Answered step by step

Verified Expert Solution

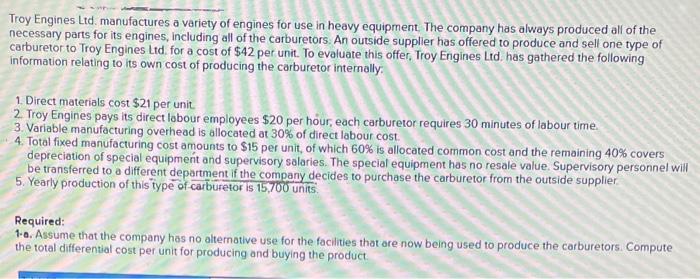

Question

1 Approved Answer

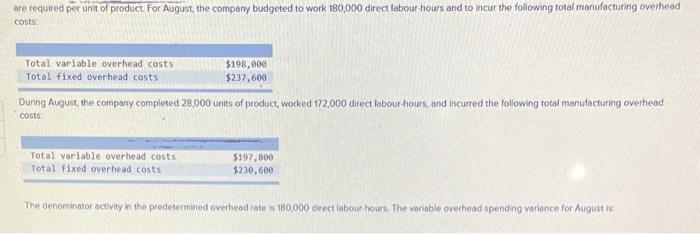

are required per unit of product For August, the company budgeted to work 180,000 direct labour hours and to incur the following total manufacturing overhead

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cloud Computing Data Auditing Algorithm

Authors: Manjur Kolhar, Abdalla Alameen, Bhawna Dhupia, Sadia Rubab, Mujthaba Gulam

1st Edition