Answered step by step

Verified Expert Solution

Question

1 Approved Answer

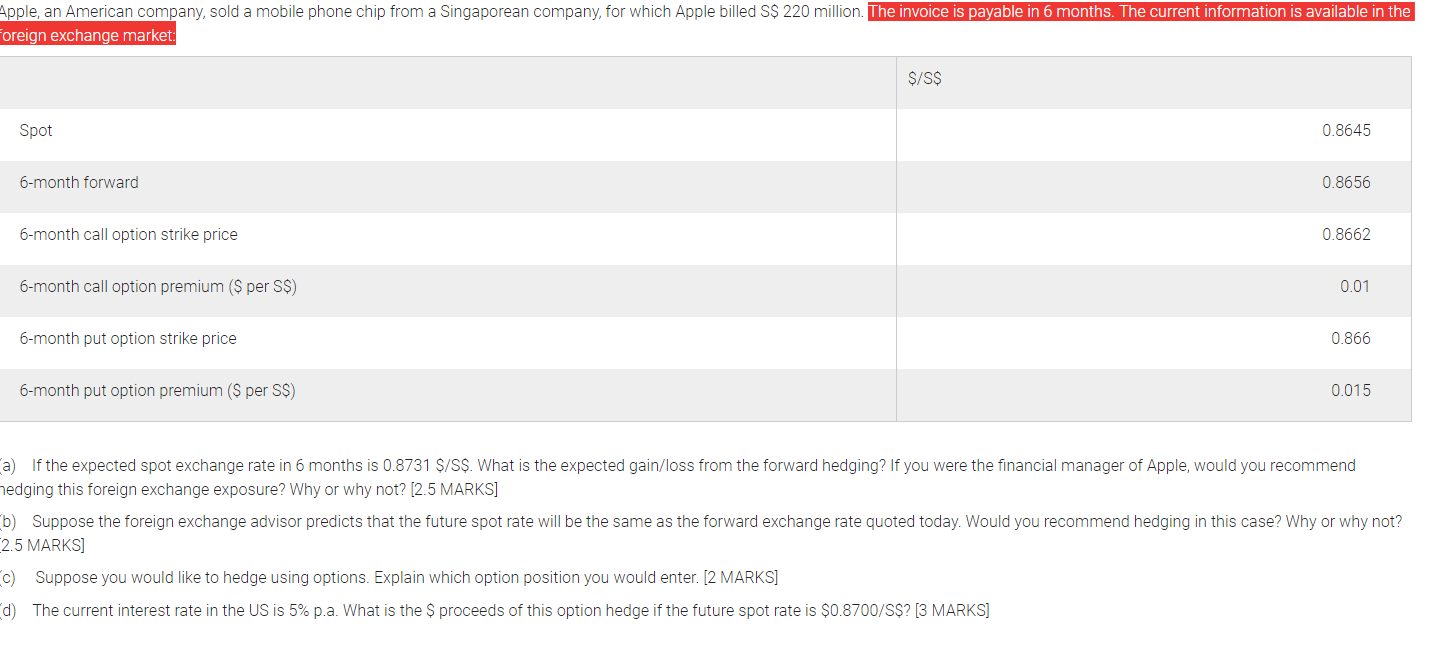

Apple, an American company, sold a mobile phone chip from a Singaporean company, for which Apple billed S$ 220 million. The invoice is payable in

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Evidence Based Audit In General Practice

Authors: Richard Baker, Robin C. Fraser MD FRCGP, Mayur Lakhani MRCP MRCGP DCH

1st Edition

075063104X, 978-0750631044