Answered step by step

Verified Expert Solution

Question

1 Approved Answer

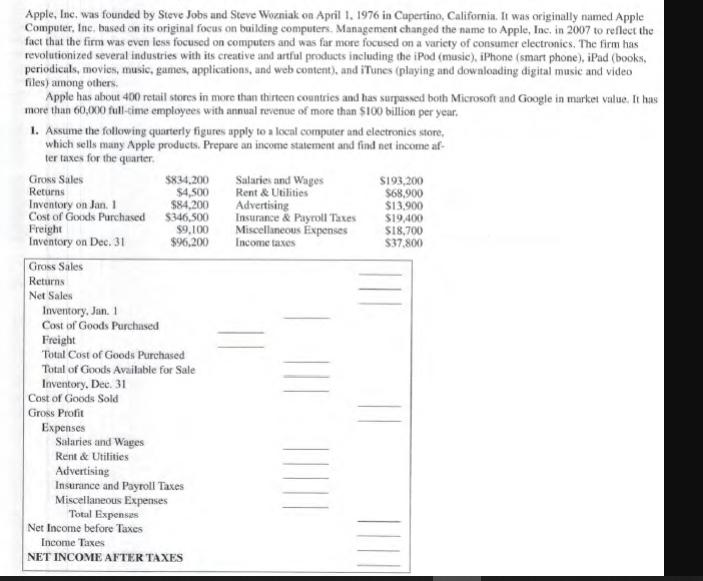

Apple, Inc. was founded by Steve Jobs and Steve Wozniak on April 1, 1976 in Cupertino, California. It was originally named Apple Computer, Inc.

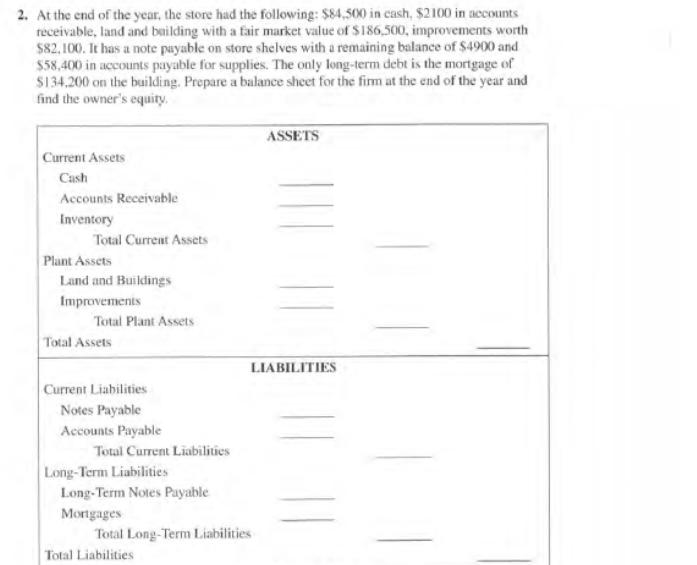

Apple, Inc. was founded by Steve Jobs and Steve Wozniak on April 1, 1976 in Cupertino, California. It was originally named Apple Computer, Inc. based on its original focus on building computers. Management changed the name to Apple, Inc. in 2007 to reflect the fact that the firm was even less focused on computers and was far more focused on a variety of consumer electronics. The firm has revolutionized several industries with its creative and artful products including the iPod (music), iPhone (smart phone), iPad (books, periodicals, movies, music, games, applications, and web content), and iTunes (playing and downloading digital music and video files) among others. Apple has about 400 retail stores in more than thirteen countries and has surpassed both Microsoft and Google in market value. It has more than 60,000 full-time employees with annual revenue of more than $100 billion per year. 1. Assume the following quarterly figures apply to a local computer and electronics store, which sells many Apple products. Prepare an income statement and find net income af- ter taxes for the quarter. Gross Sales $834,200 Salaries and Wages $193,200 Returns $4,500 Rent & Utilities $68,900 Inventory on Jan. 1 $84,200 Advertising $13,900 Cost of Goods Purchased $346,500 Insurance & Payroll Taxes $19,400 Freight $9,100 Miscellaneous Expenses $18,700 Inventory on Dec. 31 $96,200 Income taxes $37,800 Gross Sales Returns Net Sales Inventory, Jan. 1 Cost of Goods Purchased Freight Total Cost of Goods Purchased Total of Goods Available for Sale Inventory, Dec. 31 Cost of Goods Sold Gross Profit Expenses Salaries and Wages Rent & Utilities Advertising Insurance and Payroll Taxes Miscellaneous Expenses Total Expenses Net Income before Taxes Income Taxes NET INCOME AFTER TAXES 2. At the end of the year, the store had the following: $84,500 in cash, $2100 in accounts receivable, land and building with a fair market value of $186,500, improvements worth $82,100. It has a note payable on store shelves with a remaining balance of $4900 and $58,400 in accounts payable for supplies. The only long-term debt is the mortgage of $134,200 on the building. Prepare a balance sheet for the firm at the end of the year and find the owner's equity, Current Assets Cash Accounts Receivable Inventory Total Current Assets Plant Assets Land and Buildings Improvements Total Plant Assets Total Assets Current Liabilities Notes Payable Accounts Payable Total Current Liabilities Long-Term Liabilities Long-Term Notes Payable Mortgages Total Long-Term Liabilities Total Liabilities ASSETS LIABILITIES

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles And Practice Of Marketing

Authors: David Jobber, Fiona Ellis-Chadwick

10th Edition

1526849534, 978-1526849533