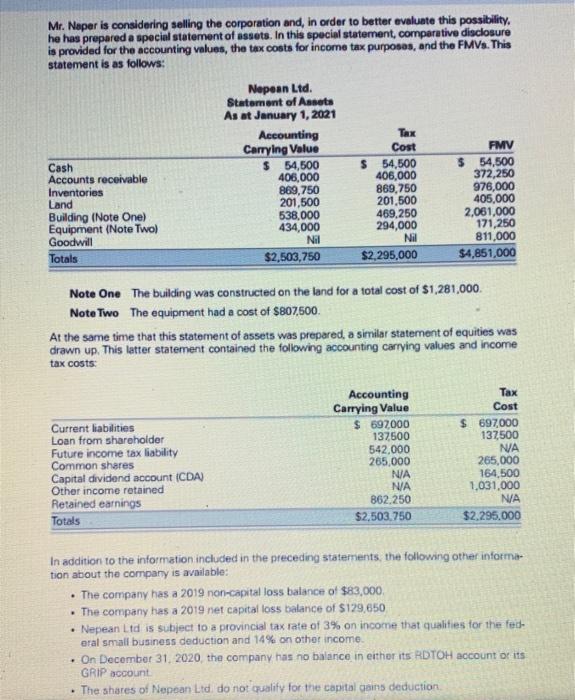

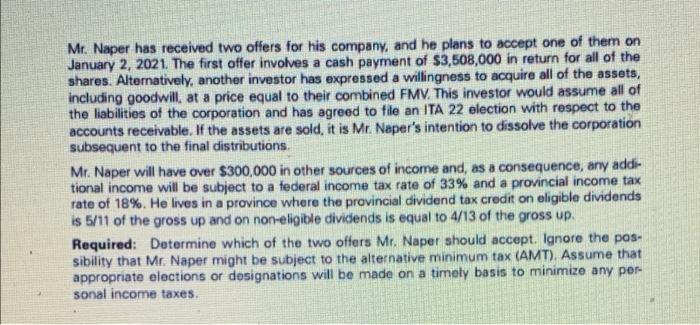

AP 17-9 (Sale of Assets vs. Shares) Mr Nathan Naper is the president and only shareholder of Nepean Ltd, a CCPC The company's taxation year end is December 31. Mr. Naper incorporated the company 15 years ago. The ACB and the PUC of the shares are both $265,000. No other shares have ever been issued Tax Mr. Naper is considering selling the corporation and, in order to better evaluate this possibility. he has prepared a special statement of assets. In this special statement, comparative disclosure is provided for the accounting values, the tax costs for income tax purposes, and the FMVs. This statement is as follows: Nepean Ltd. Statement of Assets As at January 1, 2021 Accounting Carrying Value Cost FMV Cash $ 54,500 $ 54,500 $ 54,500 Accounts receivable 406,000 406,000 372,250 Inventories 869,750 869,750 976,000 Land 201,500 201,500 405,000 Building (Note One) 538,000 469.250 2,061,000 Equipment (Note Two) 434,000 294,000 171,250 Goodwill Nil Nil 811,000 Totals $2,503,750 $2,295,000 $4,851,000 Note One The building was constructed on the land for a total cost of $1,281,000 Note Two The equipment had a cost of $807,500 At the same time that this statement of assets was prepared a similar statement of equities was drawn up. This letter statement contained the following accounting carrying values and income tax costs: Current liabilities Loan from shareholder Future income tax liability Common shares Capital dividend account (CDA) Other income retained Retained earnings Totals Accounting Carrying Value $ 597000 137.500 542,000 265,000 NIA N/A 862.250 $2,503.750 Tax Cost $ 697,000 137500 NA 265,000 164,500 1,031,000 NA $2.295.000 In addition to the information included in the preceding statements, the following other informa tion about the company is available: The company has a 2019 non-capital loss balance of $83,000 The company has a 2019 net capital loss balance of $129,650 Nepean Ltd is subject to a provincial tax rate of 3% on income that qualities for the fed. eral small business deduction and 14% on other income . On December 31, 2020 the company has no balance in either its RDTOH account or its GRIP account The shares of Nepean Ltd do not qualify for the capital gains deduction . Mr. Naper has received two offers for his company, and he plans to accept one of them on January 2, 2021. The first offer involves a cash payment of $3,508,000 in return for all of the shares. Alternatively, another investor has expressed a willingness to acquire all of the assets, including goodwill, at a price equal to their combined FMV. This investor would assume all of the liabilities of the corporation and has agreed to file an ITA 22 election with respect to the accounts receivable. If the assets are sold, it is Mr. Naper's intention to dissolve the corporation subsequent to the final distributions Mr. Naper will have over $300,000 in other sources of income and, as a consequence, any addi- tional income will be subject to a federal income tax rate of 33% and a provincial income tax rate of 18%. He lives in a province where the provincial dividend tax credit on eligible dividends is 5/11 of the gross up and on non-eligible dividends is equal to 4/13 of the gross up Required: Determine which of the two offers Mr. Naper should accept. Ignore the pos- sibility that Mr. Naper might be subject to the alternative minimum tax (AMT). Assume that appropriate elections or designations will be made on a timely basis to minimize any per sonal income taxes. AP 17-9 (Sale of Assets vs. Shares) Mr Nathan Naper is the president and only shareholder of Nepean Ltd, a CCPC The company's taxation year end is December 31. Mr. Naper incorporated the company 15 years ago. The ACB and the PUC of the shares are both $265,000. No other shares have ever been issued Tax Mr. Naper is considering selling the corporation and, in order to better evaluate this possibility. he has prepared a special statement of assets. In this special statement, comparative disclosure is provided for the accounting values, the tax costs for income tax purposes, and the FMVs. This statement is as follows: Nepean Ltd. Statement of Assets As at January 1, 2021 Accounting Carrying Value Cost FMV Cash $ 54,500 $ 54,500 $ 54,500 Accounts receivable 406,000 406,000 372,250 Inventories 869,750 869,750 976,000 Land 201,500 201,500 405,000 Building (Note One) 538,000 469.250 2,061,000 Equipment (Note Two) 434,000 294,000 171,250 Goodwill Nil Nil 811,000 Totals $2,503,750 $2,295,000 $4,851,000 Note One The building was constructed on the land for a total cost of $1,281,000 Note Two The equipment had a cost of $807,500 At the same time that this statement of assets was prepared a similar statement of equities was drawn up. This letter statement contained the following accounting carrying values and income tax costs: Current liabilities Loan from shareholder Future income tax liability Common shares Capital dividend account (CDA) Other income retained Retained earnings Totals Accounting Carrying Value $ 597000 137.500 542,000 265,000 NIA N/A 862.250 $2,503.750 Tax Cost $ 697,000 137500 NA 265,000 164,500 1,031,000 NA $2.295.000 In addition to the information included in the preceding statements, the following other informa tion about the company is available: The company has a 2019 non-capital loss balance of $83,000 The company has a 2019 net capital loss balance of $129,650 Nepean Ltd is subject to a provincial tax rate of 3% on income that qualities for the fed. eral small business deduction and 14% on other income . On December 31, 2020 the company has no balance in either its RDTOH account or its GRIP account The shares of Nepean Ltd do not qualify for the capital gains deduction . Mr. Naper has received two offers for his company, and he plans to accept one of them on January 2, 2021. The first offer involves a cash payment of $3,508,000 in return for all of the shares. Alternatively, another investor has expressed a willingness to acquire all of the assets, including goodwill, at a price equal to their combined FMV. This investor would assume all of the liabilities of the corporation and has agreed to file an ITA 22 election with respect to the accounts receivable. If the assets are sold, it is Mr. Naper's intention to dissolve the corporation subsequent to the final distributions Mr. Naper will have over $300,000 in other sources of income and, as a consequence, any addi- tional income will be subject to a federal income tax rate of 33% and a provincial income tax rate of 18%. He lives in a province where the provincial dividend tax credit on eligible dividends is 5/11 of the gross up and on non-eligible dividends is equal to 4/13 of the gross up Required: Determine which of the two offers Mr. Naper should accept. Ignore the pos- sibility that Mr. Naper might be subject to the alternative minimum tax (AMT). Assume that appropriate elections or designations will be made on a timely basis to minimize any per sonal income taxes