Question

Apply basic income tax concepts for personal tax planning Recommend investment strategies from a tax 1. Apply basic income tax concepts for personal tax planning

Apply basic income tax concepts for personal tax planning Recommend investment strategies from a tax

Apply basic income tax concepts for personal tax planning Recommend investment strategies from a tax

1. Apply basic income tax concepts for personal tax planning 2.Recommend investment strategies from a tax perspective

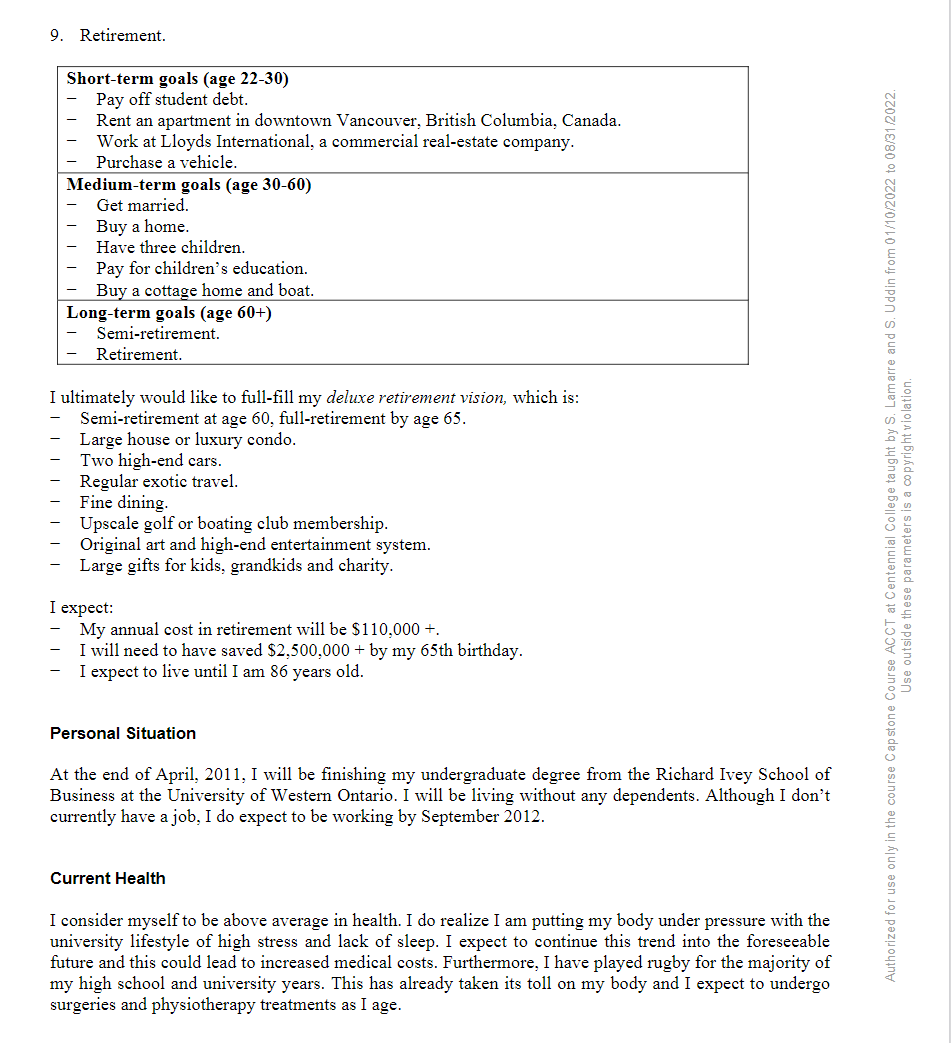

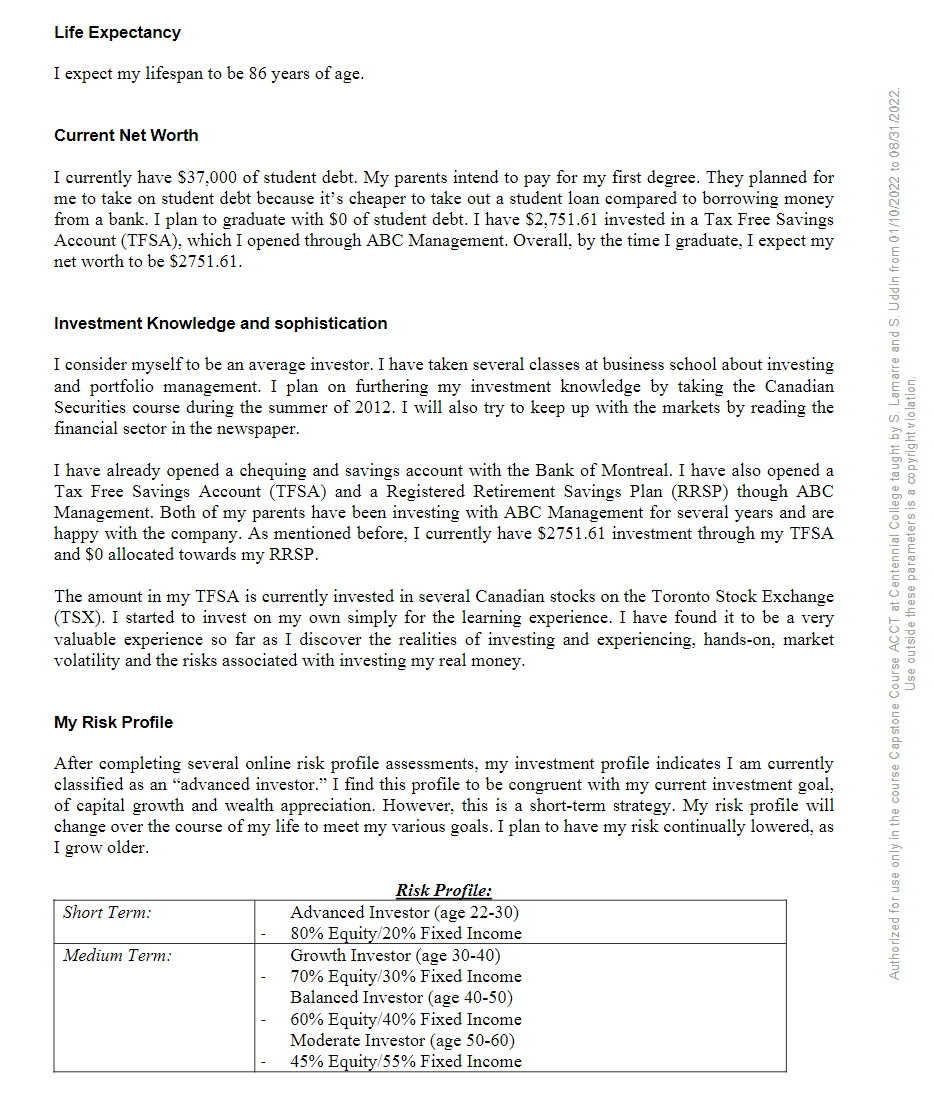

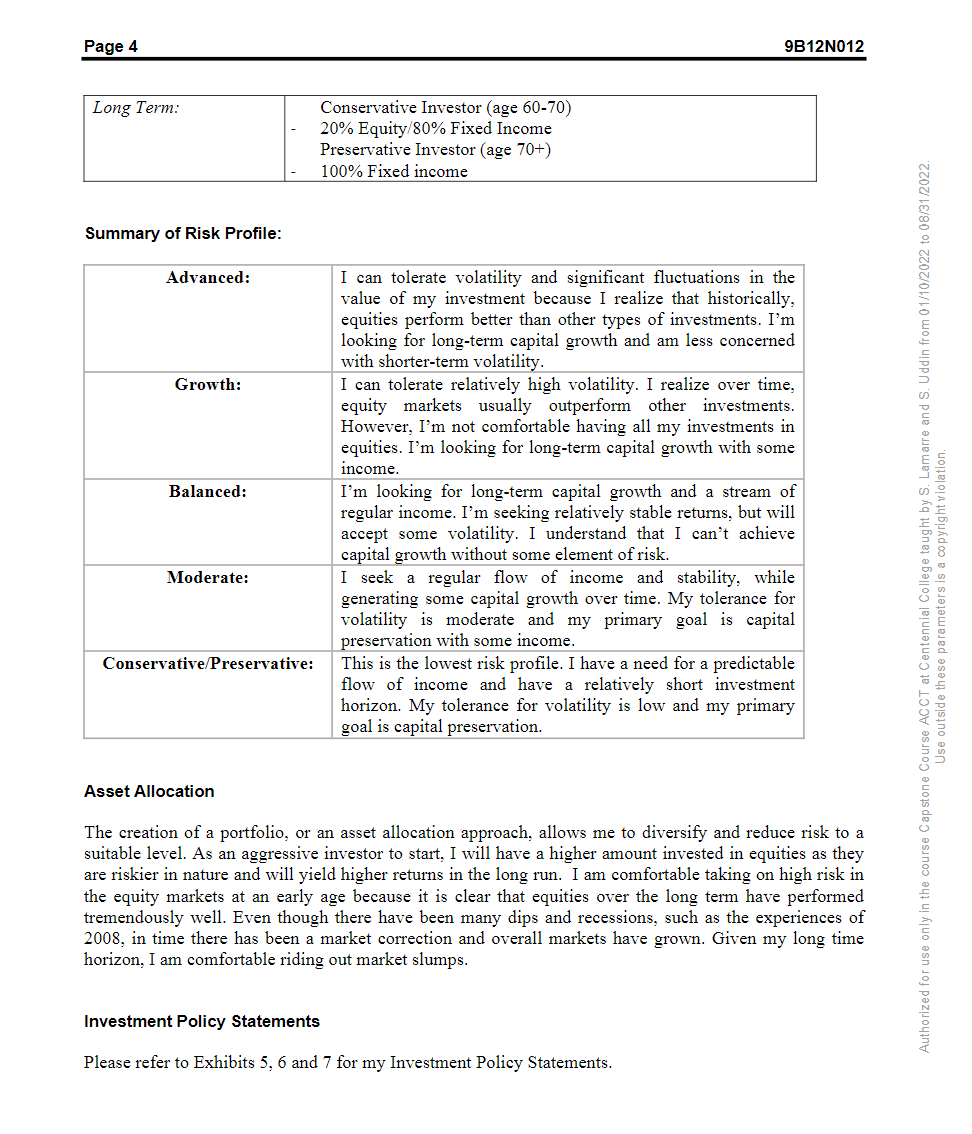

Copyright 2012, Richard Ivey School of Business Foundation Version: 2012-07-31 Mary Spencer was putting the final touches to her personal financial plan before graduating from the Richard Ivey School of Business HBA program in the spring of 2012. In general, Mary was happy with her plan. Her goals, investment policy statement and financial budget all made perfect sense to her. Even so, she kept going back to one number a 43 per cent tax rate! It didn't seem fair that just when Spencer started to make some serious income, she would have to give 43 per cent of it to the government. During one of her courses, Spencer had spent some time learning about tax strategies available to Canadians. They all seemed to involve three and four letter acronyms TSFA, RSP, RHOSP, etc. but she wondered which ones would have the optimal impact on her tax situation. What combination of three or four would work best together? OVERVIEW This personal investment plan provides my general investment goals and objectives following graduation from the Richard Ivey School of Business in April 2012. The investment plan describes the strategies I will employ to meet my financial needs and achieve my personal goals in life. Personal Goals My personal goals include the following in no particular order: 1. Pay off student debt. 2. Rent an apartment. 3. Buy a car. 4. Get married. 5. Buy a home. 6. Have children. 7. Pay for the children's education. 8. Buy a cottage home and boat. 9. Retirement. Short-term goals (age 22-30) Pay off student debt. Rent an apartment in downtown Vancouver, British Columbia, Canada. Work at Lloyds International, a commercial real-estate company. Purchase a vehicle. Medium-term goals (age 30-60) Get married. Buy a home. Have three children. Pay for children's education. Buy a cottage home and boat. Long-term goals (age 60+) Semi-retirement. Retirement I ultimately would like to full-fill my deluxe retirement vision, which is: Semi-retirement at age 60, full-retirement by age 65. Large house or luxury condo. Two high-end cars. Regular exotic travel. Fine dining Upscale golf or boating club membership. Original art and high-end entertainment system. Large gifts for kids, grandkids and charity. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation. I expect: My annual cost in retirement will be $110,000+. I will need to have saved $2,500,000 + by my 65th birthday. I expect to live until I am 86 years old. Personal Situation At the end of April, 2011, I will be finishing my undergraduate degree from the Richard Ivey School of Business at the University of Western Ontario. I will be living without any dependents. Although I don't currently have a job, I do expect to be working by September 2012. Current Health I consider myself to be above average in health. I do realize I am putting my body under pressure with the university lifestyle of high stress and lack of sleep. I expect to continue this trend into the foreseeable future and this could lead to increased medical costs. Furthermore, I have played rugby for the majority of my high school and university years. This has already taken its toll on my body and I expect to undergo surgeries and physiotherapy treatments as I age. Life Expectancy I expect my lifespan to be 86 years of age. Current Net Worth I currently have $37,000 of student debt. My parents intend to pay for my first degree. They planned for me to take on student debt because it's cheaper to take out a student loan compared to borrowing money from a bank. I plan to graduate with $0 of student debt. I have $2,751.61 invested in a Tax Free Savings Account (TFSA), which I opened through ABC Management. Overall, by the time I graduate, I expect my net worth to be $2751.61. Investment Knowledge and sophistication I consider myself to be an average investor. I have taken several classes at business school about investing and portfolio management. I plan on furthering my investment knowledge by taking the Canadian Securities course during the summer of 2012. I will also try to keep up with the markets by reading the financial sector in the newspaper. I have already opened a chequing and savings account with the Bank of Montreal. I have also opened a Tax Free Savings Account (TFSA) and a Registered Retirement Savings Plan (RRSP) though ABC Management. Both of my parents have been investing with ABC Management for several years and are happy with the company. As mentioned before, I currently have $2751.61 investment through my TFSA and $0 allocated towards my RRSP. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022. Use outside these parameters is a copyright violation The amount in my TFSA is currently invested in several Canadian stocks on the Toronto Stock Exchange (TSX). I started to invest on my own simply for the learning experience. I have found it to be a very valuable experience so far as I discover the realities of investing and experiencing, hands-on, market volatility and the risks associated with investing my real money. My Risk Profile After completing several online risk profile assessments, my investment profile indicates I am currently classified as an advanced investor." I find this profile to be congruent with my current investment goal, of capital growth and wealth appreciation. However, this is a short-term strategy. My risk profile will change over the course of my life to meet my various goals. I plan to have my risk continually lowered, as I grow older. Short Term: Medium Term: Risk Profile: Advanced Investor (age 22-30) 80% Equity/20% Fixed Income Growth Investor (age 30-40) 70% Equity/30% Fixed Income Balanced Investor (age 40-50) 60% Equity/40% Fixed Income Moderate Investor (age 50-60) 45% Equity/55% Fixed Income Page 4 9B12N012 Long Term: Conservative Investor (age 60-70) 20% Equity/80% Fixed Income Preservative Investor (age 70+) 100% Fixed income Summary of Risk Profile: Advanced: Growth: . Balanced: I can tolerate volatility and significant fluctuations in the value of my investment because I realize that historically, equities perform better than other types of investments. I'm looking for long-term capital growth and am less concerned with shorter-term volatility. I can tolerate relatively high volatility. I realize over time, equity markets usually outperform other investments. However, I'm not comfortable having all my investments in equities. I'm looking for long-term capital growth with some income. I'm looking for long-term capital growth and a stream of regular income. I'm seeking relatively stable returns, but will accept some volatility. I understand that I can't achieve capital growth without some element of risk. I seek a regular flow of income and stability, while generating some capital growth over time. My tolerance for volatility is moderate and my primary goal is capital preservation with some income. This is the lowest risk profile. I have a need for a predictable flow of income and have a relatively short investment horizon. My tolerance for volatility is low and my primary goal is capital preservation. Moderate: Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation Conservative/Preservative: Asset Allocation The creation of a portfolio, or an asset allocation approach, allows me to diversify and reduce risk to a suitable level. As an aggressive investor to start, I will have a higher amount invested in equities as they are riskier in nature and will yield higher returns in the long run. I am comfortat taking on gh risk in the equity markets at an early age because it is clear that equities over the long term have performed tremendously well. Even though there have been many dips and recessions, such as the experiences of 2008, in time there has been a market correction and overall markets have grown. Given my long time horizon, I am comfortable riding out market slumps. Investment Policy Statements Please refer to Exhibits 5, 6 and 7 for my Investment Policy Statements. INVESTMENT GUIDELINE Debt Before I start investing, I want to be completely debt free. I will begin debt free thanks to my parents, however, if I do accumulate debt I will want to pay off my highest interest rate debt first before investing. Lingering debt will only accumulate and become a burden later in life if it is not addressed early. Invest Early Every dollar I save now is worth more than saving it in any other decade due to compounding interest. To achieve my goals, it is imperative I start savings and investing now, for the future, in order to take advantage of compounding interest. Inflation I expect inflation will be above 3.0 per cent within the next four to six years. If anything. I will strive to have my savings and investments beat inflation, so the value of my savings is not eaten away. Risk When I am young I can afford to take on more risk since I have time to ride out the inevitable storms. It may be a good idea for me to allocate a high percentage to the equities market. This can include buying blue-chip stocks, exchange-traded funds (ETFs) or equity mutual funds. I may want to look at bonds or other less volatile investments, but this should only be a small part of my long-term portfolio since inflation will eat away at the small returns I may achieve. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation INVESTMENT VEHICLES Mutual Fund A mutual fund is an investment vehicle I am willing to consider. It is an investment made up of a pool of funds collected from many investors for the purpose of investing in securities such as stocks, bonds, money market instruments and similar assets. Professional money managers operate them. A mutual fund's portfolio is structured and maintained to match the investment objectives stated in its prospectus. Mutual funds usually change a fee of 2.5 per cent of the funds worth. Commissioned Advisors Advisors who work on commission almost never recommends index funds: they earn higher commissions from more expensive products, and many mutual fund dealers are not licensed to sell ETFs. Page 6 9B12N012 Exchange-traded Funds Exchange-traded funds (ETFs) are another investment vehicle to consider. An ETF, like a mutual fund, is a basket of stocks or bonds, usually designed to track broad market or sector. Unlike mutual funds, ETFs trade on an exchange, like individual stocks. You can easily build a diversified portfolio with just three or four ETFs. For example, iShares S&P/TSX Composite Index Fund (ticker: XIC) gives you a stake in all 200-plus stocks that make up the index. Since most ETFs simply track an index, there's no highly paid manager in charge of picking stocks to try to outperform the market. That means the fees are typically much lower than mutual funds: an ETF's annual fee can be less than 0.2 per cent (average 0.5-1.0 per cent), compared to as much as 3 per cent for traditional mutual funds. ETFs offer the same diversification I could find in a well-managed balanced mutual fund, but at a much lower cost. In the long run, the lower fees add up to higher returns for me as an investor. Over a five-year period, index ETFs perform better than about 75 per cent of actively managed mutual funds. Registered Retirement Savings Plan An RRSP is an ideal tool because investments grow tax-free in the account and are only taxed when withdrawn. Employer contributions to RRSPs are non-taxable benefits. Contributions are tax deductible, saving money in the current year. The RRSP should be used for medium to long-term savings because withdrawals are taxed. However, an investor can use the Home Buyer's Plans to withdraw up to $25,000 for the purchase of a home and up to $10,000 under the Lifelong Learning Plan to fund future education'. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022. Use outside these parameters is a copyright violation. Tax Free Savings Account A TFSA allows for easier access to funds compared to an RRSP. A TFSA allows savings of a maximum of $5000 per year and all capital gains and interest earned is tax-free. Contrary to an RRSP, no tax is paid on the withdrawal. There are many asset classes and investment vehicles that can be utilized for a TFSA. Registered Education Savings Plan An RESP is a savings program designed to save for a child's future education. The RESP is tax-sheltered and has a lifetime contribution limit of $50,000. The government contributes up to 20 per cent of the amount invested through the Canada Education Savings Grant (maximum $500 per year). Emergency Fund After seeing thousands of workers laid off during the most recent recession, I learned unemployment is a serious factor that needs to be considered in my financial plan. As a general rule, I will have an emergency fund to cover at least four months of my basic living expenses. This fund will be based on cash or a high interest savings account. Page 7 9B12N012 SECURITY Life Insurance If I do happen to die, my children will need to rely on my income after my death. I will be wasting money if I buy more insurance than I really need, so I need to know how much I contribute, after taxes, to my family's income. I will want to buy enough insurance to replace about 75 per cent of my lost income, plus a little but extra for funeral expenses and legal fees. To do this, I will buy from a broker who represents several insurance firms, so I can compare quotes. Disability insurance I believe disability insurance is even more important than life insurance. According to Money Sense Magazine, statistically, I am more likely to suffer a disability early than I am to die early. Budget Although difficult to do, it is crucial to budget as it gives a starting point to determine how much money will be left over to invest. With my budget, it is important that I plan to semi-retire at age 60 and fully retire by 65. I will need roughly $110,000 annually to fund my retirement lifestyle. Given I expect to live to 86. I will expect to need roughly $2,500,000 saved for retirement by the time I turn 65. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation Big Ticket Budgeting Expenses Rent an apartment I budgeted to rent an apartment in downtown Vancouver for approximately $1,400 per month including utilities. I cannot afford to spend more than $1,400 per month. If rates increase, I will move to the suburbs. Buy a car I have budgeted to buy a BMW M6 for $30,000 off of my mother when I turn 30 years old. I will use public transportation until then. I have budgeted for $3,500 annual transportation expenses including gas and insurance. I plan to live close to where I work and won't be driving often. I will utilize it mainly on weekends. Get married I have budgeted $25,000 towards my marriage. I have included this in my entertainment expense when I am between 35-40 years old. Page 8 9B12N01 Buy a home I have budgeted to put a $110,000 down payment on a house between 35-40 years of age. I wi split the cost of a $630,000 dollar home with my life partner. My mortgage and tax payment have been front loaded so the fees associated with the mortgage don't linger around. Have children I plan on having 3 children. I expect to have all three before the time I turn 40. I will want to spo my children and have allocated a very large budget towards them. Pay for the children's education I would like to provide my children with the same educational opportunity my parents provide to me. My goal is to have all three of my children attend private school. My husband and I wi also be willing to pay for their first degree if they wish to obtain one, and I expect they will. As soon as I have kids I will start a Registered Education Savings Plan (RESP). I will seek to se up a RESP with a discount brokerage, and then purchase low-cost index mutual funds. I will tr to max out my RESP contributions (up to $2,500 a year per child). It is worth noting that ever a dollar I contribute to my children's RESP earns a 20 per cent top-up form the government. I wi use the self-directed RESPs, since they are far more flexible and transparent than the group "pooled plans. The maximum Canada Education Savings Grant (CESG) I may receive in an one year is $1,000 and the lifetime maximum is $7,200. There is no annual contribution limit, bu the most I can contribute to any one child's account is $50,000. I will not get a tax refund for money I put into and RESP, but the funds grow tax-free and th withdrawals are taxed in the student's hands. In most cases, the withdrawals are effectively tax free, since any amount owing should be offset by the student's education credit and personal ta credit. Buy a cottage home and boat When I turn 60, I have budgeted to purchase a $400,000 small cottage and boat on a nice lake in interior B.C. See Exhibits 1-4 for personal budget. Copyright 2012, Richard Ivey School of Business Foundation Version: 2012-07-31 Mary Spencer was putting the final touches to her personal financial plan before graduating from the Richard Ivey School of Business HBA program in the spring of 2012. In general, Mary was happy with her plan. Her goals, investment policy statement and financial budget all made perfect sense to her. Even so, she kept going back to one number a 43 per cent tax rate! It didn't seem fair that just when Spencer started to make some serious income, she would have to give 43 per cent of it to the government. During one of her courses, Spencer had spent some time learning about tax strategies available to Canadians. They all seemed to involve three and four letter acronyms TSFA, RSP, RHOSP, etc. but she wondered which ones would have the optimal impact on her tax situation. What combination of three or four would work best together? OVERVIEW This personal investment plan provides my general investment goals and objectives following graduation from the Richard Ivey School of Business in April 2012. The investment plan describes the strategies I will employ to meet my financial needs and achieve my personal goals in life. Personal Goals My personal goals include the following in no particular order: 1. Pay off student debt. 2. Rent an apartment. 3. Buy a car. 4. Get married. 5. Buy a home. 6. Have children. 7. Pay for the children's education. 8. Buy a cottage home and boat. 9. Retirement. Short-term goals (age 22-30) Pay off student debt. Rent an apartment in downtown Vancouver, British Columbia, Canada. Work at Lloyds International, a commercial real-estate company. Purchase a vehicle. Medium-term goals (age 30-60) Get married. Buy a home. Have three children. Pay for children's education. Buy a cottage home and boat. Long-term goals (age 60+) Semi-retirement. Retirement I ultimately would like to full-fill my deluxe retirement vision, which is: Semi-retirement at age 60, full-retirement by age 65. Large house or luxury condo. Two high-end cars. Regular exotic travel. Fine dining Upscale golf or boating club membership. Original art and high-end entertainment system. Large gifts for kids, grandkids and charity. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation. I expect: My annual cost in retirement will be $110,000+. I will need to have saved $2,500,000 + by my 65th birthday. I expect to live until I am 86 years old. Personal Situation At the end of April, 2011, I will be finishing my undergraduate degree from the Richard Ivey School of Business at the University of Western Ontario. I will be living without any dependents. Although I don't currently have a job, I do expect to be working by September 2012. Current Health I consider myself to be above average in health. I do realize I am putting my body under pressure with the university lifestyle of high stress and lack of sleep. I expect to continue this trend into the foreseeable future and this could lead to increased medical costs. Furthermore, I have played rugby for the majority of my high school and university years. This has already taken its toll on my body and I expect to undergo surgeries and physiotherapy treatments as I age. Life Expectancy I expect my lifespan to be 86 years of age. Current Net Worth I currently have $37,000 of student debt. My parents intend to pay for my first degree. They planned for me to take on student debt because it's cheaper to take out a student loan compared to borrowing money from a bank. I plan to graduate with $0 of student debt. I have $2,751.61 invested in a Tax Free Savings Account (TFSA), which I opened through ABC Management. Overall, by the time I graduate, I expect my net worth to be $2751.61. Investment Knowledge and sophistication I consider myself to be an average investor. I have taken several classes at business school about investing and portfolio management. I plan on furthering my investment knowledge by taking the Canadian Securities course during the summer of 2012. I will also try to keep up with the markets by reading the financial sector in the newspaper. I have already opened a chequing and savings account with the Bank of Montreal. I have also opened a Tax Free Savings Account (TFSA) and a Registered Retirement Savings Plan (RRSP) though ABC Management. Both of my parents have been investing with ABC Management for several years and are happy with the company. As mentioned before, I currently have $2751.61 investment through my TFSA and $0 allocated towards my RRSP. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022. Use outside these parameters is a copyright violation The amount in my TFSA is currently invested in several Canadian stocks on the Toronto Stock Exchange (TSX). I started to invest on my own simply for the learning experience. I have found it to be a very valuable experience so far as I discover the realities of investing and experiencing, hands-on, market volatility and the risks associated with investing my real money. My Risk Profile After completing several online risk profile assessments, my investment profile indicates I am currently classified as an advanced investor." I find this profile to be congruent with my current investment goal, of capital growth and wealth appreciation. However, this is a short-term strategy. My risk profile will change over the course of my life to meet my various goals. I plan to have my risk continually lowered, as I grow older. Short Term: Medium Term: Risk Profile: Advanced Investor (age 22-30) 80% Equity/20% Fixed Income Growth Investor (age 30-40) 70% Equity/30% Fixed Income Balanced Investor (age 40-50) 60% Equity/40% Fixed Income Moderate Investor (age 50-60) 45% Equity/55% Fixed Income Page 4 9B12N012 Long Term: Conservative Investor (age 60-70) 20% Equity/80% Fixed Income Preservative Investor (age 70+) 100% Fixed income Summary of Risk Profile: Advanced: Growth: . Balanced: I can tolerate volatility and significant fluctuations in the value of my investment because I realize that historically, equities perform better than other types of investments. I'm looking for long-term capital growth and am less concerned with shorter-term volatility. I can tolerate relatively high volatility. I realize over time, equity markets usually outperform other investments. However, I'm not comfortable having all my investments in equities. I'm looking for long-term capital growth with some income. I'm looking for long-term capital growth and a stream of regular income. I'm seeking relatively stable returns, but will accept some volatility. I understand that I can't achieve capital growth without some element of risk. I seek a regular flow of income and stability, while generating some capital growth over time. My tolerance for volatility is moderate and my primary goal is capital preservation with some income. This is the lowest risk profile. I have a need for a predictable flow of income and have a relatively short investment horizon. My tolerance for volatility is low and my primary goal is capital preservation. Moderate: Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation Conservative/Preservative: Asset Allocation The creation of a portfolio, or an asset allocation approach, allows me to diversify and reduce risk to a suitable level. As an aggressive investor to start, I will have a higher amount invested in equities as they are riskier in nature and will yield higher returns in the long run. I am comfortat taking on gh risk in the equity markets at an early age because it is clear that equities over the long term have performed tremendously well. Even though there have been many dips and recessions, such as the experiences of 2008, in time there has been a market correction and overall markets have grown. Given my long time horizon, I am comfortable riding out market slumps. Investment Policy Statements Please refer to Exhibits 5, 6 and 7 for my Investment Policy Statements. INVESTMENT GUIDELINE Debt Before I start investing, I want to be completely debt free. I will begin debt free thanks to my parents, however, if I do accumulate debt I will want to pay off my highest interest rate debt first before investing. Lingering debt will only accumulate and become a burden later in life if it is not addressed early. Invest Early Every dollar I save now is worth more than saving it in any other decade due to compounding interest. To achieve my goals, it is imperative I start savings and investing now, for the future, in order to take advantage of compounding interest. Inflation I expect inflation will be above 3.0 per cent within the next four to six years. If anything. I will strive to have my savings and investments beat inflation, so the value of my savings is not eaten away. Risk When I am young I can afford to take on more risk since I have time to ride out the inevitable storms. It may be a good idea for me to allocate a high percentage to the equities market. This can include buying blue-chip stocks, exchange-traded funds (ETFs) or equity mutual funds. I may want to look at bonds or other less volatile investments, but this should only be a small part of my long-term portfolio since inflation will eat away at the small returns I may achieve. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation INVESTMENT VEHICLES Mutual Fund A mutual fund is an investment vehicle I am willing to consider. It is an investment made up of a pool of funds collected from many investors for the purpose of investing in securities such as stocks, bonds, money market instruments and similar assets. Professional money managers operate them. A mutual fund's portfolio is structured and maintained to match the investment objectives stated in its prospectus. Mutual funds usually change a fee of 2.5 per cent of the funds worth. Commissioned Advisors Advisors who work on commission almost never recommends index funds: they earn higher commissions from more expensive products, and many mutual fund dealers are not licensed to sell ETFs. Page 6 9B12N012 Exchange-traded Funds Exchange-traded funds (ETFs) are another investment vehicle to consider. An ETF, like a mutual fund, is a basket of stocks or bonds, usually designed to track broad market or sector. Unlike mutual funds, ETFs trade on an exchange, like individual stocks. You can easily build a diversified portfolio with just three or four ETFs. For example, iShares S&P/TSX Composite Index Fund (ticker: XIC) gives you a stake in all 200-plus stocks that make up the index. Since most ETFs simply track an index, there's no highly paid manager in charge of picking stocks to try to outperform the market. That means the fees are typically much lower than mutual funds: an ETF's annual fee can be less than 0.2 per cent (average 0.5-1.0 per cent), compared to as much as 3 per cent for traditional mutual funds. ETFs offer the same diversification I could find in a well-managed balanced mutual fund, but at a much lower cost. In the long run, the lower fees add up to higher returns for me as an investor. Over a five-year period, index ETFs perform better than about 75 per cent of actively managed mutual funds. Registered Retirement Savings Plan An RRSP is an ideal tool because investments grow tax-free in the account and are only taxed when withdrawn. Employer contributions to RRSPs are non-taxable benefits. Contributions are tax deductible, saving money in the current year. The RRSP should be used for medium to long-term savings because withdrawals are taxed. However, an investor can use the Home Buyer's Plans to withdraw up to $25,000 for the purchase of a home and up to $10,000 under the Lifelong Learning Plan to fund future education'. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022. Use outside these parameters is a copyright violation. Tax Free Savings Account A TFSA allows for easier access to funds compared to an RRSP. A TFSA allows savings of a maximum of $5000 per year and all capital gains and interest earned is tax-free. Contrary to an RRSP, no tax is paid on the withdrawal. There are many asset classes and investment vehicles that can be utilized for a TFSA. Registered Education Savings Plan An RESP is a savings program designed to save for a child's future education. The RESP is tax-sheltered and has a lifetime contribution limit of $50,000. The government contributes up to 20 per cent of the amount invested through the Canada Education Savings Grant (maximum $500 per year). Emergency Fund After seeing thousands of workers laid off during the most recent recession, I learned unemployment is a serious factor that needs to be considered in my financial plan. As a general rule, I will have an emergency fund to cover at least four months of my basic living expenses. This fund will be based on cash or a high interest savings account. Page 7 9B12N012 SECURITY Life Insurance If I do happen to die, my children will need to rely on my income after my death. I will be wasting money if I buy more insurance than I really need, so I need to know how much I contribute, after taxes, to my family's income. I will want to buy enough insurance to replace about 75 per cent of my lost income, plus a little but extra for funeral expenses and legal fees. To do this, I will buy from a broker who represents several insurance firms, so I can compare quotes. Disability insurance I believe disability insurance is even more important than life insurance. According to Money Sense Magazine, statistically, I am more likely to suffer a disability early than I am to die early. Budget Although difficult to do, it is crucial to budget as it gives a starting point to determine how much money will be left over to invest. With my budget, it is important that I plan to semi-retire at age 60 and fully retire by 65. I will need roughly $110,000 annually to fund my retirement lifestyle. Given I expect to live to 86. I will expect to need roughly $2,500,000 saved for retirement by the time I turn 65. Authorized for use only in the course Capstone Course ACCT at Centennial College taught by S. Lamarre and S. Uddin from 01/10/2022 to 08/31 2022 Use outside these parameters is a copyright violation Big Ticket Budgeting Expenses Rent an apartment I budgeted to rent an apartment in downtown Vancouver for approximately $1,400 per month including utilities. I cannot afford to spend more than $1,400 per month. If rates increase, I will move to the suburbs. Buy a car I have budgeted to buy a BMW M6 for $30,000 off of my mother when I turn 30 years old. I will use public transportation until then. I have budgeted for $3,500 annual transportation expenses including gas and insurance. I plan to live close to where I work and won't be driving often. I will utilize it mainly on weekends. Get married I have budgeted $25,000 towards my marriage. I have included this in my entertainment expense when I am between 35-40 years old. Page 8 9B12N01 Buy a home I have budgeted to put a $110,000 down payment on a house between 35-40 years of age. I wi split the cost of a $630,000 dollar home with my life partner. My mortgage and tax payment have been front loaded so the fees associated with the mortgage don't linger around. Have children I plan on having 3 children. I expect to have all three before the time I turn 40. I will want to spo my children and have allocated a very large budget towards them. Pay for the children's education I would like to provide my children with the same educational opportunity my parents provide to me. My goal is to have all three of my children attend private school. My husband and I wi also be willing to pay for their first degree if they wish to obtain one, and I expect they will. As soon as I have kids I will start a Registered Education Savings Plan (RESP). I will seek to se up a RESP with a discount brokerage, and then purchase low-cost index mutual funds. I will tr to max out my RESP contributions (up to $2,500 a year per child). It is worth noting that ever a dollar I contribute to my children's RESP earns a 20 per cent top-up form the government. I wi use the self-directed RESPs, since they are far more flexible and transparent than the group "pooled plans. The maximum Canada Education Savings Grant (CESG) I may receive in an one year is $1,000 and the lifetime maximum is $7,200. There is no annual contribution limit, bu the most I can contribute to any one child's account is $50,000. I will not get a tax refund for money I put into and RESP, but the funds grow tax-free and th withdrawals are taxed in the student's hands. In most cases, the withdrawals are effectively tax free, since any amount owing should be offset by the student's education credit and personal ta credit. Buy a cottage home and boat When I turn 60, I have budgeted to purchase a $400,000 small cottage and boat on a nice lake in interior B.C. See Exhibits 1-4 for personal budgetStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Amazon Goldmine How Amazon Can Make You A Millionaire

Authors: Mrs Esther B. Odejimi

1st Edition

1533513406, 978-1533513403