Any T2 tax software package can be used.

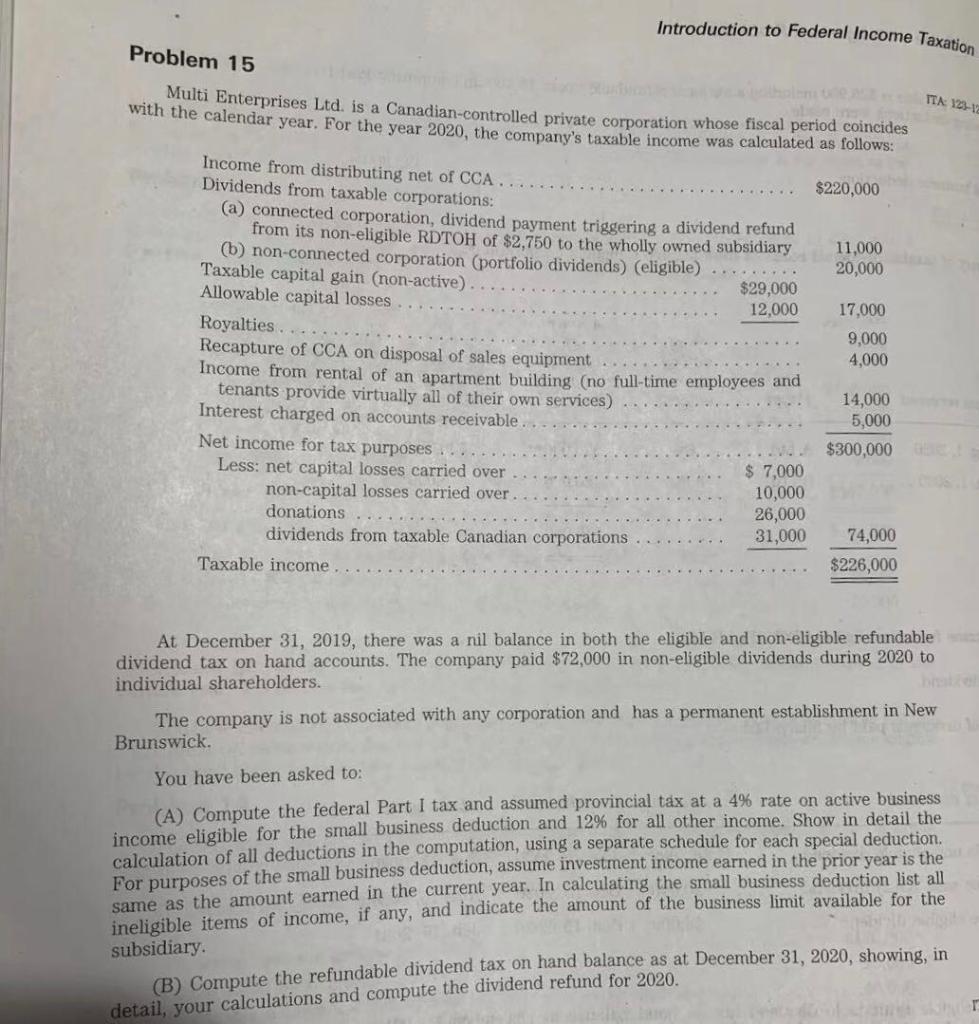

Introduction to Federal Income Taxation TTA: 123-12 Problem 15 Multi Enterprises Ltd. is a Canadian-controlled private corporation whose fiscal period coincides with the calendar year. For the year 2020, the company's taxable income was calculated as follows: Income from distributing net of CCA. Dividends from taxable corporations: $220,000 (a) connected corporation, dividend payment triggering a dividend refund from its non-eligible RDTOH of $2,750 to the wholly owned subsidiary 11,000 (b) non-connected corporation (portfolio dividends) (eligible) 20,000 Taxable capital gain (non-active) $29,000 Allowable capital losses 12,000 17,000 Royalties 9,000 Recapture of CCA on disposal of sales equipment 4,000 Income from rental of an apartment building (no full-time employees and tenants provide virtually all of their own services) 14,000 Interest charged on accounts receivable 5,000 Net income for tax purposes $300,000 Less: net capital losses carried over $ 7,000 non-capital losses carried over 10,000 donations 26,000 dividends from taxable Canadian corporations 31,000 74,000 $226,000 Taxable income At December 31, 2019, there was a nil balance in both the eligible and non-eligible refundable dividend tax on hand accounts. The company paid $72,000 in non-eligible dividends during 2020 to individual shareholders. The company is not associated with any corporation and has a permanent establishment in New Brunswick. You have been asked to: (A) Compute the federal Part I tax and assumed provincial tax at a 4% rate on active business income eligible for the small business deduction and 12% for all other income. Show in detail the calculation of all deductions in the computation, using a separate schedule for each special deduction. For purposes of the small business deduction, assume investment income earned in the prior year is the same as the amount earned in the current year. In calculating the small business deduction list all ineligible items of income, if any, and indicate the amount of the business limit available for the subsidiary. (B) Compute the refundable dividend tax on hand balance as at December 31, 2020, showing, in detail, your calculations and compute the dividend refund for 2020. Introduction to Federal Income Taxation TTA: 123-12 Problem 15 Multi Enterprises Ltd. is a Canadian-controlled private corporation whose fiscal period coincides with the calendar year. For the year 2020, the company's taxable income was calculated as follows: Income from distributing net of CCA. Dividends from taxable corporations: $220,000 (a) connected corporation, dividend payment triggering a dividend refund from its non-eligible RDTOH of $2,750 to the wholly owned subsidiary 11,000 (b) non-connected corporation (portfolio dividends) (eligible) 20,000 Taxable capital gain (non-active) $29,000 Allowable capital losses 12,000 17,000 Royalties 9,000 Recapture of CCA on disposal of sales equipment 4,000 Income from rental of an apartment building (no full-time employees and tenants provide virtually all of their own services) 14,000 Interest charged on accounts receivable 5,000 Net income for tax purposes $300,000 Less: net capital losses carried over $ 7,000 non-capital losses carried over 10,000 donations 26,000 dividends from taxable Canadian corporations 31,000 74,000 $226,000 Taxable income At December 31, 2019, there was a nil balance in both the eligible and non-eligible refundable dividend tax on hand accounts. The company paid $72,000 in non-eligible dividends during 2020 to individual shareholders. The company is not associated with any corporation and has a permanent establishment in New Brunswick. You have been asked to: (A) Compute the federal Part I tax and assumed provincial tax at a 4% rate on active business income eligible for the small business deduction and 12% for all other income. Show in detail the calculation of all deductions in the computation, using a separate schedule for each special deduction. For purposes of the small business deduction, assume investment income earned in the prior year is the same as the amount earned in the current year. In calculating the small business deduction list all ineligible items of income, if any, and indicate the amount of the business limit available for the subsidiary. (B) Compute the refundable dividend tax on hand balance as at December 31, 2020, showing, in detail, your calculations and compute the dividend refund for 2020