy covers both accidents and sickness and provides benefits until age 65. The annual premium is $460, and the employer and Lucy cach pay half. 126 RISK MANAGEMENT MINI CASE Homeowners Insurance The Hayes' have a HO-3 policy (replacement value and open perils endorsement) with a $250 deductible, a dwelling value of $300,000, an 80% coinsurance requirement, and a current yearly premium of $2,400. There is a $100,000 liability coverage per occurrence. The home is worth $375,000 and the separate land value is $75,000 for a total value of $450,000. If they raise the deductible to $2.000 and increase coverage to $375,000 for the dwelling, they will save $675 per year. Automobile Insurance (Personal Auto Package - PAP) Both Cars Type Personal Auto Policy Liability $100,000/$300,000/$50,000 Medical Payments $5,000 per person Physical Damage, Own Car Actual Cash Value Uninsured Motorist $50,000 / accident Collision Deductible $100 Comprehensive Deductible $250 Premium (per year) $1,080 MINI CASE 1 RISK MANAGEMENT MINI CASE Today is January 1, 2015 WILLIAM AND LUCY HAYES THE FAMILY William and Lucy Hayes have come to you, a financial planner, for help in developing a plan to accomplish their financial goals. From your initial meeting, you have gathered the following information William Hayes, age 37, is the owner and manager of a store that sells children's toys. He has Schedule C net income of $65,000. Lucy Hayes, age 37, is a paralegal with an income of $55,000. Their net worth is $300,000 consisting of $150,000 equity in their home and $150,000 of investments and cash and cash equivalents. William and Lucy have been married for 15 years. They plan to retire in 25 years. They have two children, Taylor and Cavan, and do not plan to have any more children. Taylor, age 15, attends the local public high school and is in the ninth grade. Cavan, age 11, is in the sixth grade at the local grammar school. FINANCIAL GOALS & CONCERNS Their primary goal, for this example, is to develop an appropriate risk management portfolio. Their other goals and concerns are as follows: 1. The Hayes' want to provide a standard of living post retirement of 80% of their preretirement carnings. 2. They want to accumulate sufficient assets to send their children to a state university 3. They want to minimize their current income tax liability. 4. They want to expand the toy store. 5. They want to be mortgage and debt free at retirement. 6. They want to purchase an airplane upon retirement. EXTERNAL INFORMATION Economic Information General inflation is expected to average 3.0% annually for the foreseeable future. WILLIAM AND LUCY HAYES 125 Bank Lending Rates 15 year conforming annual rate mortgages are 5.0%. 30-year conforming rate mortgages are 5.5 Any closing costs associated with mortgage refinance are an additional will be included in the mortgage or paid directly. of the amount mortgaged and INSURANCE INFORMATION Life Insurance Policy 1 Insured Lucy Policy 2 William Private $150,000 "Term Policy Through Face Amount Type Cash Value Annual Premium Beneficiary Contingent Beneficiary Owner Settlement Options Employer $55,000 Term (group) $0 $102 (employer paid) William Two children Lucy None $1.000 (personally paid) Lucy None William Life Annuity Lucy also has an accidental death and dismemberment policy through her employer. She is covered for $100,000 under this policy. She pays a premium of $68 per year for this coverage. Health Insurance All family members are covered by Lucy's employer under a group health plan with an annual per person deductible of $400. After the deductible is met, the plan pays 100% of the first $2,000 of covered hospital charges for each hospital stay and 80% thereafter. The policy features a $2.000 maximum annual out-of-pocket limit. The plan will then pay 100% of any other covered expenses. The family premium is $460 per month. $400 per individual deductible per year $1,000,000 lifetime benefic limit per person The Hayes' have dental insurance. The premium is $216 annually. Disability Insurance William has a personal disability policy with an own-occupation definition that provides a monthly benefit of $2,800 and has a 30-day elimination period. The policy was purchased from a local insurance company. This policy covers both accidents and sickness, is guaranteed renewable, and has a benefit period of five years. His annual premium is $608. Lucy has an own-occupation definition disability policy that provides an annual benefit of 65% of her gross pay and has a 90-day elimination period. The policy is provided through her employer. The policy covers both accidents and sickness and provides benefits until age 65. The annual premium is $460, and the employer and Lucy cach pay half. 126 RISK MANAGEMENT MINI CASE Homeowners Insurance The Hayes' have a HO-3 policy (replacement value and open perils endorsement) with a $250 deductible, a dwelling value of $300,000, an 80% coinsurance requirement, and a current yearly premium of $2,400. There is a $100,000 liability coverage per occurrence. The home is worth $375,000 and the separate land value is $75,000 for a total value of $450,000. If they raise the deductible to $2.000 and increase coverage to $375,000 for the dwelling, they will save $675 per year. Automobile Insurance (Personal Auto Package - PAP) Both Cars Type Personal Auto Policy Liability $100,000/$300,000/$50,000 Medical Payments $5,000 per person Physical Damage, Own Car Actual Cash Value Uninsured Motorist $50,000 / accident Collision Deductible $100 Comprehensive Deductible $250 Premium (per year) $1,080 - Provide correct calculations of the current position

- Provide applicable recommendations and a hood explanation

Thanks!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Corporate Finance Law

Authors: Eilis Ferran, Look Chan Ho

2nd Edition

0199671354, 978-0199671359