Answered step by step

Verified Expert Solution

Question

1 Approved Answer

answers for question 3 and 6 answers for number 3 and number 6 Your firm, ACTG 307 & Associates, is engaged to audit the financial

answers for question 3 and 6

answers for number 3 and number 6

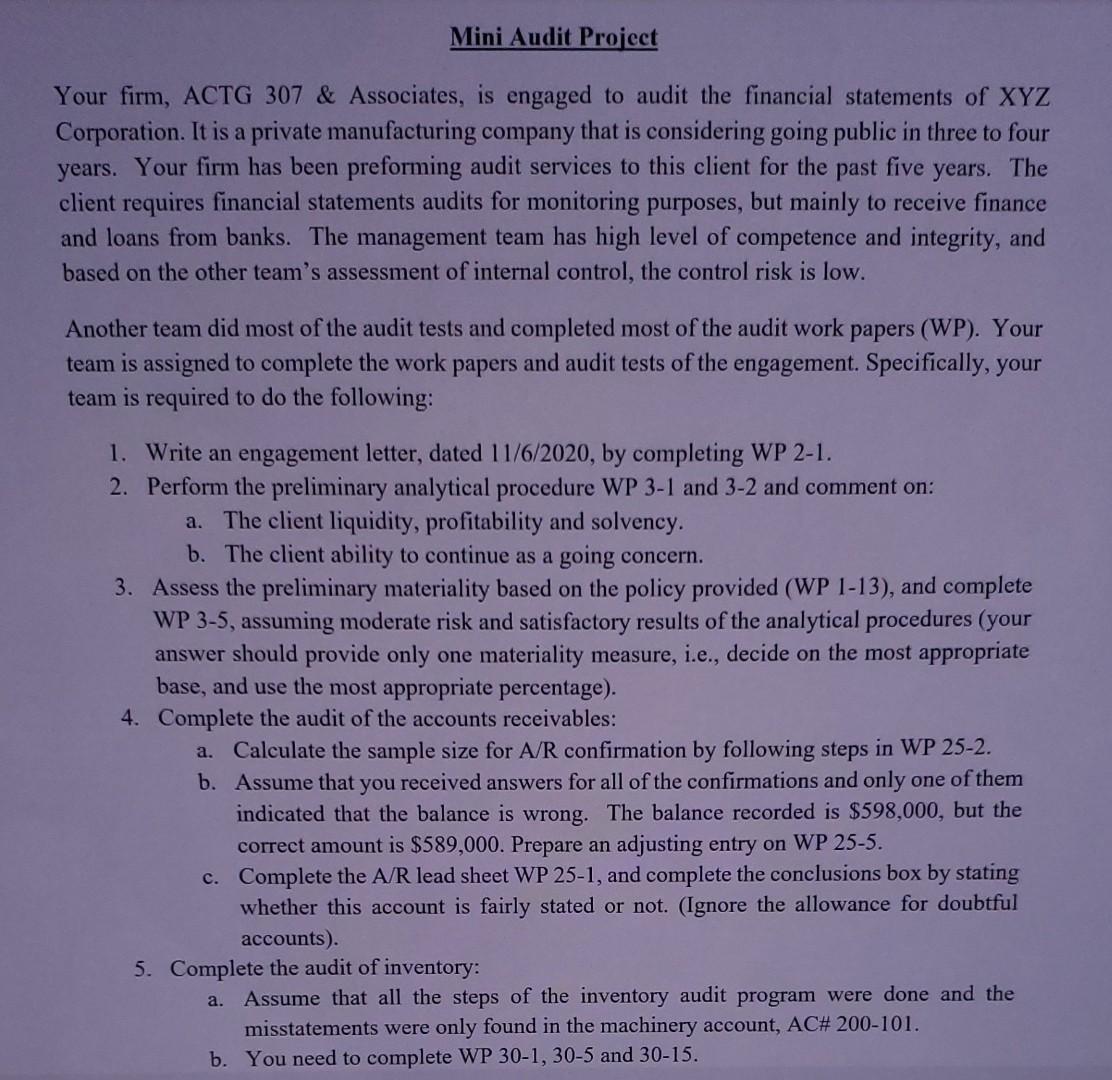

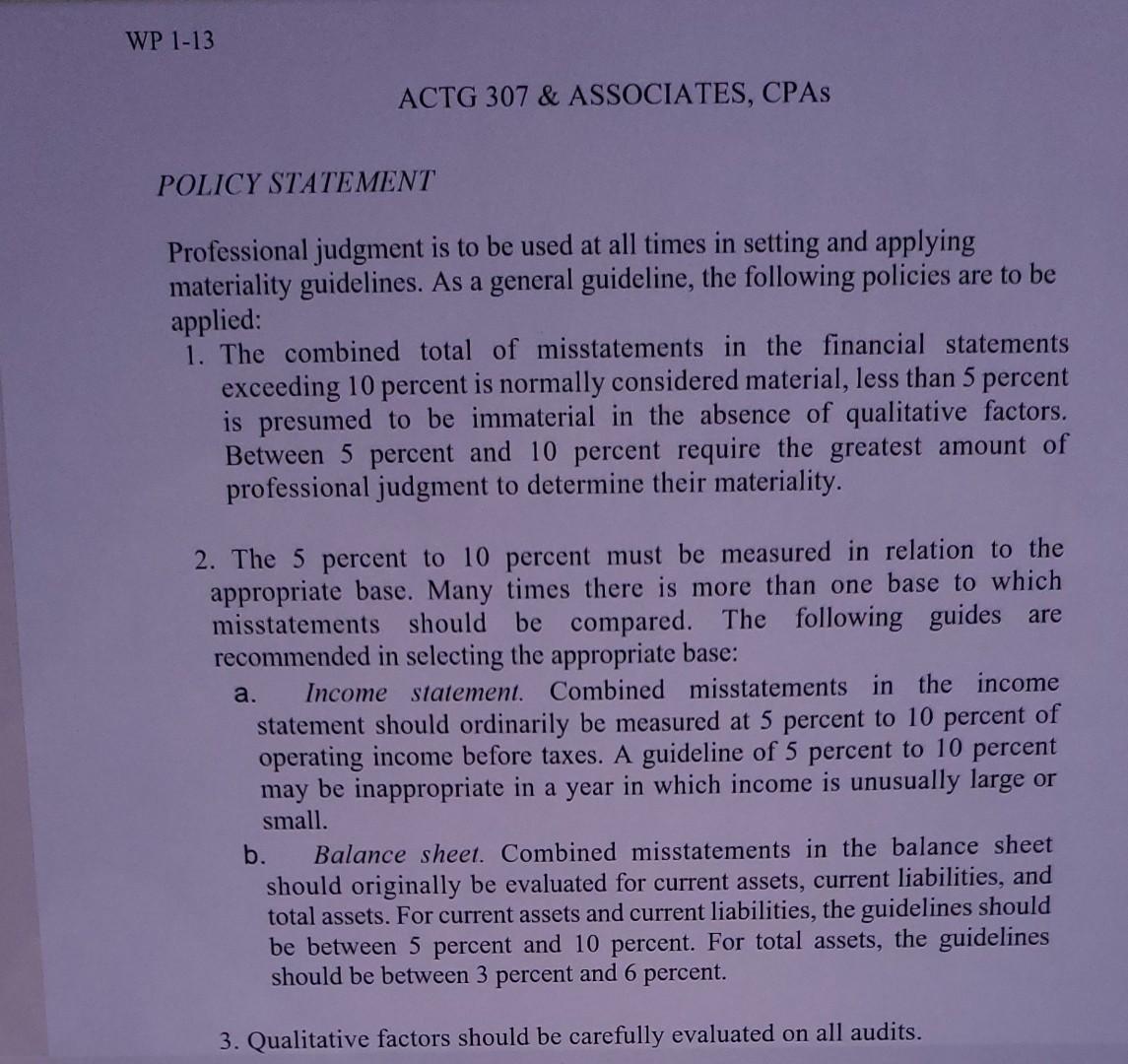

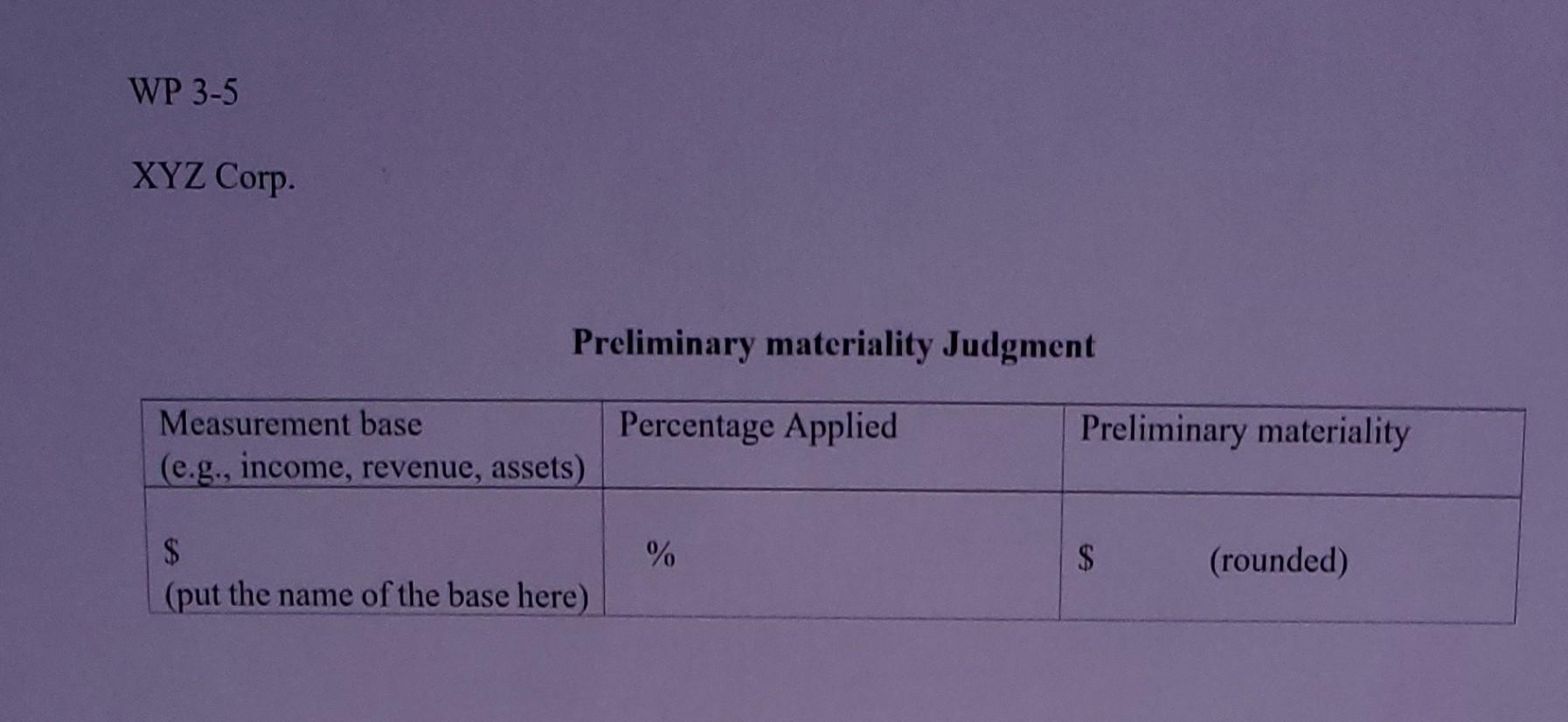

Your firm, ACTG 307 \& Associates, is engaged to audit the financial statements of XYZ Corporation. It is a private manufacturing company that is considering going public in three to four years. Your firm has been preforming audit services to this client for the past five years. The client requires financial statements audits for monitoring purposes, but mainly to receive finance and loans from banks. The management team has high level of competence and integrity, and based on the other team's assessment of internal control, the control risk is low. Another team did most of the audit tests and completed most of the audit work papers (WP). Your team is assigned to complete the work papers and audit tests of the engagement. Specifically, your team is required to do the following: 1. Write an engagement letter, dated 11/6/2020, by completing WP 21. 2. Perform the preliminary analytical procedure WP 3-1 and 3-2 and comment on: a. The client liquidity, profitability and solvency. b. The client ability to continue as a going concern. 3. Assess the preliminary materiality based on the policy provided (WP 1-13), and complete WP 3-5, assuming moderate risk and satisfactory results of the analytical procedures (your answer should provide only one materiality measure, i.e., decide on the most appropriate base, and use the most appropriate percentage). 4. Complete the audit of the accounts receivables: a. Calculate the sample size for A/R confirmation by following steps in WP 25-2. b. Assume that you received answers for all of the confirmations and only one of them indicated that the balance is wrong. The balance recorded is $598,000, but the correct amount is $589,000. Prepare an adjusting entry on WP 255. c. Complete the A/R lead sheet WP 251, and complete the conclusions box by stating whether this account is fairly stated or not. (Ignore the allowance for doubtful accounts). 5. Complete the audit of inventory: a. Assume that all the steps of the inventory audit program were done and the misstatements were only found in the machinery account, AC\# 200-101. b. You need to complete WP 301,305 and 3015. 5. Complete the audit of inventory: a. Assume that all the steps of the inventory audit program were done and the misstatements were only found in the machinery account, AC\# 200-101. b. You need to complete WP 30-1, 30-5 and 30-15. 6. Assuming that all other tests came to be satisfactory, prepare an audit report, with the appropriate opinion (dated 2/21/2021). WP 1-13 ACTG 307 \& ASSOCIATES, CPAs POLICY STATEMENT Professional judgment is to be used at all times in setting and applying materiality guidelines. As a general guideline, the following policies are to be applied: 1. The combined total of misstatements in the financial statements exceeding 10 percent is normally considered material, less than 5 percent is presumed to be immaterial in the absence of qualitative factors. Between 5 percent and 10 percent require the greatest amount of professional judgment to determine their materiality. 2. The 5 percent to 10 percent must be measured in relation to the appropriate base. Many times there is more than one base to which misstatements should be compared. The following guides are recommended in selecting the appropriate base: a. Income statement. Combined misstatements in the income statement should ordinarily be measured at 5 percent to 10 percent of operating income before taxes. A guideline of 5 percent to 10 percent may be inappropriate in a year in which income is unusually large or small. b. Balance sheet. Combined misstatements in the balance sheet should originally be evaluated for current assets, current liabilities, and total assets. For current assets and current liabilities, the guidelines should be between 5 percent and 10 percent. For total assets, the guidelines should be between 3 percent and 6 percent. 3. Qualitative factors should be carefully evaluated on all audits. Preliminary materiality Judgment Your firm, ACTG 307 \& Associates, is engaged to audit the financial statements of XYZ Corporation. It is a private manufacturing company that is considering going public in three to four years. Your firm has been preforming audit services to this client for the past five years. The client requires financial statements audits for monitoring purposes, but mainly to receive finance and loans from banks. The management team has high level of competence and integrity, and based on the other team's assessment of internal control, the control risk is low. Another team did most of the audit tests and completed most of the audit work papers (WP). Your team is assigned to complete the work papers and audit tests of the engagement. Specifically, your team is required to do the following: 1. Write an engagement letter, dated 11/6/2020, by completing WP 21. 2. Perform the preliminary analytical procedure WP 3-1 and 3-2 and comment on: a. The client liquidity, profitability and solvency. b. The client ability to continue as a going concern. 3. Assess the preliminary materiality based on the policy provided (WP 1-13), and complete WP 3-5, assuming moderate risk and satisfactory results of the analytical procedures (your answer should provide only one materiality measure, i.e., decide on the most appropriate base, and use the most appropriate percentage). 4. Complete the audit of the accounts receivables: a. Calculate the sample size for A/R confirmation by following steps in WP 25-2. b. Assume that you received answers for all of the confirmations and only one of them indicated that the balance is wrong. The balance recorded is $598,000, but the correct amount is $589,000. Prepare an adjusting entry on WP 255. c. Complete the A/R lead sheet WP 251, and complete the conclusions box by stating whether this account is fairly stated or not. (Ignore the allowance for doubtful accounts). 5. Complete the audit of inventory: a. Assume that all the steps of the inventory audit program were done and the misstatements were only found in the machinery account, AC\# 200-101. b. You need to complete WP 301,305 and 3015. 5. Complete the audit of inventory: a. Assume that all the steps of the inventory audit program were done and the misstatements were only found in the machinery account, AC\# 200-101. b. You need to complete WP 30-1, 30-5 and 30-15. 6. Assuming that all other tests came to be satisfactory, prepare an audit report, with the appropriate opinion (dated 2/21/2021). WP 1-13 ACTG 307 \& ASSOCIATES, CPAs POLICY STATEMENT Professional judgment is to be used at all times in setting and applying materiality guidelines. As a general guideline, the following policies are to be applied: 1. The combined total of misstatements in the financial statements exceeding 10 percent is normally considered material, less than 5 percent is presumed to be immaterial in the absence of qualitative factors. Between 5 percent and 10 percent require the greatest amount of professional judgment to determine their materiality. 2. The 5 percent to 10 percent must be measured in relation to the appropriate base. Many times there is more than one base to which misstatements should be compared. The following guides are recommended in selecting the appropriate base: a. Income statement. Combined misstatements in the income statement should ordinarily be measured at 5 percent to 10 percent of operating income before taxes. A guideline of 5 percent to 10 percent may be inappropriate in a year in which income is unusually large or small. b. Balance sheet. Combined misstatements in the balance sheet should originally be evaluated for current assets, current liabilities, and total assets. For current assets and current liabilities, the guidelines should be between 5 percent and 10 percent. For total assets, the guidelines should be between 3 percent and 6 percent. 3. Qualitative factors should be carefully evaluated on all audits. Preliminary materiality JudgmentStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started