Question

Appendix: Normal and Abnormal Spoilage in Process Costing, Changes in Output Measures, Multiple Departments Grayson Company produces an industrial chemical used for cleaning and lubricating

Appendix: Normal and Abnormal Spoilage in Process Costing, Changes in Output Measures, Multiple Departments

Grayson Company produces an industrial chemical used for cleaning and lubricating machinery. In the Mixing Department, liquid and dry chemicals are blended to form slurry. Output is measured in gallons. In the Baking Department, the slurry is subjected to high heat, and the residue appears in irregular lumps. Output is measured in pounds. In the Grinding Department, the irregular lumps are ground into a powder, and this powder is placed in 50-pound bags. Output is measured in bags produced. In April, the company reported the following data:

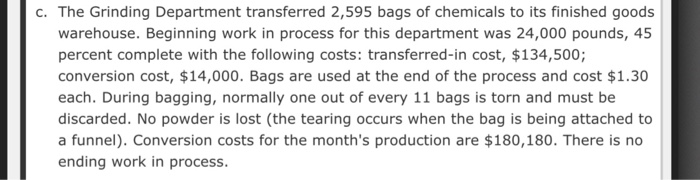

- The Mixing Department transferred 51,900 gallons to the Baking Department, costing $207,600. Each gallon of slurry weighs two pounds.

- The Baking Department transferred 103,800 pounds (irregular lumps) to the Grinding Department. At the beginning of the month, there were 6,000 gallons of slurry in process, 25 percent complete, costing $34,800 (transferred-in cost of $24,000 plus conversion cost of $10,800). No additional direct materials are added in the Baking Department. At the end of April, there was no ending work in process. Conversion costs for the month totaled $213,600. Normal loss during baking is 5 percent of good output. All transferred-in materials are lost, but since loss occurs uniformly throughout the process, only 50 percent of the conversion units are assumed to be lost.

- The Grinding Department transferred 2,595 bags of chemicals to its finished goods warehouse. Beginning work in process for this department was 24,000 pounds, 45 percent complete with the following costs: transferred-in cost, $134,500; conversion cost, $14,000. Bags are used at the end of the process and cost $1.30 each. During bagging, normally one out of every 11 bags is torn and must be discarded. No powder is lost (the tearing occurs when the bag is being attached to a funnel). Conversion costs for the month's production are $180,180. There is no ending work in process.

Required:

1. Using FIFO, calculate the cost per bag of chemicals transferred to the finished goods warehouse. Round per-unit costs to the nearest cent. Round other solutions to the nearest unit or dollar as needed.

Baking Department (to obtain the cost of goods transferred out):

| Units to account for: | |

| Beginning work in process | fill in the blank 61452b022026f91_1 |

| Units started | fill in the blank 61452b022026f91_2 |

| Total units to account for | fill in the blank 61452b022026f91_3 |

| Units accounted for: | |

| Units transferred out | fill in the blank 61452b022026f91_4 |

| Normal spoilage | fill in the blank 61452b022026f91_5 |

| Abnormal spoilage | fill in the blank 61452b022026f91_6 |

| Total units accounted for | fill in the blank 61452b022026f91_7 |

| Equivalent Units | ||

| Conversion Costs | Transferred In | |

| Total equivalent units | fill in the blank 61452b022026f91_8 | fill in the blank 61452b022026f91_9 |

| Total unit cost | $fill in the blank 61452b022026f91_10 | |

| Cost of units transferred out: | ||

| Started and competed | $fill in the blank 61452b022026f91_11 | |

| Prior period costs | $fill in the blank 61452b022026f91_12 | |

| Costs to finish | fill in the blank 61452b022026f91_13 | fill in the blank 61452b022026f91_14 |

| Normal spoilage | fill in the blank 61452b022026f91_15 | |

| Total | $fill in the blank 61452b022026f91_16 | |

Grinding Department:

| Total units accounted for | fill in the blank 61452b022026f91_17 |

Note: (For direct materials: 11 bags are used to get 10 good bags).

| Unit cost of units started and completed: | ||||

| Direct Materials | Conversion Costs | Transferred In | Total | |

| Costs added | $fill in the blank 61452b022026f91_18 | $fill in the blank 61452b022026f91_19 | $fill in the blank 61452b022026f91_20 | |

| Total equivalent units | fill in the blank 61452b022026f91_21 | fill in the blank 61452b022026f91_22 | fill in the blank 61452b022026f91_23 | |

| Cost per equivalent unit | $fill in the blank 61452b022026f91_24 | $fill in the blank 61452b022026f91_25 | $fill in the blank 61452b022026f91_26 | $fill in the blank 61452b022026f91_27 |

| Unit cost of units from beginning work in process: | ||

| Prior period costs | $fill in the blank 61452b022026f91_28 | |

| Costs to finish: | ||

| Direct materials | fill in the blank 61452b022026f91_29 | |

| Conversion costs | fill in the blank 61452b022026f91_30 | |

| Total | $fill in the blank 61452b022026f91_31 | |

| Unit cost | $fill in the blank 61452b022026f91_32 | per unit |

2. Prepare the journal entry needed to remove spoilage from the Baking and Grinding departments. Round your answers to the nearest dollar if rounding is required.

| fill in the blank 2b114ffc5f90fbe_2 | |||

| fill in the blank 2b114ffc5f90fbe_4 |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Carl s. warren, James m. reeve, Philip e. fess

21st Edition

978-0324400205, 324225016, 324188005, 324400209, 9780324225013, 978-0324188004